Image Source: Mondelez

By Brian Nelson, CFA

Back in late January, Mondelez International (MDLZ) reported better than expected fourth-quarter results. Net revenue advanced 7.1% in the quarter thanks to strong organic net revenue growth of 9.8% offset in part by weaker volume/mix. Gross margin increased 190 basis points in the quarter as the company pushed through meaningful price increases across its regional portfolio led by particular strength in Latin America. Adjusted diluted earnings per share increased 23.5% on a constant-currency basis.

Management was upbeat on the performance in the press release:

Our 2023 results underscore the strength of our execution, the importance of our investments and the resiliency of our portfolio, footprint, categories, and brands. We delivered double-digit top-line and earnings growth for the year, leading to strong cash flow generation and capital return to shareholders. Our growth was balanced across developed and emerging markets, with robust performance in all regions. As we enter 2024, we continue focusing on strong execution, supported by a significant increase in investments behind our brands, capabilities, and talent. We remain confident that we are well positioned for sustainable top- and bottom-line growth in the years ahead.

Image Source: Mondelez

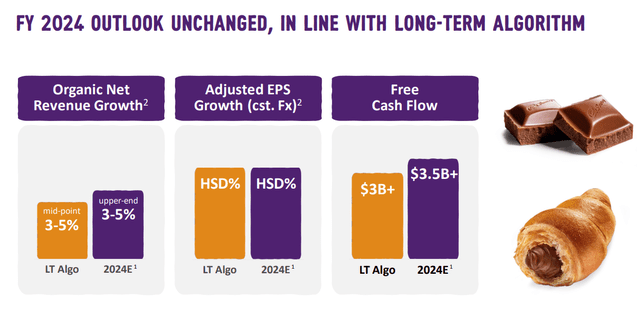

Mondelez’s full-year cash flow from operations advanced to $4.7 billion, up from $3.9 million last year. Free cash flow was up $0.6 billion on the year, to $3.6 billion. Looking ahead to 2024, Mondelez expects organic net revenue growth of 3%-5%, high-single-digit adjusted earnings per share on a constant currency basis, and the company is looking to haul in free cash flow greater than $3.5 billion. The organic revenue growth outlook for 2024 is meaningfully below the 14.7% mark it put up in 2023, with management pointing to geopolitical uncertainty as the cause. Nonetheless, we’re huge fans of Mondelez’s collection of valuable brands, and its ~2.4% dividend yield is worth a look.

———-

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.