By Brian Nelson, CFA

On February 22, Booking Holdings (BKNG) reported better-than-expected fourth quarter results that beat expectations on both the top and bottom lines, but the company noted that its business had been impacted by the conflict in the Middle East. Regardless, Booking Holdings remains one of our favorite ideas on the market today due to its fantastic free cash flow generation and secular growth prospects. Following in the footsteps of Meta Platforms this quarter, Booking Holdings also initiated its first-ever dividend, a quarterly cash dividend of $8.75 per share, and we like what this implies with respect to capital discipline. Our fair value estimate stands north of $4,100 per share, well above where shares are currently trading at this time.

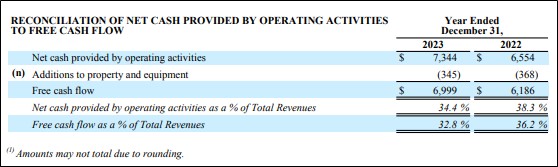

Image: Booking Holdings continues to put up robust free cash flow margins.

During the fourth quarter, gross travel bookings, net of cancellations, advanced 16% from the prior-year quarter, while room nights booked increased 9%. Total revenues leapt 18% on a year-over-year basis in the quarter, while non-GAAP net income and non-GAAP net income per diluted common share advanced 18% and 29%, respectively. Adjusted EBITDA increased 18% from last year’s quarter. For the year ended December 31, cash flow from operations increased to ~$7.34 billion from ~$6.55 billion last year, while additions to property and equipment was roughly flat at $345 million in 2023 (was $368 million last year). Total free cash flow in 2023 was a robust ~$7 billion (roughly 32.8% of total revenue), up from ~$6.19 billion in 2022. Booking Holdings ended 2023 with a modest net debt position, but not of the magnitude that detracts from its attractive financial condition.

In its press release, management noted that the war in the Middle East is having an impact on operations, but that its long-term outlook remains quite bright:

We are pleased to report a strong close to 2023 with fourth quarter room nights growing 9% year-over-year or 11% when excluding business associated with Israel, which was significantly impacted by the war. For the full year, we reached a significant milestone with over 1 billion room nights booked on our platforms, and we achieved record levels of gross bookings, revenue, and operating income. We are confident in the long-term growth of leisure travel and in the opportunities ahead for our company as we continue our work to deliver a better offering and experience for our supply partners and our travelers.

All told, Booking Holdings is one of our favorite ideas, and we view shares as attractively valued on the basis of our point fair value estimate and quite attractive when considering the high end of our fair value estimate range. The pace of the company’s gross travel bookings and room nights booked continues to be robust, despite dislocations in its business associated with Israel, and the firm’s free cash flow generation continues to march in the right direction, with the company putting up fantastic free cash flow margins. We like Booking Holdings as an idea in the Best Ideas Newsletter portfolio, and we won’t be removing it anytime soon. Its new dividend implies a forward estimated dividend yield of ~0.96%.

NOW READ: 12 Reasons to Stay Aggressive in 2024

NOW READ: 2023 Was a Fantastic Year! Are You Ready for 2024?

———-

Tickerized for BKNG, EXPE, ABNB, TRIP

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.