By Brian Nelson, CFA

Visa (V) Operating and Free Cash Flow Margins Remain Robust, Consumer Spending Remains Resilient

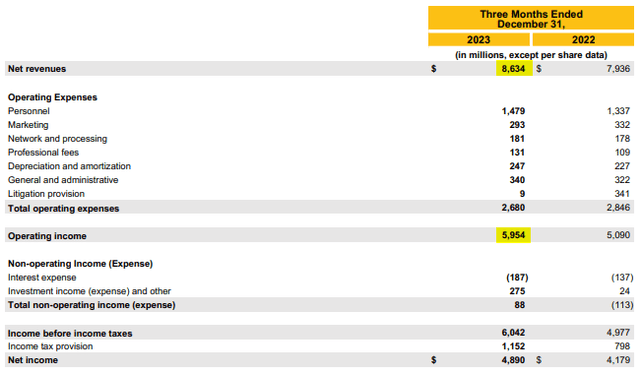

Image: Visa’s operating margins are phenomenal. Image Source: Visa

On January 25, top-weighted Best Ideas Newsletter portfolio holding Visa reported excellent first-quarter fiscal 2024 results that beat on the top and bottom lines. Net revenues advanced 9% on a year-over-year basis, while the firm was able to drive non-GAAP net income 8% higher and non-GAAP earnings per share 11% higher. In the quarter, payments volume advanced 8%, cross-border volume advanced 16%, and processed transactions increased 9%, all on a year-over-year basis. The company’s operating margin came in at an impressive 69% in the quarter, and it hauled in ~$3.35 billion in free cash flow, roughly 38.8% of revenue. The company ended 2023 with $20.2 billion in cash, cash equivalents, and investments, slightly lower than its long-term debt load of $20.7 billion. Management noted that it continues to experience “stable growth in overall payments volume and processed transactions” and that “consumer spending remained resilient,” a good sign for overall economic activity. We continue to be huge fans of Visa due in part to its secular growth prospects in e-commerce proliferation, as well as its healthy operating and free cash flow margins, which reflect of its moaty business model that reaps in fees every time one of its cards is swiped. We expect Visa to remain a strong performer.

Intel (INTC) Continues to Burn Free Cash, Outlook for 2024 Disappoints

Intel is coming off a rough period where the firm recently slashed its dividend payout, and the company’s weak outlook showed that it is far from out of the woods, particularly as rivals Nvidia (NVDA) and AMD (AMD) gain significant traction in artificial intelligence [AI]. Intel’s fourth-quarter results, released January 25, weren’t terrible thanks in part to a rebound in personal computer demand and it beat both on the top and bottom lines, but its guidance for the first quarter of 2024 set revenue in the range of $12.2-$13.2 billion, well below what the Street had been forecasting ($14.16 billion). The firm is also targeting non-GAAP earnings per share of $0.13, which also came in far below the consensus forecast. Intel’s new internal foundry model has made the firm far more capital-intensive than we would like, and we continue to prefer entities that have strong net cash positions and are able to drive meaningful revenue expansion with little capital outlays – business models more like Visa’s, for example. Intel achieved $3 billion in cost savings during 2023 and expects to achieve further efficiencies in 2024, but management’s non-GAAP gross margin continues to be volatile, expected to come in at 44.5% in the first quarter of 2024 — an improvement over full-year 2023’s mark of 43.6%, but lower than the 48.8% in the fourth quarter of last year and 47.3% in full-year 2022. Intel burned through $14.3 billion in free cash flow last year, while it ended the year with a net debt position of ~$24.2 billion. Intel’s weak outlook coupled with challenges to its free cash flow and its large net debt position leave a lot to be desired, and we won’t be adding the firm to any newsletter portfolio anytime soon.

Humana’s (HUM) Bottom Line Outlook for 2024 Misses Big, Medical Costs on the Rise

Health insurance company Humana reported dismal fourth quarter results January 25 that showed ominous medical cost trends, a warning shot across the bow for rivals CVS Health (CVS), Cigna (CI), Centene (CNC), UnitedHealth Group (UNH), Molina Healthcare (MOH), Clover Health (CLOV), Alignment Healthcare (ALHC), and Elevance Health (ELV). Humana beat revenue growth expectations during its fourth quarter of 2023, but non-GAAP earnings per share came in far below the consensus expectations “driven by higher than anticipated inpatient utilization…and a further increase in non-inpatient trends.” What’s worse, Humana expects the cost pressures it experienced in the latter months of 2023 to persist through all of 2024, with the firm guiding adjusted GAAP earnings per share to approximately $16.00, far below analysts estimates of $28.91 – a huge miss and far below the $26.09 non-GAAP mark it reported in 2023. Other health insurance providers, including UnitedHealth Group, have warned about higher costs to their businesses as procedures that were delayed during the pandemic are now being completed, and we would expect the group to continue to remain under pressure as the market gets a handle on just how steep cost pressures will be. The magnitude of Humana’s outlook miss is quite concerning, and while we don’t have plans to add the stock to any newsletter portfolio, it has us quite nervous about the potential downside risks associated with Best Ideas Newsletter portfolio holding UnitedHealth Group. For now, however, we’re not taking any action, as we monitor medical cost trends closely.

PayPal (PYPL) Fails to “Shock the World”

New PayPal CEO Alex Chriss was recently on CNBC where he stated that PayPal would shock the world with its new innovations on January 25. Unfortunately, PayPal overpromised and underdelivered as the market was not excited by the improvements — which were not revolutionary, in our view, nor did they positively surprise many. The company announced six new innovations, including 1) a new PayPal checkout experience that speeds up check out for consumers, 2) Fastlane by PayPal (a new one-click guest checkout experience), 3) Smart Receipts (a receipt offered to consumers that uses AI to optimize and drive future purchases), 4) greater customization through its advanced offers program, 5) CashPass (which offers customers cash back on purchases), and 6) Venmo business profiles (which helps businesses get discovered). Though the innovations are great, we think the problems at PayPal run much deeper. The fintech space is now cluttered with competition, and the negative consumer sentiment towards PayPal is astonishing. Why consumers care which payment platform they use by name is beyond our comprehension, and while PayPal literally processes credit card transactions separate from having an account with them, many don’t want anything to do with the company, for one reason or another. This is part of the reason why PayPal’s shares will likely continue to experience pressure, in our view. Consumer sentiment is decidedly negative. We’re not adding this once stock-market darling to any newsletter portfolio anytime soon.

—–

NOW READ: 12 Reasons to Stay Aggressive in 2024

NOW READ: 2023 Was a Fantastic Year! Are You Ready for 2024?

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.