Image Shown: Dividend growth idea Home Depot Inc is a stellar free cash flow generator in almost any operating environment. Historically, the home improvement retailer’s free cash flows have fully covered its dividend obligations, and we forecast that will continue to be the case going forward. However, we caution that its sizable share repurchases are being funded in part by its balance sheet. The firm has a large net debt load on the books. Image Source: Home Depot Inc – Second Quarter of Fiscal 2022 IR Earnings Presentation

By Callum Turcan

On August 16, Home Depot Inc (HD) reported second-quarter earnings for fiscal 2022 (period ended July 31, 2022) that beat both consensus top- and bottom-line estimates. The home improvement retailer also reaffirmed its guidance for fiscal 2022 in conjunction with its latest earnings update. We like Home Depot as an idea in the Dividend Growth Newsletter portfolio. Shares of HD yield ~2.4% as of this writing, and our fair value estimate sits at $345 per share of Home Depot, well above where the company’s shares are trading at as of this writing. Home Depot’s free cash flow generating abilities and pricing power are impressive, and its growth runway remains largely intact, even in the face of sizable exogenous shocks.

Earnings Update

In the fiscal second quarter, Home Depot reported that its customer transactions declined by 3.0% year-over-year. However, its strong pricing power saw its average ticket size grow 9.1% year-over-year resulting in its retail sales per square foot advancing by 5.7%, enabling its comparable sales to grow by 5.8% year-over-year last fiscal quarter. The company’s US comparable sales were up 5.4% year-over-year last fiscal quarter. Sustained strength at its do-it-yourself (‘DIY’) customer base and rock-solid demand from its professional customer base were key here.

Home Depot’s GAAP revenues were up 7% year-over-year in the fiscal second quarter, reaching $43.8 billion. Its GAAP gross profit rose 6% year-over-year as its GAAP gross margin fell by ~15 basis points to hit 33.1% last fiscal quarter. Aided by economies of scale, Home Depot’s GAAP operating income rose 9% year-over-year last fiscal quarter as its GAAP operating margin rose ~30 basis points to reach 16.5%. The firm’s GAAP diluted EPS rose over 11% year-over-year in the fiscal second quarter to hit $5.05 as Home Depot benefited from nice net income growth and a sizable reduction in its outstanding diluted share count.

Overall, Home Depot put up tremendous performance last fiscal quarter, and we appreciate the retailer reaffirming its full-year guidance for fiscal 2022. This fiscal year, Home Depot is guiding for both its comparable and reported sales to grow by 3% on an annual basis, its operating margin to come in at 15.4%, and for its diluted EPS to grow in the mid-single-digit range on an annual basis.

In relation to its fiscal second quarter performance, Home Depot appears to expect that exogenous factors (such as inflationary headwinds, supply chain hurdles, and rising labor costs) will weigh negatively on its performance in the second half of this fiscal year. With that in mind, Home Depot’s business is still holding up quite well.

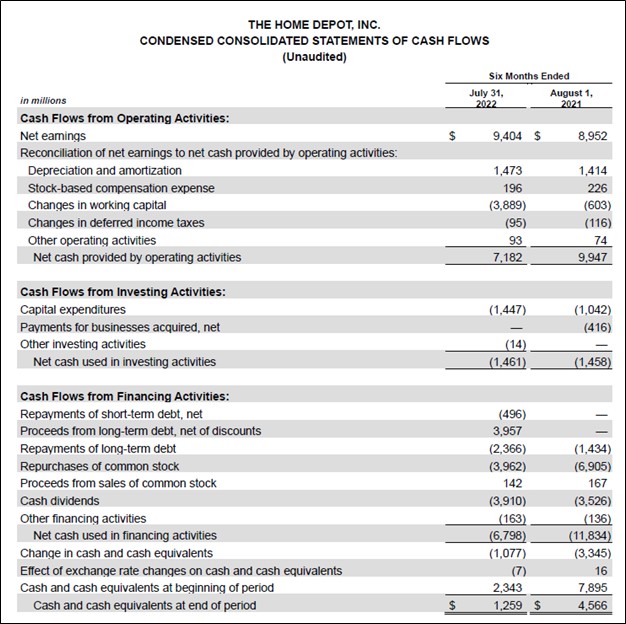

As of July 31, Home Depot had a net debt load of $39.8 billion (inclusive of short-term debt) on the books along with sizable operating lease liabilities. We caution that its large net debt load is concerning, though given Home Depot’s stellar cash flow generating abilities, we view that burden as manageable.

Home Depot generated $5.7 billion in free cash flow during the first half of fiscal 2022, even in the face of a $3.9 billion build in its working capital, while spending $3.9 billion covering its dividend obligations. The firm also spent $4.0 billion buying back its common stock during this period, and Home Depot’s share buyback programs are a key reason why its net debt load is large and steadily growing.

In our view, it would be prudent for the retailer to scale back the pace of its share repurchases to pare down its net debt load. As shares of HD have been trading meaningfully below our estimate of their intrinsic value and continue to do so, we view Home Depot’s share buybacks as a good capital allocation strategy when done in moderation so the firm can maintain its balance sheet health.

Concluding Thoughts

There is a lot to like about Home Depot as its business model has proven to be incredibly resilient of late. Inflationary headwinds, supply chain hurdles, and labor shortages are concerning, though the home improvement retailer has been able to adeptly navigate around those issues so far. Looking ahead, we expect Home Depot will continue to reward income seeking investors via sizable dividend increases. We continue to like Home Depot in the Dividend Growth Newsletter portfolio.

—–

Discretionary Spending Industry – ATVI, BBY, CBRL, CMG, DIS, DG, DLTR, DPZ, EL, F, GM, HAS, HD, LOW, MCD, NFLX, NKE, SBUX, TSLA, YUM, DKS, TJX, ROST, WHR, KMX, AZO, RL, ULTA, LEG, GPC, VFC, CTAS, WSM

Tickerized for HD, WMT, LOW, ITB, DHI, KBH, PHM, TOL, MAS, OC, SHW, LL, XHB, NAIL, HOMZ, LEN, FND, RDFN, Z, ZG, BZH, NVR, MTH, WHR, PKB, VMC, MLM, EXP, SUM, WSC

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares of DIS, META, GOOG, VRTX, and XLE and is long call options on DIS, GOOG, META, MSFT, V, and VRTX and is long put options on RDFN and RKT. Berkshire Hathaway Inc Class B shares (BRK.B), Chipotle Mexican Grill Inc (CMG), Dollar General Corporation (DG), Domino’s Pizza Inc (DPZ) and The Walt Disney Company (DIS) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. Dick’s Sporting Goods Inc (DKS) and Home Depot Inc (HD) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.