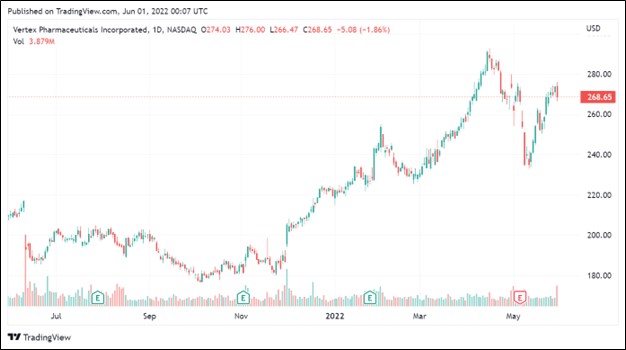

Image Shown: Shares of Vertex Pharmaceuticals Inc have surged higher over the past year. We continue to like the biotech firm in our Best Ideas Newsletter portfolio.

By Callum Turcan

The biopharmaceutical space is full of attractive investment opportunities, though early-stage firms without commercialized drug portfolios are quite risky investments given their lack of meaningful revenues and sizable negative cash flows. Vertex Pharmaceuticals Inc (VRTX), on the other hand, has a commercialized portfolio of therapeutics that treat cystic fibrosis (‘CF’) which enables the biotech firm to generate substantial revenues and cash flows. We include Vertex Pharma as an idea in the Best Ideas Newsletter portfolio.

Overview

Due to the asset-light nature of its business model (most expenses flow through R&D expense on the income statement and the firm does not have large capital expenditures in the ‘Investing’ section of the cash flow statement), Vertex Pharma’s capital expenditure requirements to maintain a given level of revenues are relatively modest, making free cash flows easier to come by. Vertex Pharma also has a fortress-like balance sheet. Its impressive financial strength enables the company to fund the development of several promising drug candidates without needing to issue debt or equity to meet its funding needs. The company’s drug development pipeline is robust, in our view, and we will cover some of its leading candidates in this article.

Update on VX-548

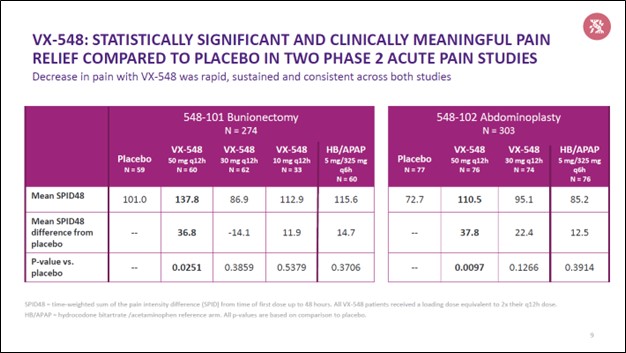

Shares of VRTX have been on a powerful upward climb of late as investors cheered on positive clinical trial data concerning its VX-548 drug candidate, which was announced in March 2022. VX-548 is a selective NaV1.8 inhibitor that, if successful, could represent a major breakthrough in acute pain treatment and management. Traditionally, pain treatment and management particularly for acute pain has been handled by opioids. However, given the high potential for abuse and the ongoing opioid epidemic, non-opioid pain treatment options such as the potential VX-548 treatment would represent a huge win not just for Vertex Pharma but society as well.

In our April 2022 article Best Biotech Idea Vertex Pharma Outperforming Struggling Peers, Its New Treatment for Pain a Game Changer in the Fight Against the Opioid Epidemic (link here), we covered this potential game changer in great detail. We encourage our members to check out that note.

Image Shown: An overview of the clinical trial data from Vertex Pharma’s VX-548 drug candidate, which if successful would represent a major breakthrough in the way health care providers treat pain, specifically acute pain. Image Source: Vertex Pharma – First Quarter of 2022 IR Earnings Presentation

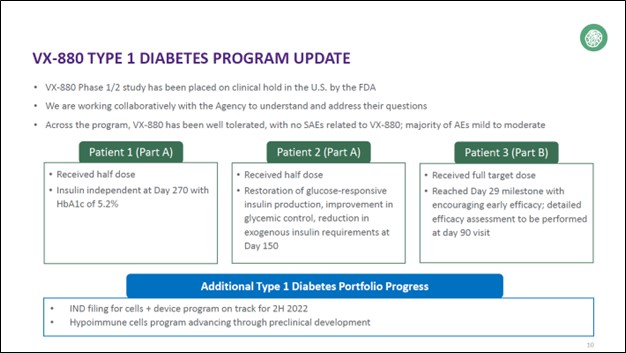

Update on VX-880

Another one of Vertex Pharma’s innovative drug candidates is VX-880. The investigative drug candidate is a potential cell replacement therapy for patients with Type 1 diabetes that have impaired hypoglycemic awareness and severe hypoglycemia. Here is a summary of the potential therapeutic, which is derived by stem cells:

VX-880 is an investigational allogeneic stem cell-derived, fully differentiated, insulin-producing islet cell therapy manufactured using proprietary technology. VX-880 is being evaluated for patients who have T1D with impaired hypoglycemic awareness and severe hypoglycemia. VX-880 has the potential to restore the body’s ability to regulate glucose levels by restoring pancreatic islet cell function, including glucose-responsive insulin production. VX-880 is delivered by an infusion into the hepatic portal vein and requires chronic immunosuppressive therapy to protect the islet cells from immune rejection.

Currently, VX-880 is undergoing Phase 1/2 clinical trials with Part A of this process involving two patients receiving half a dose and Part B is expected to involve five patients receiving the full dose. In May 2022, Vertex Pharma noted that “VX-880 [was] generally well tolerated in all three patients dosed to date” and that none of these patients had experienced serious adverse events (‘SAEs’) relating to VX-880 (there were some instances of SAEs which did not relate to VX-880).

Additionally, the firm noted that “the majority of adverse events (‘AEs’) were mild or moderate in all patients treated to date” and that “the data from the first two patients in Part A established proof-of-concept for VX-880” as the initial results in the first two patients were promising. However, the US Food and Drug Administration (‘FDA’) placed a clinical hold on trials conducted in the US involving VX-880 “due to a determination that there is insufficient information to support dose escalation with the product,” though that does not necessarily mean the drug candidate is flawed. Vertex Pharma is working with the US FDA to provide the necessary information so the clinical trials can resume in earnest. We hope that work on this potential therapeutic can resume in a timely manner.

Image Shown: An overview of Vertex Pharma’s innovative VX-880 drug candidate which aims to treat patients with Type 1 diabetes that have impaired hypoglycemic awareness and severe hypoglycemia. Image Source: Vertex Pharma – First Quarter of 2022 IR Earnings Presentation

Update on VX-147

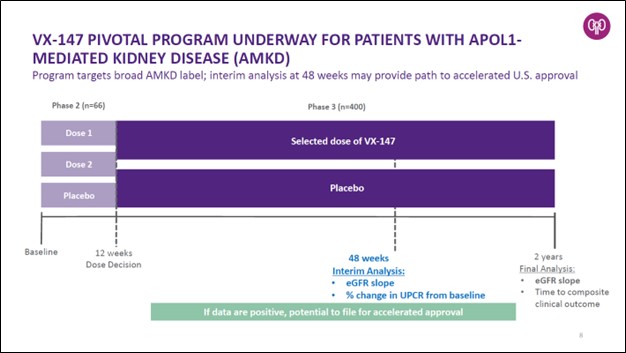

The drug candidate that is farthest along the clinical trial process and closest to potentially receiving regulatory approval is VX-147, an investigational therapy that aims to treat patients with proteinuric kidney disease mediated by two mutations in the APOL1 gene (‘AMKD’). According to Vertex Pharma, this disease impacts roughly 100,000 people in the US and Europe, its two key geographical markets (at least initially).

Vertex Pharma announced positive results from its Phase 2 clinical trials covering VX-147 in December 2021 which set the stage for the company to move towards “pivotal development” starting in the first quarter of 2022. In March 2022, Vertex Pharma announced its VX-147 drug candidate was getting ready to begin a Phase 2/3 clinical trial. According to Vertex Pharma, positive data from this clinical trial could lead to an accelerated approval from regulators, though nothing is for certain. We are keeping a close eye on its VX-147 drug candidate, and if successful, this would represent Vertex Pharma’s first commercialized drug outside of the CF realm.

By the end of March 2022, Vertex Pharma aimed to begin enrollment in the Phase 2/3 clinical trial. Here is what a March 2022 press release had to say on the matter:

The company will evaluate the safety and efficacy of VX-147 in a single pivotal clinical trial designed to assess the impact of VX-147, on top of standard of care, on kidney function and proteinuria in people with AMKD. The primary endpoint of this study is reduction in the rate of decline of kidney function as measured by estimated glomerular filtration rate (‘eGFR’) slope versus placebo at approximately two years. The study is also designed to have a pre-planned interim analysis at Week 48 evaluating eGFR slope in VX-147 versus placebo, supported by a percent change from baseline in proteinuria. If positive, the interim analysis may serve as the basis for Vertex to seek accelerated approval of VX-147 in the U.S. for patients with AMKD…

This randomized, double-blind, placebo-controlled Phase 2/3 adaptive study will first evaluate two doses of VX-147 for 12 weeks to select a dose for Phase 3 and subsequently evaluate the efficacy and safety of the single, selected dose in the Phase 3 portion of the study.

Patients aged 18 to 60 years, with two APOL1 mutations, urine protein to creatinine ratio (‘UPCR’) ≥0.7 g/g to <10 g/g, eGFR ≥25 to <75 mL/min/1.73m2 and on stable doses of standard of care medications are eligible to enroll. Approximately 66 patients are planned to be enrolled in the Phase 2 dose-ranging portion of the study, and approximately 400 additional patients are planned to be enrolled in the Phase 3 portion of the study.

The primary efficacy endpoint for the final analysis is eGFR slope in patients receiving the VX-147 selected dose compared to placebo. The secondary efficacy endpoint is time to composite clinical outcome, which will also be assessed at the final analysis and is defined as a sustained decline of ≥30% from baseline in eGFR, the onset of end-stage kidney disease (i.e., maintenance dialysis for ≥28 days, kidney transplantation or a sustained eGFR of <15 mL/min/1.73 m2) or death. The final study analysis will occur when subjects have at least two years of eGFR data and when approximately 187 composite clinical outcomes have occurred.

During Vertex Pharma’s latest earnings call, management stated that “it is really simply too early to comment on enrollment dynamics for VX-147” in response to an analyst’s question on the issue. However, management was clearly upbeat on the VX-147 drug candidate’s chances, and we are as well.

Image Shown: We are keeping a close eye on Vertex Pharma’s VX-147 drug candidate, which aims to treat patients with proteinuric kidney disease mediated by two mutations in the APOL1 gene. There are an estimated ~100,000 patients in the US and Europe that could benefit from this potential therapeutic. Image Source: Vertex Pharma – First Quarter of 2022 IR Earnings Presentation

Earnings Update

Vertex Pharma reported first quarter 2022 earnings on May 5 that beat top-line estimates but missed bottom-line estimates. The firm reiterated its full-year product revenue guidance for 2022, which closely tracks its overall revenue performance. Sales of its CF drug portfolio, represented by its TRIKAFTA/KAFTRIO, SYMDEKO/SYMKEVI, ORKAMBI, and KALYDECO therapeutics, were up 22% year-over-year last quarter. Revenue growth helped its GAAP operating income to rise by 17% year-over-year last quarter, as Vertex Pharma aggressively stepped up its investments in R&D while its other corporate-level expenses increased moderately. Its R&D expenses grew by 32% year-over-year last quarter and represented 29% of its total revenues during this period.

Launching TRIKAFTA/KAFTRIO in several international markets was key to supporting its sales growth last quarter, as its product revenues in international markets rose 55% year-over-year in the first quarter and were up 9% in the US. The European Commission (‘EC’) approved the use of KAFTRIO in combination with Ivacaftor (its brand name is KALYDECO) to treat CF in patients aged 12 and older in August 2020. In January 2022, the EC approved the use of KAFTRIO to treat CF in children aged 6-11 in combination with Ivacaftor (KALYDECO). These positive regulatory developments helped Vertex Pharma further grow the reach of its CF therapeutic portfolio.

The US, by far remains its largest market in terms of product revenues, and was the source of just under two thirds of Vertex Pharma’s $2.1 billion in total GAAP revenues last quarter. In June 2021, the US FDA approved TRIKAFTA for use in children aged 6-11 to treat CF which supported Vertex Pharma’s domestic performance. A combination of Vertex Pharma’s ample pricing power and efforts to expand the patient pool that can utilize its CF drug portfolio underpins its medium-term growth runway.

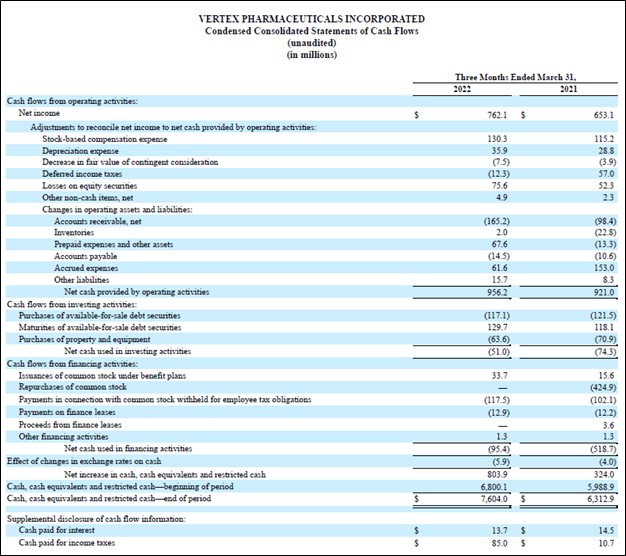

Vertex Pharma generated $0.9 billion in free cash flow during the first quarter and did not repurchase a significant amount (or any) through its share repurchase program (though it did spend $0.1 billion on ‘payments in connection with common stock withheld for employee tax obligations’). The company does not have a common dividend program at this time. While Vertex Pharma launched a share buyback program with $1.5 billion in repurchasing capacity last year, its strong stock price performance of late has apparently encouraged management to conserve cash.

Image Shown: Vertex Pharma has a stellar cash flow profile given its tremendous net operating cash flow generating abilities and modest capital expenditure requirements to maintain a given level of revenues, a product of its asset-light business model. Image Source: Vertex Pharma – 10-Q SEC filing covering the First Quarter of 2022

At the end of March 2022, Vertex Pharma had $8.2 billion in cash, cash equivalents, and current marketable securities with no short-term debt and $0.5 billion in long-term finance lease liabilities. The firm also had modest amounts of other non-cancellable financial liabilities on the books at the end of this period. Vertex Pharma’s fortress-like balance sheet represents one of the reasons we are huge fans of the biotech company.

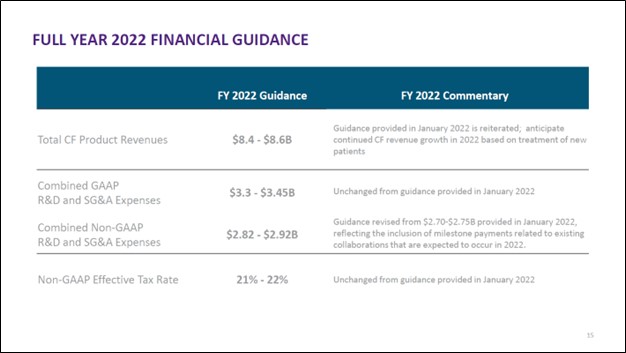

Looking ahead, Vertex Pharma aims to generate $8.4-$8.6 billion in total CF product revenues this year. At the midpoint, that represents 12% year-over-year growth. We appreciate that Vertex Pharma’s commercialized CF drug portfolio remains in high demand. The firm also adjusted its non-GAAP R&D and SG&A expense guidance for 2022 slightly higher versus previous expectations to reflect milestone payments expected to occur this year. We appreciate that Vertex Pharma has a robust development pipeline and that its collaborations are progressing favorably.

Vertex Pharma is quite active in the CRISPR gene editing space and we covered its exposure to this area in great detail in our August 2021 article Best Idea Vertex Pharma Marching Forward with Innovative CRISPR Technology (link here) that we encourage our members to check out.

Image Shown: Vertex Pharma’s guidance for 2022 indicates its growth story is expected to continue in earnest this year. Image Source: Vertex Pharma – First Quarter of 2022 IR Earnings Presentation

Concluding Thoughts

We are impressed with Vertex Pharma’s performance of late and appreciate that its drug development pipeline is steadily progressing in the right direction. The company’s relentless focus on innovation is clearly paying off. Our fair value estimate for Vertex Pharma sits at $270 per share, and the top end of our fair value estimate range sits at $365 per share. Vertex Pharma’s stock price has been on a nice upward trend over the past year, and we see room for shares of VRTX to potentially run significantly higher going forward.

—–

Health Care Bellwethers Industry – JNJ, WBA, CVS, ISRG, MDT, ZBH, BAX, BDX, BSX, MTD, SYK, BIIB, GILD, ABT, ABBV, LLY, AMGN, BMY, MRK, PFE, VRTX, ZTS, REGN, UNH

Related: XLV

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares in DIS, FB, GOOG, VRTX, and XLE and is long call options on DIS and FB. Johnson & Johnson (JNJ) and Health Care Select Sector SDPR Fund (XLV) are both included in Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Vertex Pharmaceuticals Inc (VRTX) is included in Valuentum’s simulated Best Ideas Newsletter portfolio. UnitedHealth Group Inc (UNH) is included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.