Image Shown: Shares of Lululemon Athletica Inc are recovering in the wake of the company’s recent earnings report.

By Callum Turcan

On March 29, Lululemon Athletica Inc (LULU) reported fourth quarter earnings for fiscal 2021 (period ended January 30, 2022) that matched consensus top-line estimates and beat consensus bottom-line estimates. Lululemon also announced it had initiated a new $1.0 billion stock buyback program after completing its previous program in the first quarter of fiscal 2022. The company issued favorable guidance for fiscal 2022 during its latest earnings update, which helped drive shares of LULU sharply higher during normal trading hours on March 30. Shares of LULU are up more than 20% during the past 52 weeks through the time of this writing, more than doubling the return of the S&P 500 during that time. We value shares north of $400 each at the time of this writing, revealing significant potential upside should price-to-fair value estimate convergence materialize.

Earnings Update

This fiscal year, Lululemon forecasts it will grow its revenues 20%-22%, to ~$7.5-$7.6 billion, after growing its GAAP net sales 42% in fiscal 2021 on an annual basis. Lululemon’s success is partially a result of its “Power of Three” strategy announced back in April 2019, which centers on product innovation (growing its men’s athleisure business while building on the strength of its women’s athleisure business), omni guest experiences (growing its e-commerce business and improving its digital operations to support omnichannel sales growth), and market expansion (growing its international business with an eye towards China while improving on its strong market position in the US and Canada).

Lululemon noted that its direct-to-consumer (‘D2C’) net revenue grew by 22% annually in fiscal 2021 after more than doubling in fiscal 2020. D2C sales represented 44% of its total net revenue in fiscal 2021. Lululemon’s company operated store net revenue grew by 70% annually in fiscal 2021 as customers returned to its stores in the wake of coronavirus (‘COVID-19’) pandemic-related lockdown measures easing up in regions worldwide.

The company has been steadily expanding the reach of its Fabletics brand by growing the brand’s footprint in physical retail stores and building up its e-commerce presence. For reference, this is a brand that sells cheaper athleisurewear offerings than Lululemon’s namesake brand and caters to the “body positivity” trend (meaning inclusive apparel across different body types). Another example of Lululemon’s product innovation is the recent launch its first footwear products which supports its longer term growth outlook.

Upside from these initiatives are more than offsetting headwinds created by supply chain hurdles, inflationary pressures, and the pandemic, at least so far. Lululemon’s GAAP gross margin rose to 57.7% in fiscal 2021, up ~170 basis points year-over-year, highlighting its pricing strength and the upside from growing economies of scale. The company’s GAAP operating margin rose to 21.3% in fiscal 2021, up ~270 basis points year-over-year, as its SG&A expenses grew at a slower pace than its revenue.

Its GAAP diluted EPS rose to $7.49 in fiscal 2021, up from $4.50 in fiscal 2020. Looking ahead, Lululemon aims to post $9.15-$9.35 in diluted EPS this fiscal year, which at the midpoint represents 23% year-over-year growth.

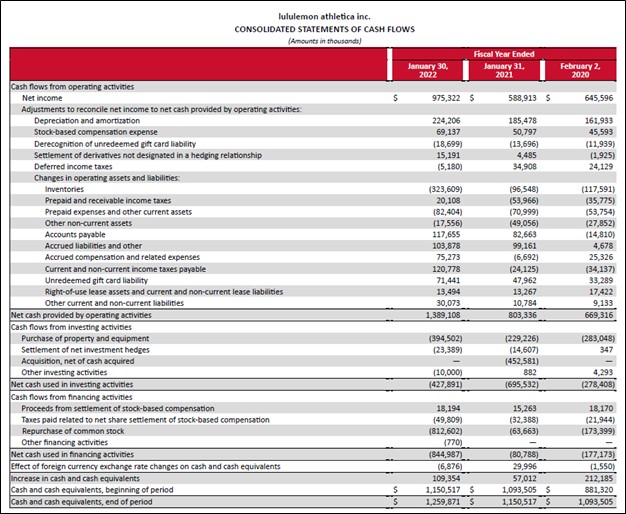

Lululemon has a tremendous cash flow profile. In fiscal 2021, it generated $1.0 billion in free cash flow (up from $0.6 billion in fiscal 2020) and spent $0.8 billion buying back its stock. The company does not have a common dividend program at this time.

Image Shown: Lululemon’s strong free cash flow generating abilities effectively fund its share buyback programs. Image Source: Lululemon – Fiscal 2021 10-K SEC Filing

Furthermore, Lululemon has a pristine balance sheet with $1.3 billion in cash and cash equivalents and no debt on the books at the end of fiscal 2021. The company does have other non-cancellable financial obligations to be aware of such as ‘current lease liabilities’ and ‘non-current lease liabilities,’ which combined stood at $0.9 billion at the end of fiscal 2021, though its cash-like position more than offset those liabilities.

Management Commentary

During Lululemon’s latest earnings call, its management team had some important commentary to provide on the firm’s supply chain hurdles, inventory mix, and pricing power (emphasis added):

“Shifting to the supply chain, we continue to experience delays across our global network, particularly related to transporting our products via ocean freight. As a result, we continue to lean more heavily into air freight. However, I am pleased with how our teams have become increasingly adept at navigating these challenges. We have implemented several strategies to ensure we have the proper levels of inventory to fuel our top line growth.

And as I have stated on prior calls, our core seasonless product makes up a meaningful percentage of our inventory, approximately 45%, which carries minimal markdown risk and positions us well to fulfill ongoing and future guest demand…

When looking at pricing, we continue to be strategic. We plan to take some selective price increases over the course of the year on a small portion of our styles. Our pricing also factors in the value of our innovation and we will continue to monitor the competitive environment to ensure we maintain our price position relative to our key peers.” — Calvin McDonald, CEO of Lululemon

During the earnings call, management appeared confident that planned product pricing increases and Lululemon’s position at the higher end of the athleisurewear market would help the firm maintain its strong margin performance seen of late. We caution that rising logistics expenses due to the surge in fuel prices seen over the past few months and Lululemon’s reliance on air freight will pressure its margins in the near term, though it has levers to pull to offset those hurdles.

Concluding Thoughts

Shares of LULU started moving precipitously lower in December 2021 before staging a meaningful recovery in March 2022. As of this writing, Lululemon is converging towards our fair value estimate as investors are warming back up to its multipronged growth story which underpins its promising free cash flow growth runway. Inflationary pressures and supply chain hurdles remain, but the company has done a stellar job navigating those headwinds while keeping its rock-solid financials intact. Shares continue to have upside potential on the basis of our fair value estimate.

—–

Discretionary Spending Industry – ATVI, BBY, CBRL, CMG, DIS, DG, DLTR, DPZ, EL, F, GM, HAS, HD, LOW, MCD, NFLX, NKE, SBUX, TSLA, YUM, DKS, TJX, ROST, WHR, KMX, AZO, RL, ULTA, LEG, GPC, VFC, CTAS, WSM

Tickerized for NKE, ADDYY, LULU, DKS, FL, SPWH, HIBB, UA, UAA, FXI, MCHI

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares of DIS, FB, XLE and is long call options on DIS and FB. Berkshire Hathaway Inc Class B shares (BRK.B), Chipotle Mexican Grill Inc (CMG), Dollar General Corporation (DG), Domino’s Pizza Inc (DPZ) and The Walt Disney Company (DIS) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. Dick’s Sporting Goods Inc (DKS) and Home Depot Inc (HD) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.