Image Shown: PepsiCo Inc is adeptly navigating various inflationary, labor, and logistical hurdles. Investors have started to warm back up to the name and its impressive pricing power over the past several months.

By Callum Turcan

On October 5, beverage and snack giant PepsiCo Inc (PEP) reported third-quarter earnings for fiscal 2021 (period ended September 4, 2021) that beat both consensus top- and bottom-line estimates. PepsiCo also raised its full-year guidance for fiscal 2021 in conjunction with the report.

Earnings Snapshot

The firm’s GAAP revenues grew by 12% year-over-year and its GAAP operating income climbed higher 5% year-over-year in the fiscal third quarter. Strength at PepsiCo’s snacks and beverage business in the Americas, Africa, Middle East, and Asia was key, particularly as it concerns growing PepsiCo’s operating income, as its business in Europe faced meaningful inflationary pressures.

Its outperformance in key markets around the world last fiscal quarter gave PepsiCo the confidence to push through a nice guidance boost. PepsiCo’s new guidance for fiscal 2021 shifted its expected non-GAAP organic revenue growth higher by 200 basis points versus its previous guidance, while its non-GAAP adjusted EPS forecasts left the door open for potential upside:

For fiscal year 2021, the Company now expects to deliver approximately 8 percent organic revenue growth (versus our previous guidance of 6 percent), at least 11 percent core constant currency EPS growth (versus our previous guidance of 11 percent), and at least 12 percent core EPS growth (versus our previous guidance of 12 percent).

In our view, it appears that strong organic volume growth and meaningful pricing increases (two concepts we will cover in just a moment) are enabling PepsiCo to hold the line as it concerns its forecasted bottom-line performance. PepsiCo expects to post non-GAAP core EPS of $6.20 in fiscal 2021 versus $5.52 in fiscal 2020.

Pricing Increases and Organic Volume Growth

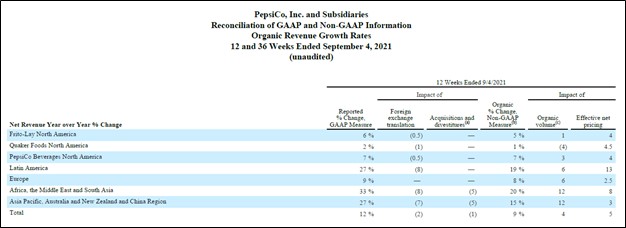

PepsiCo is facing major supply chain hurdles and inflationary headwinds. The firm’s performance in the fiscal third quarter was heavily aided by net pricing increases as one can see in the upcoming graphic down below. Organic volume growth came in relatively strong at most of PepsiCo’s segments in the wake of these pricing increases, indicating demand for PepsiCo’s offerings remains robust. At its Quaker Foods North America segment, meaningful net pricing increases combined with the fading effects of the “pantry stockpiling” effect seen last year in the wake of the coronavirus (‘COVID-19’) pandemic saw this segment’s organic volumes shift lower year-over-year last fiscal quarter.

Image Shown: PepsiCo is turning to meaningful net pricing increases to offset inflationary headwinds, and its organic volume growth has held up relatively well so far in the wake of those pricing increases. Image Source: PepsiCo – Third Quarter of Fiscal 2021 Earnings Press Release

We are impressed with the organic volume growth PepsiCo put up last fiscal quarter in Latin America, Africa, the Middle East, and Asia when taking net pricing increases into account. PepsiCo’s North American operations (excluding its Quacker Foods segment) also put up decent organic volume growth in the wake of meaningful net pricing increases. During PepsiCo’s latest earnings call, management had this to say in response to a question from an analyst on inflationary headwinds, pricing increases, and how that would impact PepsiCo’s bottom-line (emphasis added):

“I think I would think about it this way; obviously, we’ve given you some pretty specific guidance in terms of where we would expect EPS to land for Q4. You know that we fore advise by 6 months to 9 months, those hedges that we had in the beginning of the year are starting to roll off, the new ones that are in place are higher costs.

We had shared on the last call, as well as in the prepared remarks today that we expect to be able to price through the inflation that we’re facing whether it be commodities inflation or other types of operating expense inflation. Some of that pricing occurred in the summer, much more of it is occurring in the fall in the beverage business and substantially all of it for 2021 in the snack food business is occurring really as we speak during these weeks right now.

You also know that we forwarded by that 6 months to 9 months out, so we will have a better handle on where exactly 2022 costs are going to land as we get into the first quarter of 2022. And I would expect this to price a bit more to be reflective of some of that sort finalization of costs during the course of 2022. So Q4, some of the pricing coming through, the balance of it coming in Q1 of 2022, and the EPS guidance is reflective of all of that.” — Hugh Johnston, Vice Chairman, Executive VP, CFO of PepsiCo

Given PepsiCo’s strong organic volume growth performance in the wake of recent pricing increases, it appears that consumers around the world are still willing to pay up for its products. Management intends to capitalize on this dynamic by pushing through additional pricing increases going forward as communicated in the above statement.

Innovation remains key here. PepsiCo is working with Boston Beer Company Inc (SAM) to produce an alcoholic version of PepsiCo’s popular Mountain Dew beverage, dubbed HARD MTN DEW, which is expected to have a 5% alcohol content by volume. This agreement was announced back in August 2021 and highlights PepsiCo’s focus on making the most of its top tier properties. Other innovations include the launch of Doritos Flamin’ Hot Limon and Doritos Cool Ranch chips that was announced back in January 2020, along with other products such as zero sugar offerings of its Mountain Dew beverages and Lay’s Cheddar Jalapeño chips which are relatively new additions to PepsiCo’s product lineup.

Financial Snapshot

The firm intends to spend $5.8 billion covering its dividend obligations in fiscal 2021 and $0.1 billion buying back its stock. PepsiCo noted that its share repurchase program for this fiscal year had been completed and that the firm did “not expect to repurchase any additional shares for the balance of [fiscal] 2021” in its latest earnings press release.

PepsiCo generated $4.4 billion in free cash flow during the first three quarters of fiscal 2021 while spending $4.3 billion covering its dividend obligations and another $0.1 billion buying back its stock. We appreciate management taking their foot off of the gas pedal as it concerns share repurchases given that PepsiCo exited the fiscal third quarter with a net debt load of $34.4 billion (inclusive of short-term debt). Shares of PepsiCo are trading in the upper bound of our fair value estimate range as of this writing (the top end of our fair value estimate range sits at $162 per share of PEP).

In our view, PepsiCo would be wise to pare down its net debt load over time. The firm is a stellar free cash flow generator with a stable business model that apparently has ample pricing power, and we expect PepsiCo will be able to stay on top of that burden going forward while continuing to make good on its dividend obligations. PepsiCo had a $6.9 billion cash, cash equivalents, and short-term investments balance at the end of the fiscal third quarter, providing the firm with ample liquidity to manage its near term funding needs.

Concluding Thoughts

Inflationary headwinds, labor constraints, and logistical hurdles are wreaking havoc across the globe, though PepsiCo appears to be fully capable of adeptly navigating these obstacles. The firm possess ample pricing power, aided by its focus on innovation in the beverages and snacks industry. PepsiCo is a tremendous cash flow generator in almost any operating environment. Shares of PEP yield a nice ~2.7% as of this writing.

We do not intend to add shares of PEP to any of our newsletter portfolios at this time, though we do include Vanguard Consumer Staples Index Fund ETF (VDC) in the High Yield Dividend Newsletter portfolio (more on that here) to gain exposure to top tier consumer staples names. Over the long haul, we expect the global economy will be able to push past recent headwinds, though meaningful hurdles remain. Please note we added long put options on the SPDR S&P 500 ETF Trust (SPY) to both the Best Ideas Newsletter portfolio and Dividend Growth Newsletter portfolio on October 4 as “protection” against rising near term volatility in US equity markets (more on that here).

Note the High Yield Dividend Newsletter is only available via email.

—–

Recession Resistant Industry – BUD, CL, CLX, CPB, COST, FDP, GIS, HRL, K, KDP, KHC, KMB, KO, KR, MDLZ, MKC, MO, PEP, PG, PM, SJM, TAP, TGT, TSN, WMT, CHD, SYY, ADM, LANC, CASY

Tickerized for PEP, KO, SAM, SPY, VDC, STZ, BUD, TAP, PG, OTLY, ZVIA, KDP, NAPA, GIS, KHC, AMPL, CAG, POST, BGS, TWNK, SJM, HAIN, BRBR, CPB, CELH, MNST, PBJ

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Philip Morris International Inc (PM) and Vanguard Consumer Staples ETF (VDC) are both included in Valuentum’s simulated High Yield Dividend Newsletter portfolio. Long put options on the SPDR S&P 500 ETF Trust (SPY) with an expiration date of December 31, 2021, and strike price of $412 are included in both the simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.