Image Source: Merck & Co Inc – IR Presentation

By Callum Turcan

Pharmaceutical giant Merck (MRK) has performed well during the past few fiscal years by reducing operating costs while utilizing strong growth at some of its oncology drug offerings to drive sales higher. Shares of Merck yield 2.7% as of this writing and are trading at the upper half of our fair value estimate range after an impressive run up in Merck’s stock price began in April 2018. Management recently raised Merck’s full-year sales and non-GAAP EPS guidance for 2019, which we will cover in a moment.

Enhancing Profitability Levels

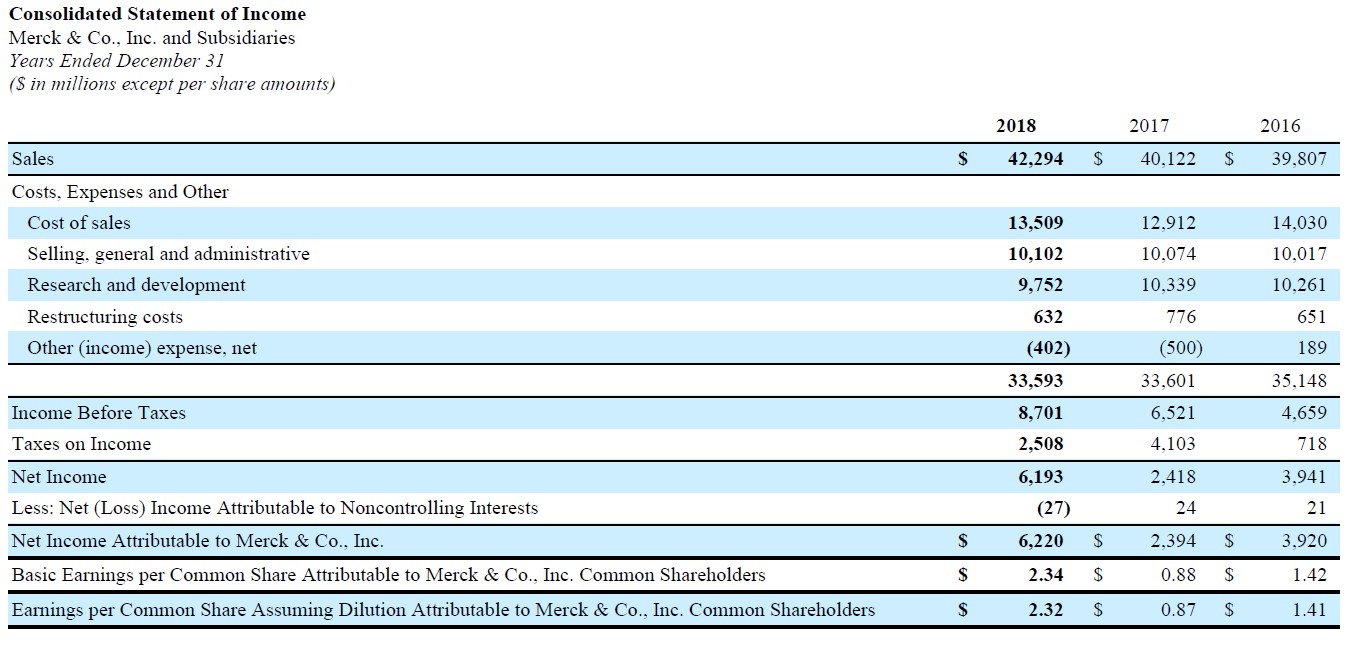

From 2016 to 2018, Merck cut its GAAP operating expenses from $35.1 billion to $33.6 billion (down over 4%) as you can see in the graphic below. The pharmaceutical giant’s GAAP revenue expanded from $39.8 billion to $42.3 billion (up over 6%) during this period. Reductions in the company’s R&D spending combined with controlled SG&A expenses allowed for Merck’s GAAP operating margin to expand by over 885 basis points from 2016 to 2018, hitting ~20.6% last year. Regarding revenue growth, sales of Merck’s KEYTRUDA drug (helps fight certain cancers) skyrocketed from $1.4 billion in 2016 to $7.2 billion in 2018 while growth at its animal health segment was also particularly strong (both livestock and companion animal related sales were up).

Image Shown: Merck has meaningfully reduced its operating expenses over the past few fiscal years while still being able to grow its top line, resulting in material operating income growth. Image Source: Merck – 2018 Annual Report

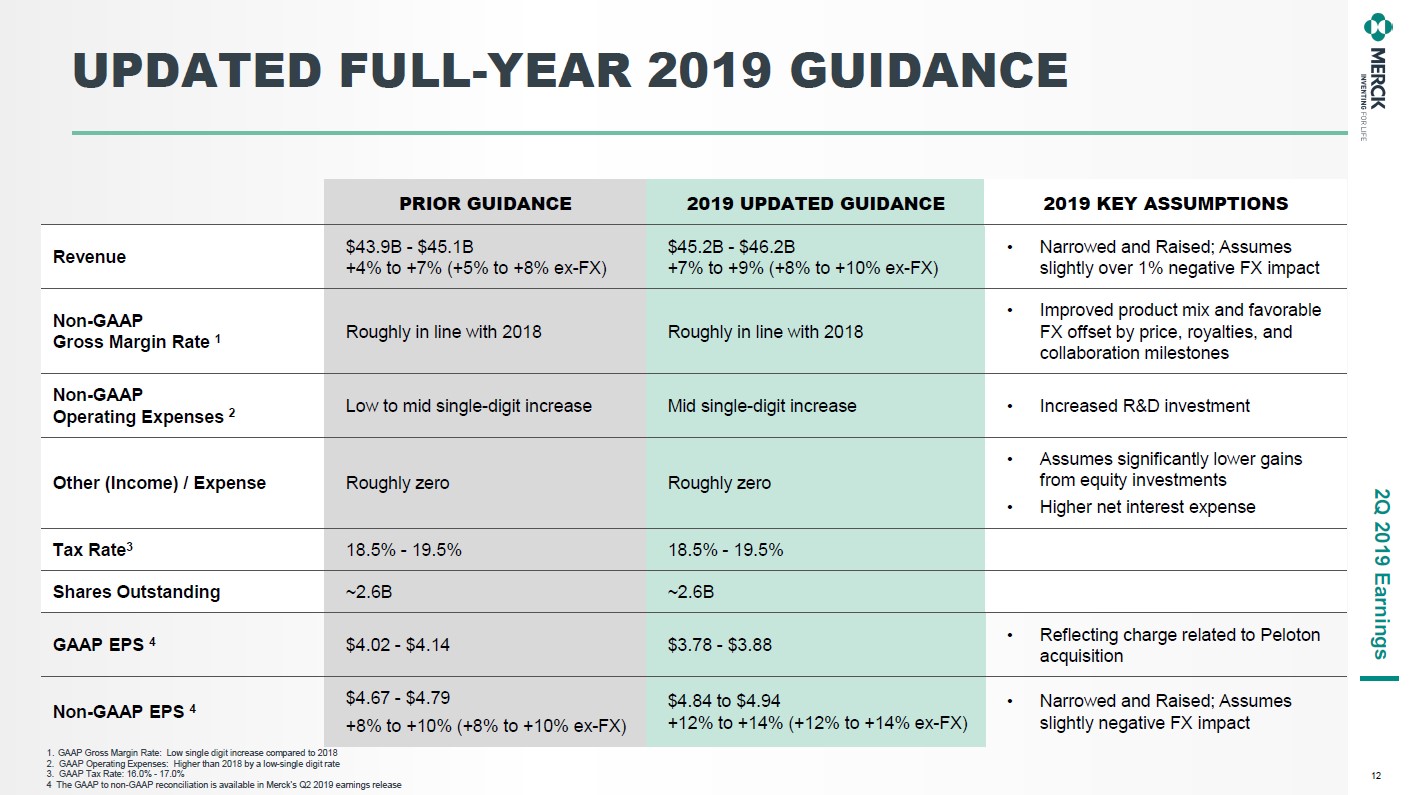

Going forward, Merck sees strong sales at its oncology division including; KEYTRUDA (used to treat melanoma, non-small cell lung cancer, and other types of cancer), LYNPARZA (used to treat advanced ovarian cancer, fallopian tube cancer, and primary peritoneal cancer), and LENVIMA (used to treat thyroid cancer, certain kidney and livers cancers, and potentially other cancers) driving its top line and ultimately profits higher. Down below is a look at Merck’s revised guidance for 2019 (management increased Merck’s full year revenue and non-GAAP EPS forecast during the firm’s second quarter earnings report on July 30). Merck is targeting high single-digit top line growth and double-digit non-GAAP EPS growth in 2019 on an annual basis.

Image Shown: Merck is targeting meaningful revenue and non-GAAP EPS growth this year, and management recently raised the pharmaceutical giant’s full-year guidance for 2019. Image Source: Merck – IR Presentation

We generally like the structure of the big pharmaceutical industry and think the space allows for companies to generate meaningful shareholder value. Down below is a concise summary of how we view the industry:

“The big pharma industry is primarily composed of makers of branded drugs. Intellectual property protection is vital to the successful commercialization of medicines and offers makers of branded drugs a unique competitive advantage via patents, which can extend for decades. When branded drugs lose market exclusivity, however, makers of generic pharmaceuticals can generate intense price competition, causing drastic revenue losses on unprotected therapies. Long-term success for branded pharma companies depends on a strong and diverse drug pipeline, which can be augmented by M&A activity. We generally like the group and expect continued industry consolidation.”

Last year, Merck generated $8.3 billion in free cash flow which easily covered $5.2 billion in dividend payments. Over the past three full fiscal years, Merck’s average annual free cash flows stood at $7.2 billion while its average annual dividend commitments came in at $5.2 billion. We give Merck a Dividend Cushion Ratio of 1.9x due to its strong free cash flows, but caution that its net debt load of $19.5 billion at the end of June 2019 weighs negatively on Merck’s ability to raise its payout. The company has also historically spent a lot on share buybacks, including $9.1 billion in 2018, which consumes cash that could be used to strengthen the balance sheet or boost dividend payments per share.

Bolstering Merck’s Drug Pipeline

In May 2019, Merck agreed to acquire all of the outstanding shares of Peloton Therapeutics for $1.05 billion in cash upfront along with $1.15 billion in contingent payments if certain regulatory and sales milestones are met. Please note that this deal was to bulk up Merck’s oncology drug pipeline and that the transaction closed in July 2019. Merck noted that:

“…privately held Peloton [is] a clinical-stage biopharmaceutical company focused on the development of novel small molecule therapeutic candidates targeting hypoxia-inducible factor-2α (HIF-2α) for the treatment of patients with cancer and other non-oncology diseases. Peloton’s lead candidate is PT2977, a novel oral HIF-2α inhibitor in late-stage development for renal cell carcinoma (RCC).”

Furthermore, Merck agreed to acquire all of the outstanding shares of Tilos Therapeutics in June 2019 for just under $0.8 billion along with contingent payments if certain milestone are met. That deal was also about bolstering Merck’s oncology and other drug pipelines but no closing date was given in the press release (and the deal wasn’t mentioned, at least not directly, in Merck’s 10-Q filing for the second quarter of 2019). Merck noted that:

“…Tilos Therapeutics [is] a privately held biopharmaceutical company developing therapeutics targeting the latent TGFβ complex for the treatment of cancer, fibrosis and autoimmune diseases.”

While Merck cut its R&D spending over the past few fiscal years (management noted the company planned “increased R&D investment” in 2019), management is using those savings to acquire very promising potential drug candidates.

Concluding Thoughts

Merck is improving its financials and we like that, but we still aren’t interested in shares after the run up during the past year and a half. The pharmaceutical giant’s net debt load is manageable given its strong free cash flows, but dividend growth will require share buybacks to be pared back first in order to make room for payout growth. It will take some time until we get an idea of how well Merck’s recent acquisitions pan out.

Check out Merck’s supplemental two-page Dividend Report here —->>>>

Pharmaceuticals (Big) Industry – ABT ABBV AMGN AZN BMY LLY GSK MRK NVS NVO PFE SNY

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.