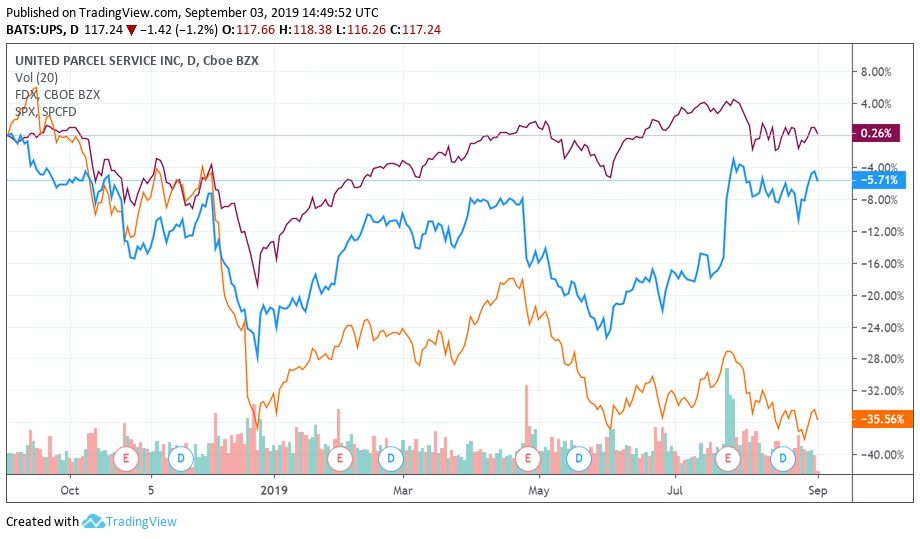

Image Shown: Shares of both FedEx Corporation (FDX) (indicated by the orange line above) and United Parcel Service Inc (UPS) (indicated by the blue line above) have come under a tremendous amount of pressure over the past year as the industry navigates the fallout from the US-China trade war. Both companies are investing heavily to improve their offerings to stay ahead of the game as large tech companies increasingly encroach on the shipping industry’s traditional turf. The S&P 500 index is indicted by the purple line above.

By Callum Turcan

The past year has not been kind to the air freight and logistics industry. The price of shares of FedEx Corp (FDX) have fallen by more than a third during the past twelve months, as of this writing. Though shares of United Parcel Service (UPS) have fared better after climbing higher in recent months, the company’s shares have still underperformed the broader market as of this writing, even when taking dividends into account. Other shipping and logistics companies such as XPO Logistics Inc (XPO) and C.H. Robinson Worldwide (CHRW) have also seen their share prices come under intense pressure. Concerns over the synchronized slowdown in global economic activity combined with rising geopolitical tensions have clearly weakened investor sentiment towards these companies. Though we like aspects of the industry, please note that there’s a reason why these companies are not included in our Best Ideas Newsletter and Dividend Growth Newsletter portfolios at this time. Here’s how we view the space:

“The highly competitive air freight and logistics industry is heavily tied to cyclical domestic economic expansion (primarily from retail good shipments). The international freight market remains a critical growth engine for air cargo providers, while all constituents deal with the cost of rising fuel (diesel) prices and potentially price-sensitive demand during periods of economic weakness. Firms with freight-forwarding, asset-light operations and/or large difficult-to-replicate shipping networks can carve out sustainable competitive advantages while generating high returns on investment. We generally like the group.”

FedEx has been repeatedly accused by China of sending dangerous packages to China and Hong Kong, accusations that were brought forth after the company allegedly rerouted packages meant for embattled Huawei in China to facilities in America. Those headlines have played a role in depressing its stock price. The company is trapped between a rock and a hard place, the US and China, with no easy out as geopolitical tensions are spilling over into every segment of the global economy. We are monitoring the situation between FedEx and China. Please note that there’s a chance that, should geopolitical tensions continue escalating, that government authorities (particularly those in China) may decide to further pressure FedEx in unconventional ways.

Additionally, FedEx made waves this year when it decided to stop shipping Amazon’s (AMZN) packages, a relationship that was responsible for a very low single-digit percentage of its total shipment volume and revenue in 2018. That move was made so FedEx could work on its other relationships. Amazon is building out its own logistics and shipping infrastructure by expanding its warehouse footprint, acquiring a fleet of dozens of cargo planes, and bulking up its last-mile delivery operations. In the future, many (including us) see Amazon’s shipping and logistics operations catering to both in-house and third-party demand in large quantities. FedEx didn’t want to give Amazon a helping hand in that endeavor.

To replace Amazon and alter its growth trajectory, FedEx is working together with companies like Walmart (WMT) and Yum Brands’ (YUM) Pizza Hut on delivery robots. Last-mile delivery services involve transporting goods from warehouses to their final destination. However, the margins on residential delivery services are weaker than those achieved by delivering packages to convenience stores, given the need to make numerous stops just to deliver a small number of packages relative to what a semi-truck could haul in to one location. Delivery robots could change that.

For UPS, its relationship with Amazon represents a much bigger slice of its revenue and shipment volumes. UPS derives a high-single-digit percentage of its annual revenue from Amazon and handles a sizable chunk of the e-commerce giant’s total shipments. While UPS is very much exposed to Amazon’s long-term strategies, for better or worse, UPS is making major investments in self-driving trucks and drones to stay ahead. Rolling out those options should provide for a much stronger last-mile and freight offering to existing and potential clients.

Drones could be used to meet same-day or next-day delivery obligations, picking up packages at warehouses and delivering them to consumers without the need for any more human involvement. For freight, the trucking industry has been stymied by a relative lack of labor, a problem which could be mitigated through autonomous or semi-autonomous vehicles (something that’s still in the design and pilot project phase).

Even with these initiatives in mind, UPS is still facing an uphill climb as Amazon is making a big push into last-mile delivery logistics. That strategy involves Amazon acquiring an enormous fleet of vans (~20,000) from Mercedes-Benz, owned by Daimler AG (DMLRY), and encouraging its employees to start their own delivery company. Also, Amazon plans to almost double its cargo plane fleet in the next few years (from 39 to 70 by 2021). These types of investments are made possible in part through the impressive cash flows churned out by Amazon’s cloud-computing AWS segment.

On the other hand, please keep in mind UPS operates ~500 cargo planes and FedEx operates ~700 cargo planes. Air freight is where the traditional shipping companies continue to retain two key advantages over Amazon, scale and expertise. Over time, however, Amazon is likely to keep expanding in this space as the prevalence of e-commerce grows worldwide.

Concluding Thoughts

For now, the market seems to be giving UPS the benefit of the doubt and has started bidding its stock back up over the past few months. For FedEx, the market is concerned that the spillover effects from the US-China trade war and lack of upside via Amazon’s impressive growth story will hurt the shipping company’s future performance. Our fair value estimate for UPS stands at $114/share, just below where shares are trading at as of this writing.

Our fair value estimate for FedEx stands at $196/share, well above where shares are trading as of this writing. FedEx is trading below the low end of our fair value range, indicating a possible mispricing. However, we aren’t interested in FedEx either as the market is clearly pricing in geopolitical and other concerns that could hurt its future financial performance, something very difficult to capture within enterprise valuation processes.

We like companies that are undervalued on a discounted cash-flow basis, are trading at a relative discount to peers, and whose share prices are advancing, as the latter indicates what we believe to be an increased likelihood of price-to-intrinsic value convergence. After all, the stock price eventually has to start “going up” for price-to-intrinsic value convergence to occur. Why not just wait for it to start advancing before considering the position, instead of trying to catch a falling knife.

Air Freight & Logistics Industry – CHRW EXPD FDX ODFL UPS

Related: IYT

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.