Image Source: J. M. Smucker Company – IR Presentation

By Callum Turcan

J. M. Smucker Company (SJM) is known for its peanut butter (sold under such brands as Jif and Adams), jams (including its namesake Smucker’s offering and Knott’s Berry Farm products), coffees (such as Folgers and Café Bustelo), pet products (including Nature’s Recipe and Meow Mix), and more. The firm posted first quarter earnings for FY2020 (quarter ended July 31) on August 27 that upset the market and sent shares down more than 8% that day. Smucker’s revenue and earnings both missed estimates while management lowered the firm’s full year guidance for fiscal 2020.

Smucker now expects its FY2020 EPS to come in at $8.35-$8.55/share, down from $8.45-$8.65/share previously. Furthermore, net sales are now expected to either drop by 1% or come in flat year-over-year in FY2020 while previously, Smucker Company’s forecasted a 1% to 2% year-over-year increase in its net sales. We can understand why shares of SJM sold off aggressively and we aren’t interested in adding the company to either newsletter portfolio.

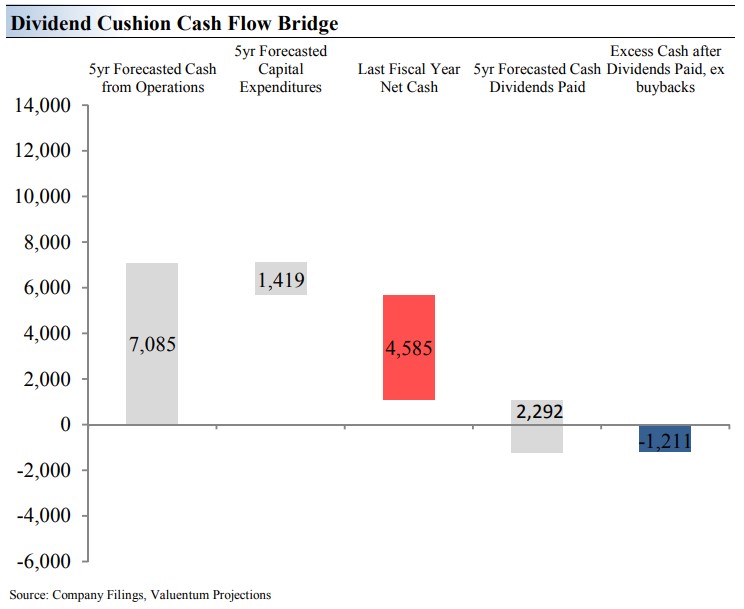

We have lowered our fair value estimate for Smucker to $107 per share from $109/share previously, after the report. Shares of SJM now trade just below that level as of this writing indicating Smucker Company’s equity is fairly valued. We caution Smucker Company’s dividend coverage is very weak as its Dividend Cushion ratio stands at just 0.5x (note the ‘Dividend Cushion Cash Flow Bridge’ in the image below. While a lower interest rate environment will likely help Smucker retain access to capital markets at more attractive rates, as will its Baa2 investment grade credit rating from Moody’s Corporation (MCO), please note its large net debt load poses a serious threat to its future dividend payouts should its financial performance significantly weaken. Shares of SJM yield ~3.3% as of this writing.

Image Source: SJM’s Dividend Report

Management is addressing this issue through deleveraging efforts. In FY2020, Smucker Company aims to pay down an additional $400 million in debt by the end of the year through expected free cash flow generation. Free cash flows in FY2020 are forecasted by management to come in at $875-$925 million. Last quarter, management noted Smucker Company paid down $130 million in debt and that the firm’s leverage ratio (debt to EBITDA) stood at 3.6x, which will come down to just above 3.0x by the end of FY2020. We would like to see that climb down even lower but appreciate Smucker Company’s deleveraging strategy.

Keep in mind that per share dividend growth is slowing down to make room for deleveraging efforts at Smucker. Companies with large net debt loads (outside of the REIT or utility space) find it increasingly hard to sustainably grow their payouts at a meaningful rate. This is why net cash positions are a great addition to any income growth thesis as strong balance sheets support future per share payout growth (instead of detracting from in the case of net debt positions).

Problems Widespread

Smucker Company reported weakness across the board last quarter. Excluding the favorable impact from an acquisition, the firm’s US Retail Pet Food division saw revenue move lower by $27 million year-over-year (down ~4%) as the unfavorable impact of volume/mix (reduced segment sales by 600 basis points) more than offset the favorable impact from rising net price realizations (increases segment sales by 200 basis points). Part of the decline was due to Smucker exiting low margin products, which we can appreciate, but this weakness was also due to “soft trends at certain retailers” which is worrisome.

The firm’s US Retail Coffee division saw revenue decrease by $24 million year-over-year (down ~5%) due to unfavorable volume/mix (reduced segment sales by 200 basis points) and unfavorable net price realizations (reduced segment sales by 300 basis points). Weakness at its Folgers brand was largely to blame.

Pivoting to its US Retail Consumer Foods division, Smucker reported an $11 million drop in revenue year-over-year (down ~3%) when factoring out the impact of divestments. Lower net price realizations, primarily for its Jif products after a significant price markdown, reduced the segment’s net sales by 400 basis points year-over-year which was modestly offset by favorable net volume/mix effects adding 100 basis points to the segment’s net sales. Smucker Company recently announced that a new plant in Longmont, Colorado, is now operational which will reportedly double the production of its Smucker’s Uncrustables products. Rising availability of the Smucker’s Uncrustables offering are expected to pad the firm’s revenue trajectory going forward as you can see in the graphic below.

Image Shown: Smucker Company is targeting significant growth at its Smucker’s Uncrustables offering now that production of the snack is set to double. Image Source: Smucker Company – IR Presentation

Finally, Smucker wasn’t spared on the international front either. When removing the impact of divestments, net sales at its International and Away From Home segment dropped by $15 million year-over-year (down ~6%). That was partially due to negative foreign currency movements reducing revenue by $2 million. Additionally, unfavorable volume/mix effects shaved 300 basis points off the segment’s net sales year-over-year while lower net price realizations reduced segment revenue by 200 basis points, largely due to weakness at its Folgers offering.

Our biggest takeaway from Smucker’s first quarter FY2020 performance is that demand is weakening for its products. There are numerous ways the firm can fight back including stepping up marketing efforts or reducing prices further in a bid to bolster demand, but nothing comes for free. Organic net sales dropped 4% year-over-year in the first quarter FY2020 according to the firm.

Smucker’s organic net sales growth guidance for FY2020 (flat to 1% growth on an annual basis) is a tad more optimistic than its expected decline in net sales. That forecast relies heavily on a rebound at its US Retail Coffee segment that when combined with improving pet food and snack sales, will see Smucker Company post much stronger performance during the second half of FY2020. Smucker’s Uncrustables sales are expected to ramp up over the coming quarters now that its new production facility is operational. Here’s what management had to say on the firm’s coffee strategy, from Smucker Company’s latest quarterly conference call (emphasis added):

“With respect to the shortfall in U.S. Retail Coffee, we are confident that this was a temporary dynamic. While we expected a sales deceleration from the fourth quarter, the decline was greater than anticipated. This was partially due to timing of distribution gains across all formats that have shifted to the second quarter.

As part of this change, we gained incremental shelf space going forward across all formats. We are already seeing momentum build in the second quarter and continue to expect top- and bottom-line growth for the Coffee segment this fiscal year.

Our category leadership position remained strong. Along with the number one Folgers brand, Dunkin’ became the number three brand in retail sales during the quarter and continue to outpace category growth [Smucker Company has a partnership with Dunkin’ Brands Group Inc (DNKN)]. In addition, we own four of the top five brands growing household penetration in the coffee category, and our K-Cup [in partnership with Keurig Doctor Pepper Inc (KDP)] portfolio is outpacing category growth by approximately two times in the latest four, 12 and 52-week periods.”

Revenue growth is an essential part of Smucker’s strategy to become more profitable, as scale is required to keep costs contained relatively speaking (in regard to both gross and operating margins). Management is “pursuing cost management over the remainder of the year to deliver earnings growth, despite the decrease in (its) sales guidance” in order to offset top-line pressures. Cost savings programs represent a key part of Smucker’s long-term strategy to generate shareholder value. Please note that cutting down the firm’s debt load and likely reducing its interest expenses is another way management is enhancing Smucker Company’s cash flow profile.

Image Shown: Smucker Company is targeting ongoing improvements in its cost and capital structure to enhance its ability to reward shareholders over the long-term. That strategy requires management to resuscitate revenue growth at the company. Image Source: Smucker Company – IR Presentation

Concluding Thoughts

Management seems confident things will stabilize and begin to turn around in the coming quarters, and we will be waiting to see how that plays out. We strongly support Smucker’s deleveraging efforts but are staying far away from SJM as things stand today.

Food Products (Small/Mid-Cap) Industry – CALM DF FLO FDP HAIN HRL JJSF LANC MKC SJM THS TSN

Related – PEP KDP DNKN CHWY

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.