Image source: Intel analyst presentation

Shares of simulated newsletter portfolios idea Intel have faced material selling pressure in mid-2018 as a result of a number of reports of increased competition from rivals, namely AMD. We’re not worried and still like the company’s valuation profile.

By Kris Rosemann

Chip-making giant Intel’s (INTC) delays in its 10-nanometer chip program have the market concerned over its position relative to rivals such as Advanced Micro Devices (AMD), which is planning to launch its 7-nanometer chops in early 2019. Intel’s 10-nanometer are now not expected to be launched until late 2019 and likely won’t ship in material volume until 2020. Though the actual speed difference and overall performance between the two chips remain up for debate, in our view, market observers expect Intel’s delayed launch to result in an erosion of its market share.

The news surrounding Intel’s delays and AMD’s potential to grab share in the attractive data center market have sent shares of AMD considerably higher during the past several weeks, and we’ve raised our fair value estimate for AMD to $18 per share each, after upping our forecasts for top and bottom-line performance. We’re watching market-share developments between Intel and AMD closely, and another material fair value estimate increase may be in the cards for AMD in the not-too-distant future if the company proves that it might deliver expectations even greater than our current forecasts.

As many investors continue to focus on Intel’s arguable shortcomings in its next chip launch, Intel is still committed to making its current chips as competitive as possible. Management points to robust growth in its data-centric businesses, which saw revenue jump 26% on a year-over-year basis in the second quarter of 2018 (as evidence of its recent success in the area), and its plan moving forward will rely on its ability to “stitch together” its CPUs and memory chips.

Additional tweaks in Intel’s current chip lineup are expected to make it more competitive against the likes of Nvidia (NVDA) in artificial intelligence, which will require cost competitiveness along with robust levels of computing capacity to handle massive loads of data. We continue to like the potential of the recent Intel-Mobileye combination as it relates to artificial intelligence in the rapidly growing connected automotive space, a part of the reason Intel fancies itself as the “greatest data collector.”

Intel also believes it has an ace up its sleeve in a new memory chip technology it calls Optane, which it plans to pair with its processors in 2019, and expects to gain some capability above rivals as the technology has been built from scratch in-house. Management expects this, along with the aforementioned tweaks to its existing chips, to help its earnings growth continue outpacing the broader market as it gears up for its late 2019 10-nanometer chip launch. Intel remains focused on capturing a notable piece of the rapidly-growing data-centric opportunity it is being presented.

Intel’s CEO Search Weighing on Sentiment

We’re keeping an close eye on Intel’s ongoing CEO search, which was launched when Brian Krzanich stepped down from the role earlier this year after violating Intel’s non-fraternization policy and interim CEO (and current CFO) Bob Swan indicated he did not want the full-time position. The company has a strong internally-based executive succession history, but recent exits have left its C-suite depleted. The instability may not have been able to come at a worse time as Intel works to remain the leader in data-center chips, integrate multiple acquisitions, break into the mobile device market, and continue expansion into new businesses.

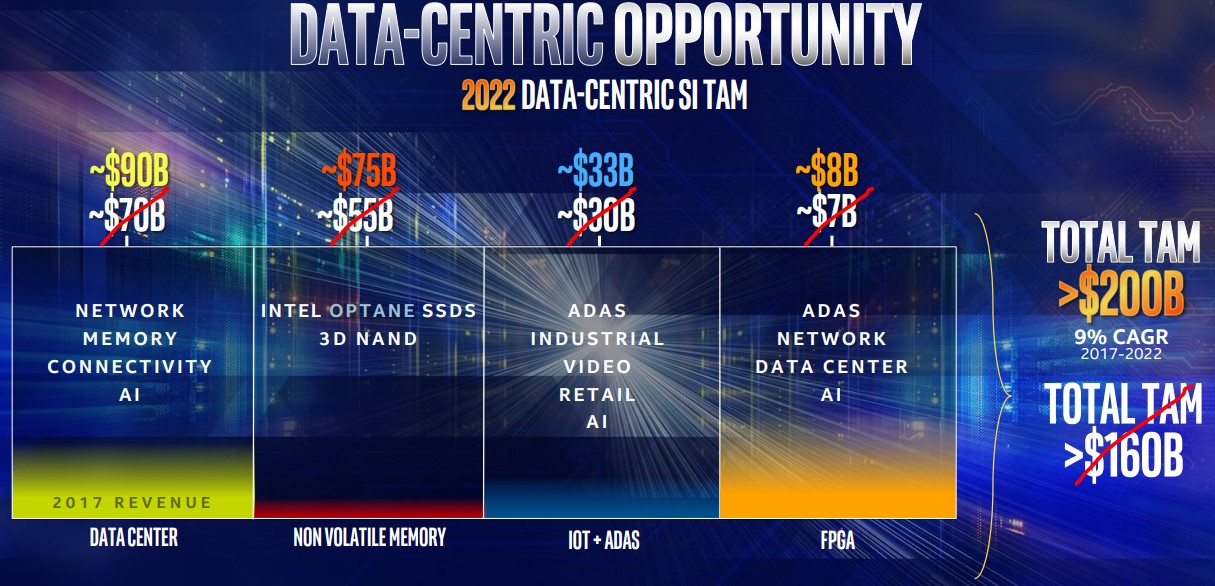

Our fair value estimate for Intel currently sits at $56 per share, and this estimate includes an assumption of revenue growth flat-lining at 3% in 2020 through the end of our 5-year discrete forecast horizon, expectations that may be considered modest given expectations for Intel’s 10-nanometer chips hitting the market in full force in 2020. Intel’s data-centric opportunities remain tremendous as well, and it expects its data-centric total addressable market to grow at a ~9% CAGR from 2017-2022 to more than $200 billion, up from previous estimates of $160+ billion in 2021.

Image source: Intel analyst presentation

Wrapping Things Up

AMD expects robust top-line growth in the near term, but it remains somewhat challenged in terms of profitability levels and cash flow generation (cash flow used in operations was $131 million in the first half of 2018). That may very well be beginning to change, however, as its growing businesses achieve economies of scale–the second quarter of 2018 marked its highest quarterly net income in seven years, for example. But Intel is no small foe. Nevertheless, AMD is already making its presence known in the data center space, and recent highlights of the business include platform deployments and commitments from industry leaders such as Hewlett Packard Enterprise (HPE), Cisco (CSCO), and Tencent (TCEHY).

Though we like AMD, its shares have gone too far too fast, in our view, and we continue to like the long-term opportunity Intel is presented with. Unlike AMD, Intel remains a robust free cash flow generator, which helps it achieve a strong Dividend Cushion ratio as cash dividends paid remain a fraction of free cash flow. Shares are currently changing hands at ~11.7 times management’s 2018 non-GAAP earnings guidance, which was raised following in its second quarter report amid “broad based business strength,” and ~11.3 times consensus estimates for 2019 non-GAAP earnings. We continue to like Intel as an idea in both simulated portfolios of the Best Ideas Newsletter and Dividend Growth Newsletter. Shares yield 2.5% at the time of this writing.

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Kris Rosemann does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.