Pizza chain Papa John’s continues to struggle through board room drama and other public relations headaches related to recent developments surrounding its founder and largest shareholder. The company cut its 2018 guidance in a material way in its second quarter report.

By Kris Rosemann

Public relations nightmares such as the situation currently surrounding Papa John’s (PZZA) are extremely rare and do not always result in a material tangible negative impact on a company’s financial performance, but this does not appear to be the case for the pizza chain. Founder John Schnatter made headlines after his comments on player protests in the National Football League, once a key partner for the company, on the third quarter 2017 earnings call, and he created an even larger firestorm in the summer of 2018 when reports surfaced of even more insensitive language used in a conference call in 2018.

Papa John’s has been working to cut ties with its founder, but as its largest shareholder (Schnatter owned ~29% of its common stock at the end of 2017), Schnatter has promised not to go away any time soon, a point he drove home in a recent open letter to management. Nevertheless, management hasn’t been shy about the events and their impact on the company’s financial performance. Multiple references to those aforementioned events as inflection points in its comparable sales performance in its 2018 second quarter conference call and a new marketing strategy made the executive suite’s opinions on the matter clear.

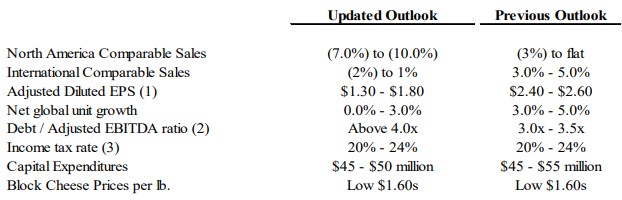

Management noted that comparable sales in North America in the month of July–the report regarding Schnatter’s second controversy surfaced July 11–fell 10.5% from the year-ago period, which is a substantial drop off from an already poor 6.1% year-over-year decline in the second quarter of the year, which the company is adamant is at least in part due to the 2017 third quarter earnings call fiasco. Papa John’s now expects 2018 North America comparable sales to fall 7%-10% (prior guidance was down 3% to flat) and International comparable sales to be down 2% to up 1% (prior guidance was 3%-5% growth).

A key consideration in Papa John’s investment thesis in the past had been its attractive economics at the restaurant unit level, but the extremely poor comparable sales performance has materially impacted this advantage. Margins are suffering as a result, and we expect increased marketing spending to exacerbate the impact. Management has also noted that promotional activity alone will not be sufficient in rectifying its public image, meaning that discounting on top of potentially higher marketing spending should be watched for as it relates to margin performance. Domestic company-owned restaurants operating margin contracted 1.4% in the second quarter from the year-ago period as a result of lower comparable sales and commodity and wage inflation.

Adjusted diluted earnings per share in the second quarter of 2018 at Papa John’s fell to $0.49 from $0.65 in the comparable period of 2017, and management took the opportunity to slash its full year guidance for the measure to a range of $1.30-$1.80 from $2.40-$2.80. Clearly the company is facing material headwinds as it relates to its bottom line, and industry-wide margin pressures such as rising commodity and labor costs are not helping. Additional discounting and increased marketing spending are also likely playing a role in its dismal outlook, and while some casual restaurant operators have been benefiting from a high-level of private equity interest in the space, board room drama is likely more than enough to keep such a factor at bay for the time being.

Image source: Papa John’s second quarter report

All things considered, we initially underestimated the financial impact Schnatter’s situation has had and will have on Papa John’s, and additional color from management led us to cut our fair value estimate for shares to $45 a piece. The company’s materially weakened near-term outlook has also resulted in its Dividend Cushion ratio being cut to 0.8, just below parity.

Though Valuentum prefers to avoid commentary on issues relating to public relations situations, the added risk from such a development can almost never be viewed in any sort of positive light, even if share prices can be unfairly beaten down at times. This, however, does not appear to be the case with Papa John’s as management’s expectations outline a tangible impact of the drama surrounding the company.

Related: DPZ, FRSH, YUM

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Kris Rosemann does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.