Cracker Barrel is holding its share-price uptrend nicely. The company is one of our favorite restaurants thanks in part to its differentiated niche and country store concept. Special dividend payouts make it a hidden income gem, in our view.

By Brian Nelson, CFA

Here’s what we wrote last May, “Cracker Barrel Hits the Trifecta!:”

Cracker Barrel’s (CBRL) store-within-a-restaurant concept is one of the best revenue-generators per square foot around, and it is run by a management team that knows the importance of the dividend to income investors. We continue to believe it is a great fit for the Dividend Growth Newsletter portfolio and an often overlooked one in light of its preponderance of special dividends that often fly under the radar. The Cracker Barrel ‘story’ continues to be one of pricing expansion and margin strength, as the company’s average check increased 1.7% in the fiscal third quarter, helping to drive its operating margin to 10.2% of revenue from 9.6% in the prior-year period. We can’t wait to see the leverage inherent to Cracker Barrel’s business model when total revenue trends turn upward.

Part of our thesis with Cracker Barrel had been a return to meaningful traffic expansion, but that hasn’t happened as broader traffic pressures continue to impact the entire restaurant space as new concepts continue to pop up with seemingly every imaginable theme. Cracker Barrel has staying power, however, and its ability to achieve pricing growth to drive operating income expansion in the face of overall top-line pressure is admirable (food commodity deflation has been helping). During the fourth quarter of fiscal 2017 (ended July 2017), results released September 13, the company’s operating margin expanded 80 basis points on a year-over-year basis, helping to propel earnings per diluted share to $2.23 from $2.12 in prior-year period.

Though comparable store traffic and net restaurant sales faced declines during the fourth quarter of fiscal 2017, both measures “outperformed the Casual Dining Industry,” and the company’s fiscal 2018 outlook spoke of “projected increases in comparable store restaurant sales in the range of 2.5%-3.5%, and comparable store retail sales in the range of 0%-1%.” Management noted that inflationary headwinds could put a damper on margin expansion, however, with the team projecting “operating income margin to be relatively flat to the prior year as a percent of total revenue,” but we think upside potential exists on the back of further menu price increases, which advanced 1.4% on average during the fiscal fourth quarter.

Image Source: Cracker Barrel

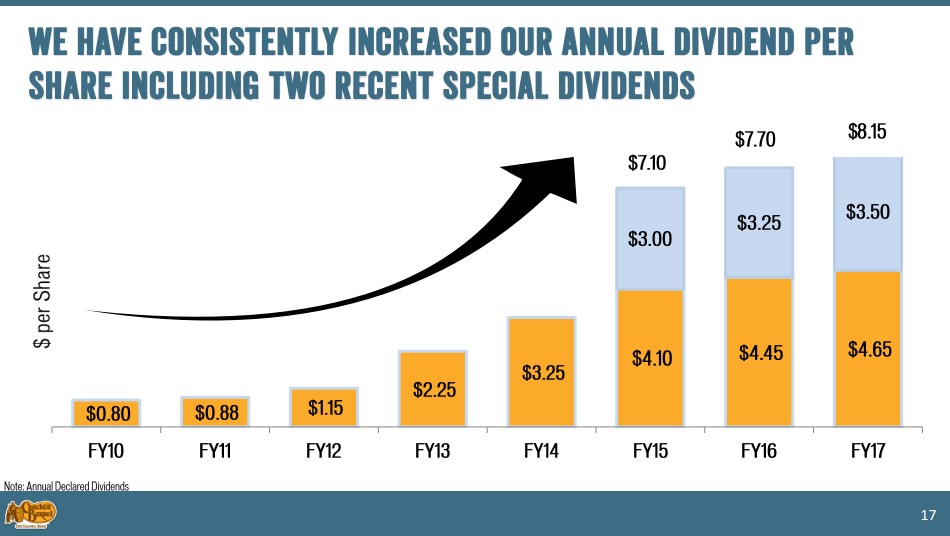

All in, we continue to believe Cracker Barrel is a good fit for the Dividend Growth Newsletter portfolio, in part because special dividends are doing a good job hiding its income potential, thereby translating into an above-average dividend yield (in most years). Including the $3.50 per share special dividend, total dividends declared in fiscal 2017 amounted to $8.15 per share (it also issued special dividends of $3 and $3.25 per share in fiscal 2015 and fiscal 2016, respectively; see page 17 here). On the basis of 2017 numbers, that’s nearly a 5.4% dividend yield given Cracker Barrel’s share price at the time of publishing. We’ll be watching for any impacts from Hurricane Harvey and Hurricane Irma, though we believe any dislocations will be transitory.

We still like this hidden income idea a lot.

Related ETF: BITE