Image Shown: Shire’s equity has been under enormous pressure as of late.

The share price of Shire Plc remains under pressure after posting decent quarterly results in early August. On the surface, the results themselves do not merit the equity hitting a new low, in our view. However, the market continues to grapple with the future direction of the company. Let’s examine the various components of Shire’s underlying business in this article.

By Alexander J. Poulos

Overview

Shire PLC (SHPG) is a Dublin, Ireland based pharmaceutical company with an interesting past. Abbvie (ABBV) attempted to acquire Shire in order to enact a tax inversion which it subsequently abandoned. The failed merger emboldened Shire to become aggressive in the M&A front with the successful takeout of Baxter’s (BAX) spin-out Baxalta. The combined assets provided Shire with an excellent way to diversify away from its core ADHD meds into the rare disease market.

Diversified Revenue Stream

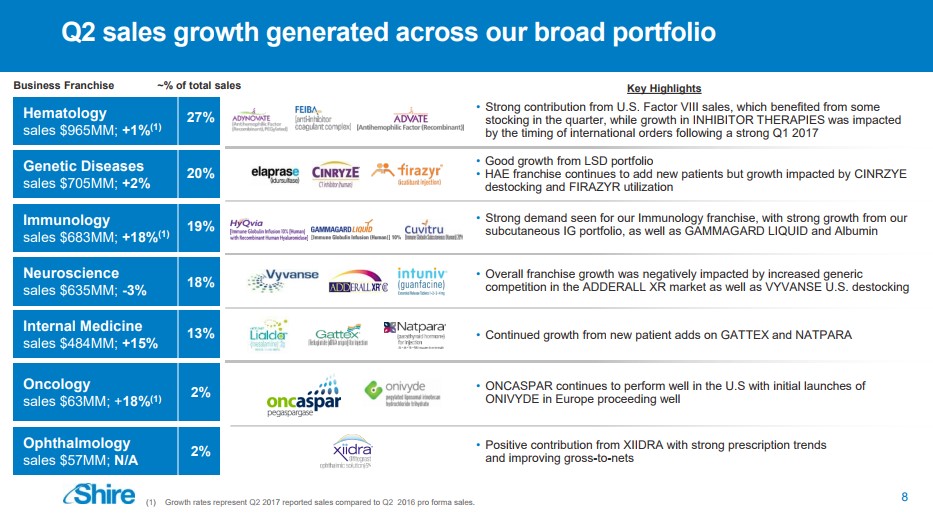

Image Source: Shire

Shire’s largest division remains the Hematology division, which was acquired via the Baxalta purchase. The division continues to face significant competition via the recent growth of Biogen’s (BIIB) recent spin-off Bioverativ’s (BIVV) Eloctate and Alprolix. We remain negative on the prospects of the Hematology division as we feel new competitors with seemingly better products are poised to enter the market. Upon entry, we would expect Shire’s division to be unable to defend its market position, which may pressure the top line further. The Hematology division will continue to serve as a source of free cash flow in the coming years. As for Shire, revenue growth will remain tepid, thus placing the equity in the traditional pharma category. The lack of a meaningful dividend lessens the appeal even further.

In addition to the challenges faced by the Hematology division, Shire’s core competency– its dominant share in the ADHD market–is nearing the end of its patent life. One of Shire’s top sellers remains Vyvanse a treatment for ADHD (attention deficit hyperactivity disorder). Vyvanse is patent protected through 2023 with the potential for a six-month extension based on additional pediatric testing, but the challenge for Shire is to expand the overall market–Vyvanse sales have advanced a rather tepid 5% thus far in 2017. The increase in sales of Vyvanse has helped cushion the loss of revenue from Adderall, Shire’s previous generation treatment for ADHD, but we feel the market for Vyvanse may remain rather stagnant–with Shire’s next generation product Mydayis likely cannibalize some of the growth available for Vyvanse.

Shire received some unfortunate news on the IP front with its lead product in the Internal Medicine category Lialda losing patent protection six months earlier than anticipated. Lialda is a small-molecule product that will face a rapid generic cliff now that it has lost patent protection. We do not expect growth of Shire’s additional products will be able to offset the loss of Lialda, thus further pressuring the top line, in our view.

A Transformational Event is Possible

We were very intrigued with the idea floated by the Shire’s management to potentially spin off the Neuroscience division, which houses the cash-cow Vyvanse, to shareholders, in which we might expect to be in the form of a tax-free spin-out. The following quote comes from the CEO of Shire taken from the recent earnings call webcast:

Flemming Ornskov, Shire plc – CEO, MD & Executive Director

As you just heard, the future remains bright for our Neuroscience business. But with that said, the successful completion of the acquisition of Baxalta has now, more than ever, established Shire as a leading biotech company focused on rare diseases. As part of our ongoing work to optimize Shire’s portfolio and Shire’s strategic focus, we have decided that now is the right time to formally assess potential strategic options for the neuroscience business. We are now in a position of much greater long-term financial and strategic flexibility, which could allow us to think about new options for the future.

In the course of the next several months, we will consider strategic options that could drive even greater shareholder value from this successful franchise, which could include the independent public listing of our Neuroscience franchise. And as I mentioned earlier, while we are currently looking to bring aboard a new Head of R&D for Shire, we would, of course, adjust accordingly our R&D leadership requirements following this strategic assessment.

While we do not have all of the answers today, I look forward to providing an update on this strategic review by year-end.

We are very interested in the potential of a reorganization of Shire. Recent examples of such moves are the split-up of Baxter, which led to Baxalta, which ironically Shire acquired. The most recent instance in the biotech sector was the decision by Biogen to cleave off Bioverativ. We believe the parallels with Biogen are the more-appropriate comparison as the parent company struggled to grow the top line. The board made a very shareholder-friendly decision to carve the company into two, a move that could act as a catalyst for growth. We feel Shire continues to view itself as a growth entity—dare we say a biotechesque franchise.

Ophthalmology

We remain impressed with the current growth trajectory of Xiidra, Shire’s recent entry into the lucrative dry-eye market. Industry-leader Restasis continues to dominate the market with a near-100% market share the past few years. Xiidra has captured a significant portion of the overall market thanks to some aggressive marketing on the part of Shire. We remain bullish on the prospects of Xiidra, but we wonder if the proposed split off the company were to come to fruition, Xiidra would lack a logical home. The product would not be a logical fit for the Neuroscience division as the disease states offer little in the way of potential sales rep overlap. The same can be said with the remaining Rare Drug stump, thus leading to our commentary of an excellent product lacking a natural home.

Concluding Thoughts

We just can’t get excited over the current composition of Shire. We feel the company would be well-served if a division of the main assets were to take place. We are pleased to see management openly express the possibility, and we will closely monitor the story as it develops, posting a timely update if warranted.

—————

Update: Executive Departures

Shire recently announced the departure of the CFO who is curiously leaving to join a start-up venture. Jeff Shelton, the current CFO, will remain with Shire through year-end while the search for a successor is undertaken. We cannot help but get the feeling a potential split of the company is now off the table based on the following comment from the press release:

Jeff Poulton, Chief Financial Officer, said: “It has been a privilege to work for Shire and to have played a part in the exceptional growth story of such an inspirational company. It has been a difficult decision, but in departing Shire, I wanted to join a smaller organization where I can play a role in building a new company. As Shire finalizes the integration of Baxalta and focusses on paying down debt, this also presents a perfect time for me to begin this transition. I know I leave Shire well positioned to pursue its strategy and deliver value for shareholders, supported by a strong Finance team.”

The market did not take kindly to the news as Shire marked a new low for the year. If a division of Shire is not a viable option—in our opinion there are superior choices in the pharma/biotech arena.

The update was added to the article August 22, 2017. Independent Healthcare and Biotech contributor Alexander J. Poulos is long Bioverativ.