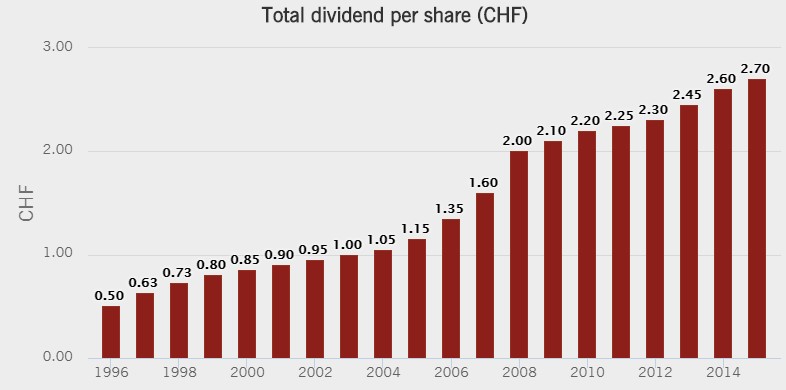

Image Shown: Novartis’ dividend history, source: Novartis.

By Alexander J. Poulos and Brian Nelson, CFA

Sometimes the most attractive opportunities manifest themselves in companies that are in the midst of a transition. In the case of entities in the pharmaceutical industry, the transition often occurs during the period of patent-protection loss of a top-selling treatment. Typically, the market will sour on the company’s prospects as revenue is expected to decline in the near term. However, the longer investment time horizon we have at Valuentum allows us to examine whether such opportunities still fit for inclusion in the newsletter portfolios. Said differently, we’re less interested in what the company will do in the next quarter or two than we are in the company’s competitive advantages and its discounted cash-flow derived intrinsic worth. If the long-term is still bright, we can overlook temporary near-term challenges.

Overview

Novartis (NVS) is a well-diversified pharmaceutical powerhouse based in Switzerland. The company is far from a household name in the US, but to draw a fair comparison based on market capitalization, a close competitor is Pfizer (PFE) at nearly $200 billion (we’re talking about mega-cap). The comparison with Pfizer gains increasing relevance, too, as Novartis like Pfizer does not exclusively rely on patent-protected pharmaceuticals to derive the bulk of its revenue stream. The diversity of Novartis’ revenue stream allows for a generous return of capital to shareholders in the form of an increasing annual dividend, a noted difference from the quarterly payout of Pfizer, which was cut when the latter bought Wyeth a number of years ago. The analysis below details the three most important divisions of Novartis beginning with its Pharmaceuticals division.

Pharmaceuticals

The Pharmaceutical segment remains the most dynamic area of Novartis. The company remains on pace to bring forth three novel products that together we estimate will more than offset the revenue loss from key products. Novartis recently lost patent protection of its top-selling product Gleevec after a long and fruitful run. The move was not unexpected; the groundwork has been put in place to offset the loss, but Novartis is now firmly in the penalty box as revenue is expected to drop when the company reports 2016 numbers.

To streamline its product portfolio and to concentrate on areas of noted strength, Novartis had entered into a deal with fellow European pharma heavyweight GlaxoSmithKline (GSK) in 2014 to purchase Glaxo’s Oncology division while combining their respective consumer health groups. Novartis exited the vaccine market by divesting the bulk of its line to Glaxo as well. Novartis gained a host of novel oncology properties expanding its formidable presence in oncology. Thus far, oncology therapies have remained resistant to hardball negotiating tactics by the PBM’s, and while there are no guarantees that payers will not balk over price, oncology remains the premier area of focus for the pharma/biotech sector. Novartis internal R&D efforts have begun to bear fruit with three important compounds on pace to exceed the revenue lost from the expiration of Gleevec’s patent ($4.74 billion in sales for 2015).

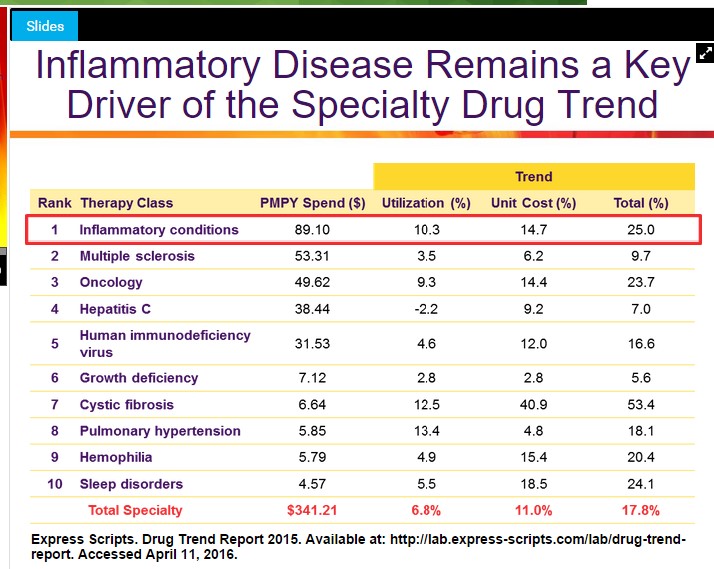

The first compound worthy of discussion is Cosentyx, Novartis entrance into the crowded field of inflammatory diseases. Cosentyx is an interleukin 17-a antagonist, for the treatment of a host of inflammatory diseases, most notably psoriasis. The treatment requires subcutaneous injections similar to other treatments such as Humira and Enbrel. Treatment of inflammatory disease with a biological agent such as Cosentyx comprises the largest treatment cohort of specialty pharma. The rapid growth of specialty pharma is approaching par with traditional oral dosage forms. In the current environment where PBM’s are looking to get a handle on the rising cost of therapies, the biological treatments for inflammatory disease offer a particularly enticing target for hardball negotiating tactics.

Image Source: Express Scripts

Evidence of the PBM’s taking a harder stance has recently been exposed from Amgen (AMGN) where the company doesn’t expect to be able to raise prices on Enbrel in 2017 (as disclosed in the most recent conference call). We raise the specter of increasing cost scrutiny to offer a more balanced view of the opportunity in Cosentyx, even as we say that Cosentyx remains well on pace to post sales in 2016 in excess of $1 billion dollars, cementing the treatment as a blockbuster product.

In clinical trials, Cosentyx registered superior outcomes compared to Enbrel and Johnson and Johnson’s (JNJ) Stelara. The head to head data is key; this allows the product to differentiate itself in the eyes of the payers. The PBM’s will look to cover the most effective product, and with Cosentyx posting superior outcomes, the product might be able to take meaningful share from Stelara. To add additional context as to the upside of the product, Stelara posted sales of $2.3 billion in the first three quarters of 2016.

Novartis is conducting an outcomes trial comparing Cosentyx to top selling product Humira. A positive head-to-head result will further support Cosentyx as the optimal choice in the treatment of psoriasis. If Cosentyx is able to post superior results in this trial, a credible case could be made that Cosentyx by itself will replace the revenue lost from Gleevec. We’ll continue to monitor developments.

Entresto

Entresto is a novel new treatment for heart failure. The compound is a combination of Sacubitril a Neprilysin Inhibitor and Novartis’ recent blockbuster Diovan (Valsartan). Thus far, the utilization of the product is not up to the initial hopes of management as the payers required a prior authorization before paying for the product.

The lack of favorable formulary placement is a major impediment to sales growth in 2016, with net sales of $200 million in the US expected for 2016. Management remains confident it will be able to rectify the formulary issue with an aggressive push to negate the need for a prior authorization. Aiding in this endeavor is recent data that indicates the product is efficacious.

Though we remain in a “show me state,” the data is indeed compelling. We continue to monitor the weekly IMS Rx data to determine if Entresto remains on the right path, but thus far, the number of prescriptions filled continues to point north. We’re encouraged.

As a novel new agent with a large addressable market, Entresto is a particularly noteworthy compound. The key for Novartis, however, will be to unlock the PBM’s initial resistance towards covering the product. Due to the lack of meaningful competition, Entresto has the potential to become one of Novartis top-selling products.

Ribociclib

Novartis’ Oncology division is a source of future innovation with a promising new therapy for breast cancer. Ribociclib is a new treatment that was recently granted breakthrough therapy designation by the FDA. Ribociclib is designed to be used in conjunction with letrozole to treat women with postmenopausal HR+/HER2- advanced or metastatic breast cancer. The combo would be a first line treatment, a key designation as it should allow for maximum uptake.

Thus far in individual trials, Ribociclib has shown to be slightly more efficacious than category leader Pfizer (PFE) Ibrance. Novartis is conducting a head to head study; a positive outcome would allow Ribociclib to vault past Ibrance, becoming the top-selling product in its class. Thus far, the oncology properties have proven to be remarkably resistant to pricing pressure from the individual payers–a win here would set up a lucrative annuity-like revenue stream for Novartis.

In November, the FDA issued a priority review for Ribociclib, which will shorten by ten months the decision process. A PDUFA date for Ribociclib has not been assigned at the time or is in writing; we expect a decision within six months of the FDA acceptance of the application, which is dated November 1, 2016, at some point before the end of the second quarter

Siponimod

In a strategic bit of lifecycle management, Novartis’ Multiple Sclerosis franchise faces the loss of patent exclusivity of its top-selling product Gilenya. The patent is expected to expire in 2019. Gilenya accounted for $2.7 billion in sales in 2015 and continued to ramp higher.

Novartis, however, scored an impressive clinical win with stunning results for Siponimod for the treatment of secondary progression multiple sclerosis. The key for Novartis is the category remains an area of significant unmet need, which should allow the company to ramp sales at an aggressive rate. Siponimod is competing in a wide open field versus Gilenya which needs to contend with multiple existing products such as Teva’s (TEVA) Copaxone and Biogen’s (BIIB) Tecfidera. Novartis has a clear path to establishing Siponimod as the primary standard of care for the indication of secondary progressive multiple sclerosis which should go a long way towards recouping the expected loss of Gilenya revenue in 2019. Assuming, Siponimod continues its impressive streak of results, a credible case could be made that the product might eclipse the sales of Gilenya.

Novartis continues its research-based focus with numerous compounds in various stages of the investigation. The list above highlights some of the most promising near-term candidates. The field remains uncertain with many surprises both positive and negative that can manifest themselves at any time. One example in particular was Siponimod, which was not even identified as one of Novartis top molecules–it came out of the blue in a positive manner. The second division worth examination is the Sandoz division that manufactures generic equivalents and biosimilars, an area of particular focus.

Sandoz

The Sandoz Division manufactures pharmaceutical products that have lost patent exclusivity. The field is notoriously competitive with little in the way to distinguish operations from competitors. Sandoz, however, does offer Novartis an attractive opportunity to manage the patent loss of some of its principal products. If Sandoz is the first to file for an authorized generic of a product, the division will be granted a six-month exclusive window to manufacture the only authorized generic of the product.

Once the six-month exclusivity lapses, however, the margins plummet as additional competitors enter the market. Once the six-month exclusive window lapses, the product will behave in a similar manner as a commodity, rising and falling based on the number of competitors in the market. Typically, however, the price will collapse and stay depressed. For Novartis, we like that the company can maintain the bulk of the branded sales (just a bit longer) by transferring the branded product to their Sandoz division, making the exercise worthwhile.

The Sandoz division accounted for ~20% of Novartis’ overall sales in 2015, but accounted for only ~10% of operating income due to the lower margins that come with making generic medications. The key driver going forward is Sandoz’s burgeoning biosimilar division, which is on pace to produce equivalents of many of the top-selling biologic agents. Thus far, Sandoz has authorized biosimilars of Copaxone 20mg and Neupogen, in addition to unanimous approval for a bioequivalent of Enbrel. Sandoz did suffer a notable setback in the quest for a biosimilar for Neulasta by receiving a complete response from the FDA. Sandoz will need to address the deficiencies noted and refile, delaying the process.

The Sandoz Division offers Novartis a clear path to profit from the burgeoning field of biosimilar equivalents of top-selling products. The biotech field is rapidly evolving, and the rise of biosimilars has shaken the industry; it is no longer feasible to rest on the laurels of decades-old innovations. These compounds will now face the same price competition as solid dosage forms. The older more established companies who have not meaningfully diversified their product line are at particular risk as multiple companies are vying for a piece of their once formidable sales.

The payers of the world, most notably governments, are keen to keep price competition heated in an attempt to corral price, as the demographic tidal wave descends on each countries’ healthcare budget. Great rewards await the companies that can bring forth novel new treatments to address the various ills plaguing humankind.

Alcon

The final division worth noting is the troubled Alcon eye care division. Novartis acquired Alcon in a series of purchases with the final price tag eclipsing $50 billion dollars. Thus far, the move has been a disappointment with hoped-for deal synergies failing to materialize. Alcon’s key product Lucentis continues to lose market share as Regeneron’s (REGN) Eyelea continues to take share. Further complicating matters is the weak sales in its surgical division with plans in place to turn around the division.

The market remains rife with rumors that Novartis may seek to divest Alcon to pursue other fast-growing fields. We do not share the view, as Novartis’ debt load leaves it sufficient firepower to make tuck-in acquisitions, as needed. Thus far, the management team has indicated an appetite for smaller complementary deals instead of larger more expensive deals. We continue to share the cautious stance of management, as market caps remain elevated in the mid-to-late stage biotech companies.

To Novartis credit, it made a couple of tuck-in acquisitions at the end of 2016, acquiring Encore Vision to bolster the offerings of the Alcon division. Also, right at the end of the year, Novartis paid $50 million to gain an option on Conatus Pharmaceuticals NASH candidate. It remains to be seen if either product will bear fruit, but we like the low-cost approach in these efforts. Novartis is gaining access to some innovative products at a modest cost.

Dividend*

As a diversified company in a number aspects of the drug delivery universe, Novartis generates a substantial amount of free cash flow. During the past three years, for example, cash flow from operations has hovered between $12-$14 billion, while capital spending has been between $2-$3 billion, good for about $10 billion in run-rate free cash flow generation capacity (it allocated $6.6 billion to the dividend in 2015).

The primary method employed to return cash to shareholders remains the annual dividend. As is typical of European equities, the dividend is distributed once a year, unlike the quarterly payouts that dominate the US market. We rate Novartis’ Economic Castle as attractive, and we do not believe the company will have any difficulty raising the dividend in coming years. At this time we are not prepared to add Novartis to the Dividend Growth Newsletter portfolio, but Novartis does have a collection of exciting branded products. We wanted to get this one in front of you in case we decide to pull the trigger on the idea.

* The price of Novartis’ ADRs and the US dollar value of any dividends may be negatively affected by fluctuations in the US dollar/Swiss franc exchange rate.

Disclosures: Alexander J. Poulos is long Novartis.