![]()

Image Source: BY-YOUR-⌘

By Kris Rosemann

We hope you are having a great start to the week! We wanted to bring your attention to one of the holdings that we include in the portfolios of the Best Ideas Newsletter and Dividend Growth Newsletter, Cisco (CSCO). The newsletter portfolios are one of the best ways to measure Valuentum’s asset allocation and stock-selection performance, and they are released on the 1st of the month (Dividend Growth Newsletter) and the 15th of the month (Best Ideas Newsletter), respectively. If you ever want to view the archives, they are located in the left column of the website, “View Current and Archived Newsletters.”

Both of the newsletter portfolios surface ideas that we think fit well within a portfolio context while considering Valuentum’s methodology for capital appreciation, the Valuentum Buying Index, in the Best Ideas Newsletter, and Valuentum’s methodology for dividend growth, the Dividend Cushion ratio, in the Dividend Growth Newsletter portfolio, among other criteria. Cisco, for example, was added to both newsletter portfolios a few years ago. Sometimes members are concerned that they’ve “missed out” on opportunities when they see that a holding was added some time ago. The newsletter portfolios continue to set new highs.

Another way to assess our analytical performance is via the ideas in the Nelson Exclusive, our fastest-growing monthly publication. We believe this publication is one of the best ways for our team to showcase the depth of our analytical work. We really get to the bottom of things in this publication — what’s the CEO’s salary; is the executive team properly incentivized? What’s really going on? We spare no details. Several of the ideas highlighted in the Exclusive are already performing well out of the gates, and the publication is brand new! For members that may be most concerned about a “buy and monitor closely” portfolio strategy as those of the portfolios of the Best Ideas Newsletter and Dividend Growth Newsletter, the Exclusive is a fine option.

Our analytical product, the 16-page reports and 2-page supplemental dividend reports, is not light on the financial details either. We understand that financial analysis is not “fun.” We know that the numbers can be intimidating. But we want you to have an informed estimate of what the company you are investing in is actually worth. That requires some number crunching; sometimes a lot. The value of any company will always rest in the net cash on its balance sheet and the present value of its future enterprise free cash flows that accrue to investors. Name anything – for it to have value, it must eventually convert to free cash flow. The price-to-fair-value “question,” or comparing the price of a company to its free-cash-flow based fair value estimate, will always be one of the most important stock investment considerations. The market is a “weighing machine” over the long haul, and “cash” will always be king.

This is a big one: Investing is all about forward-looking information. What a company has done in the past is…well…history. It’s over with. Many investors are often provided historical information (due to compliance reasons or others) so they may come to believe that historical information is what money managers are using in their decision-making process. Perhaps – but not the best ones. (This may be the best article ever written on the topic.) As a result, many investors have somehow grown skeptical of considering forward-looking information. Why? Well, historical information is easily available, and they have grown comfortable with it because it is precise. But such information will never be the driver behind future stock prices. But how do we address the unpredictable nature of future free cash flows in our valuation framework? We employ a margin of safety, as in the fair value ranges, which embrace a cone of outcomes surrounding our future free-cash-flow derived point fair value estimates.

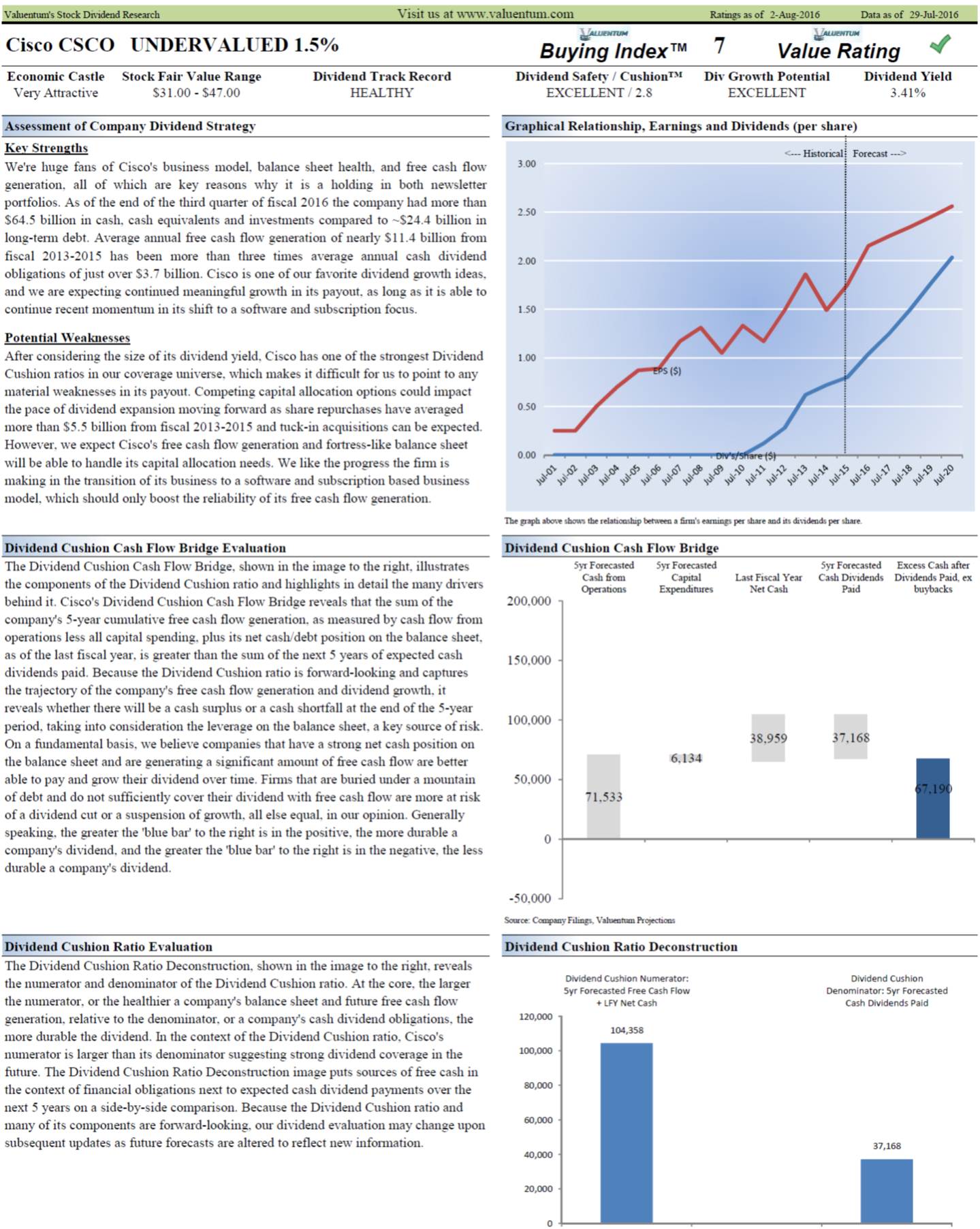

But to the point about the future. While many of your income investor friends are looking at the past for ideas, you also have access to one of the most comprehensive forward-looking, cash-flow based dividend coverage metrics, the Dividend Cushion ratio. This ratio has essentially predicted the dividend cuts in our coverage with a high degree of accuracy, putting investors ahead of the high-profile cuts at BHP (BHP), ConocoPhillips (COP), Potash (POT), Kinder Morgan (KMI), and the list goes on and on. At the end of this article, we’ll include the composition of the Dividend Cushion ratio for Cisco, which explains why we like the company’s long-term dividend growth prospects so much. Without further delay, let’s dig into Cisco’s most recent results.

The communication networking giant announced fiscal fourth quarter results August 17. Excluding the impact of its divested SP Video and CPE business, Cisco reported revenue growth of 2% in the quarter on a year-over-year basis. Ongoing momentum in its business model transformation was on full display in the quarter as well, as deferred revenue from software and subscriptions leapt 33% from the year-ago period. We like what Cisco’s business transformation will do for it in terms of recurring revenue (more visible and reliable revenue streams).

Such a transformation will be coupled with the firm’s announcement of a restructuring initiative that is intended to optimize its cost base in lower growth areas and reinvest the cost savings into key growth areas, such as security, Internet of Things (IoT), collaboration, next generation data, and cloud. The restructuring plan will result in the release of up to 5,500 employees, or approximately 7% of the company’s workforce. Pretax charges of up to $700 million are expected on a GAAP basis, and $325-$400 million of such charges are expected to be recorded in the first quarter of fiscal 2016, with the balance of the charges recognized throughout the remainder of the fiscal year.

While we like what the restructuring actions should ultimately do for Cisco in terms of cost savings and reinvestments for future growth, its bottom-line performance has already been solid as of late. GAAP diluted earnings per share jumped 24% in the fiscal fourth quarter on a year-over-year basis and advanced 21% for the full fiscal year from fiscal 2015. Free cash flow generation for the company remained nothing short of impressive in fiscal 2016, as it leapt nearly 10% from fiscal 2015 to an impressive ~$12.4 billion.

Such strong free cash flow generation is the basis for Cisco’s impressive balance sheet health, one of the key considerations that keeps the company in both of our newsletter portfolios. As of the end of fiscal 2016, the firm had a net cash position of more than $37.1 billion, an extremely attractive quality for a firm that will have to be extremely flexible in responding to consumer demand and work to be more innovative than ever before, not to mention what the cash position does for its dividend strength.

We think Cisco’s management has a great handle on its business. The restructuring plan is a welcome shift of attention in terms of growth priorities for the firm, and we like the potential it brings in cost savings in the near-term horizon, as well as what it means for driving top-line growth over the long run. Our investment thesis for Cisco remains the same. As we stated after the firm’s third quarter report “Flash: Cisco Pops…”

Cisco’s business model transition, gross margin resiliency, fantastic free cash flow generation, fortress balance sheet, and attractive dividend yield make it a no-brainer position in the portfolios of both the Best Ideas Newsletter and Dividend Growth Newsletter, in our view.

We continue to believe price-to-fair value convergence in Cisco’s shares is in the cards (our fair value estimate sits at $39), and we have no qualms with taking a patient approach as we collect one of the strongest dividends on the market, in our opinion. Shares currently yield ~3.4% with a Dividend Cushion ratio of 2.8. As promised, here’s how we derive its Dividend Cushion ratio, taken directly from page 2 of Cisco’s dividend report, found on its landing page here.