Image Source: Mike Mozart

By Jessica Bishop

Sprint (S) is not in good financial shape, and we view the company’s equity as a mere lotto ticket that likely won’t pay off. It’s probable that shares of Sprint may continue to converge toward $0 as the economic cycle matures. After all, these are good times, and the company is a mere penny stock. Investors have to be thinking: What’s going to happen when economic activity truly heads south? Our fair value estimate remains unchanged at $4 per share as of the latest update, however, and our relatively large fair value range reflects the tremendous risks of this overleveraged, capital-intensive business model that has only just begun to turn the corner with respect to operating profits this late in the economic cycle.

Sprint has been doing all that it can to keep its head above water; it has improved its free cash flow burn (use) to -$1.4 billion (negative $1.4 billion) in fiscal 2015 from -$3.3 billion (negative $3.3 billion) in fiscal 2014 and -$5.3 billion in fiscal 2013 (negative $5.3 billion), and management expects to be adjusted free-cash-flow neutral in fiscal 2016. Though we would like free cash flow to be significantly positive, as is the case with rivals AT&T (T) and Verizon (VZ), we are happy to see an improvement, and frankly, Sprint will need this incremental cash to keep creditors at bay. Of note, however, most of the free-cash-flow generation improvement is still of the lower-quality variety via ongoing reduction in operating expenses and reduced capital spending. Operating income may hit $1.5 billion in fiscal 2016 from $300 million in fiscal 2015 as a result of these unsustainable endeavors (it can’t cut costs and reduce spending forever).

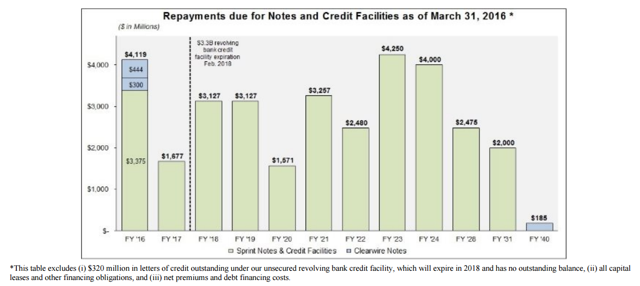

Image Source: Sprint 10-K

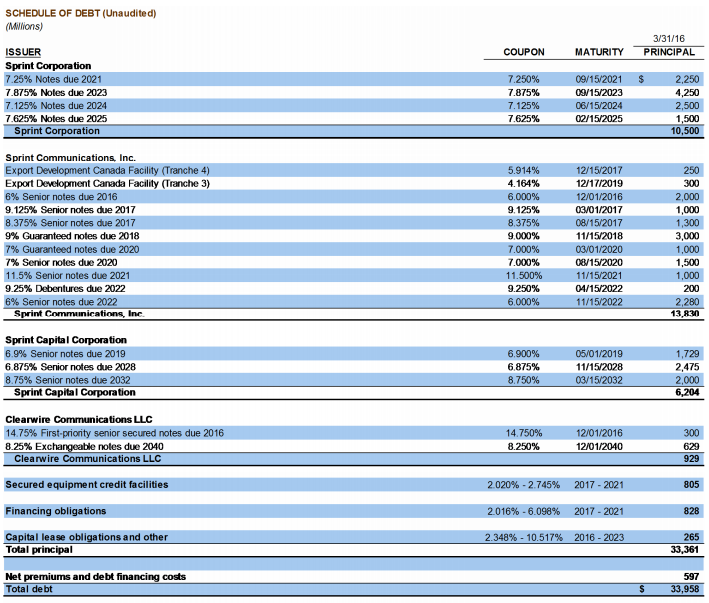

Those that know Sprint know of this risk very well, and that risk is that Sprint has considerable financial leverage on the books; it has net debt in excess of $30 billion, with more than $3 billion in debt maturing in fiscal 2016 (its maturities, as shown above, are meaningful and consecutive over the next several years). Refinancing risk won’t let up anytime soon through fiscal 2024 (not a typo), and it may heighten at the worst possible time if a global economic recession hits in the next few years. Yikes! However, to help in keeping its credit afloat (Moody’s has a corporate credit rating of Caa1 on the company), it currently has ~$5.7 billion of general purpose liquidity including ~$2.6 billion in cash (the balance is mostly its revolver). Interestingly, sophisticated financing maneuvers, namely RAN LeaseCo, a second transaction with MLS, and signed bridge financing, will allow Sprint to “repay” fiscal 2016 maturities. What it will do after 2017, however, remains a huge concern for long-term investors.

Sprint operates in a very competitive field (the backdrop likely best described as brutal), with its two largest rivals being AT&T and Verizon, which are also struggling to hold onto customers (both had postpaid net losses in the Jan-Mar 2016 period). To keep from losing customers, Sprint is offering and may have to continue to offer significantly lower prices than that of its rivals, or pursue sophisticated marketing techniques. Such strategic moves to pursue customer retention will continue to pressure operating income, in our view, and there are no guarantees these moves will pay off, of course. Though there have been positive internal metric developments as of late, including the highest post-paid additions in three years during 2015 and the “best-ever postpaid churn” for the year in its 20-year history in the wireless business, we can’t help but note that this is happening when the economy is extremely healthy.

Sprint has had to cut back capital spending and reduce marketing expenses (SG&A has fallen to $8.5 billion in fiscal 2015 from $9.6 billion in fiscal 2014), but the company is not going quietly into the night. To improve its competitive position, Sprint has taken advantage of the attention of the soccer tourney Copa America Centenario, by being the first U.S. carrier to demo 5G wireless at a major public event. Services like its LTE Plus service (in 204 markets) has helped its performance for voice and data. Its focus on innovation, by actively researching and demonstrating its 5G capabilities and partnering with Nokia (NOK), while reducing operating expense (management plans on reducing by ~$2 billion in fiscal 2016) will help lead to an improvement of adjusted EBITDA of up to $10 billion in fiscal 2016 from $8.1 billion in fiscal 2015.

Though the company is saddled with a tremendous amount of debt, if it hits its adjusted EBITDA target, net debt-to-adjusted EBITDA will have fallen considerably, to ~3x, and may fall more if the company makes good on its promise to pay all debt maturing in 2016. Is it time for Moody’s to raise the corporate credit rating? Just because leverage may improve doesn’t mean that the company will survive, however, which may be why the credit rating agency is slow to move. Softbank, which owns more than 80% of the company, is the ace up Sprint’s sleeve, but minority shareholders could still be left in the cold. We still believe the best long-term outcome for Sprint shareholders is a buyout by a rival. We’ll be monitoring the M&A landscape closely.

Image Source: Sprint 10-K