Image Source: Tesla

By Brian Nelson, CFA

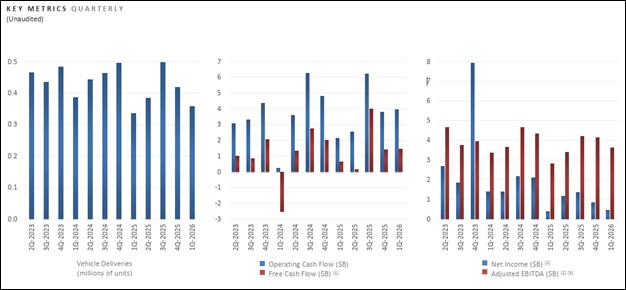

On April 22, Tesla (TSLA) reported better than expected first quarter results with revenue and non-GAAP earnings per share coming in better than the consensus estimates. Automotive and total revenues advanced 16% from the year-ago period, while gross profit rose 50%, as gross margins expanded nearly 480 basis points. Though down sequentially, income from operations more than doubled versus the same period last year, as its operating margin swelled 214 basis points. Adjusted EBITDA increased 30% on a 183 basis-point improvement in its EBITDA margin. Year-over-year, non-GAAP net income rose 56%, while non-GAAP earnings per share advanced 52%.

Management had the following to say about the results:

We continued to make meaningful progress on the build out of the infrastructure and AI software that underpins our Robotaxi and future robotics businesses in Q1. We commenced ramp of additional AI compute, new factories across battery and battery materials, and further prepared lines for start of production of Megapack 3, Cybercab and the Tesla Semi. We saw continued growth in demand for our vehicles in markets in APAC and South America, while also seeing a rebound of demand in both EMEA and North America.

We are making the necessary investments that will ensure our access to key materials and componentry in each region across vehicle, energy and AI as trade and geopolitics become more uncertain. In recent months, we have announced further regionalization and vertical integration of critical supply chains.

Our focus on affordability and utility across our vehicle lineup continues to be a key competitive advantage, particularly as gas-powered alternatives become more expensive due to their reliance on a more sensitive and less flexible energy supply chain.

We are excited about Tesla’s positioning in 2026 with tailwinds persisting for the autos business, our continued progress on FSD (Supervised), the ramp of Robotaxi, progress on Optimus ahead of mass production and the growth of our energy production capacity.

There remains significant effort and hard work to realize our mission of Amazing Abundance. As always, we are focused on maintaining a rapid pace of innovation in new and exciting technologies – such as electrification, cutting-edge software and artificial intelligence – expanding our lead in advanced manufacturing and increasing supply chain resilience to ensure we manage future risk to our scale. The future is incredibly bright.

During the quarter, Tesla generated $3.9 billion in operating cash flow and spent $2.5 billion in capital expenditures, resulting in free cash flow of $1.4 billion. It ended the quarter with $44.7 billion in cash and cash equivalents. Tesla’s first quarter results were good, and we await volume production of the Cybercab, Tesla Semi, and Megapack 3 this year and preparations for its first large-scale Optimus robot factory in the current second quarter. Tesla continues to focus on maximum capacity utilization at its factories and managing the business to ensure a strong balance sheet. Shares of Tesla gained following the report, but dipped after the conference call following capital spending guidance of $25+ billion for 2026. We like Tesla, but the company’s shares are too pricey for our taste.

—–

Brian Nelson owns shares in SPY, SCHG, QQQ, QQQM, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, QQQM, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.