Let’s set one thing straight. On a fundamental basis, biotech firm Gilead Sciences (GILD) is performing quite well, contrary to what its recent stock price move might suggest. Prescriptions for the firm’s Harvoni and Sovaldi hepatitis-C drugs continue to track slightly ahead of projections, and we would expect a slightly stronger-than-forecast fourth-quarter report as a result. In coming periods, we look forward to positive management commentary that speaks to the strength and sustainability of the firm’s hepatitis-C franchise (about half of Gilead’s sales).

Any commentary, in light of the recent uncertainty and growing competition in the hepatitis C market, will be reassuring for investors that have been anxiously pursuing tax-loss selling and profit-taking in Gilead’s shares the past few weeks. From our perspective, all is well at Gilead, and good news is forthcoming when the firm reports fourth-quarter results in early February (or late January), if the upcoming J.P. Morgan Healthcare Conference January 13 does not improve sentiment before then. We think patience is in order for new information, and the few weeks after the New Year could bring a wave of buying as fourth-quarter tax-loss sellers reinstate positions in this fundamentally-solid firm.

According to the World Health Organization, 130-150 million people globally have chronic hepatitis C infection, and a significant number of those who are chronically infected will develop liver cirrhosis or liver cancer, with as many as 350,000-500,000 people dying each year from hepatitis C-related liver diseases. According to Gilead, “the worldwide potential for all oral antiviral pan-genotypic HCV cure is sizable with over 12 million infected individuals in commercial markets alone.” Chronic hepatitis C affects roughly 3-4 million people in the US, and the majority of these are baby boomers (individuals born between 1945 and 1965). The market for HCV-related treatments is large and growing due to demographic trends, and we think many industry biotech participants will be able to garner various levels of success in the space; it is not an all-or-nothing game. The HCV therapeutic market, by our estimates, continues to be vastly underserved, despite advances in treatments, and only a small fraction of those infected with HCV are actually diagnosed, let alone treated.

The efficacy of Gilead’s Solvaldi has been well-established in patients with HCV genotypes 1, 2, 3, or 4 infections, and cure rates are as high as 90%; therapy has been reduced to 8-12 weeks from 24-48 weeks. Solvadi and its successor Harvoni are excellent examples of what we would describe as interferon-free, all-oral regimens that achieve extremely high cure rates with fewer side effects. Previous HCV treatments, for example, caused side effects that ranged from bone marrow suppression and fatigue to debilitating rash and anemia. Harvoni’s efficacy, by combining the NS5A inhibitor ledipasvir with the nucleotide analog polymerase inhibitor sofosbuvir (Solvadi), is so impressive that it can achieve cure rates in the range of 94%-99%. This efficacy will be difficult for any competing therapy to better.

Image Source: Gilead

But competition is a-coming, though it certainly shouldn’t be unexpected.

Litigation regarding Sovaldi covers a large portion of Gilead’s regulatory filings ranging from contract arbitration with Jeremy Clark—a former employee and inventor of a patent that claims metabolites of sofosbuvir and RG7128—and arbitration with Roche regarding the exclusive license to sofosbuvir to interference proceedings and litigation with Merck’s (MRK) Idenix and litigation with Merck itself that requests Gilead pay royalties on the sales of sofosbuvir. It is only that the news has been so prominent related to litigation with AbbVie (ABBV), which recently obtained patents that claim the use of a combination of LDV (ledipasvir)/SOF (sofosbuvir) for the treatment of HCV, that the most attention has been given to the recent Abbott (ABT) spin-off. The stakes are high, and participants want a piece of the lucrative HCV market. We won’t know the final decisions of these cases for some time, but the likelihood of an adverse ruling materially hurting Gilead is low, in our view. Instead, we think it is more likely that AbbVie or Merck will acquire Gilead in the future than destroy value in the HCV market through the court system.

There are a number of therapies that compete with Sovaldi and Harvoni. Johnson & Johnson (JNJ) Janssen’s Olysio (simeprevir), Merck’s Victrelis, and Vertex’s (VRTX) Incivek (telaprevir) are a few antivirals that come immediately to mind, though the latter two aren’t specifically indicated as such. AbbVie’s Viekira Pak was recently approved by the FDA. “Viekira Pak contains three new drugs—ombitasvir, Enanta’s (ENTA) paritaprevir and dasabuvir—that work together to inhibit the growth of HCV…Viekira Pak is the fourth drug product approved by the FDA in the past year to treat chronic HCV infection. The FDA approved Olysio (simeprevir) in November 2013, Sovaldi (sofosbuvir) in December 2013 and Harvoni (ledipasvir and sofosbuvir) in October 2014 (source: FDA).” Further, Achillion Pharmaceuticals (ACHN) believes its HCV regimen has “best in-disease” performance, though results so far have extended only to a Phase 2 “Proxy Study” and use sofosbuvir for treatment.

The HCV-landscape continues to evolve, and there is plenty of room for a number of players in this space, including the big 3: Johnson & Johnson, Gilead, and now AbbVie. At the moment, we believe that Gilead’s Harvoni is the most efficacious, as Viekira Pak trials showed a bigger and lower bottom-rung of cure rates (91%-100%), compared to Gilead’s Harvoni registering a much tighter range of 94%-99%. Those using the Viekira Pak reported side effects of feeling tired, itching, feeling weak or lack of energy, nausea and trouble sleeping; the most common side effects of Harvoni include tiredness and headache. The Viekira Pak is four-to-six pills per day, while Harvoni is only a single pill taken daily, so convenience also appears to edge in Gilead’s favor.

Cause for concern over a pricing war in the HCV market also appears overblown. A standard course of treatment for Sovaldi costs $84,000, while Harvoni is priced in the neighborhood of $94,500. AbbVie is expected to price the Viekira Pak regimen at ~$83,319 per patient per 12-week course – hardly signaling a price war. In fact, the Viekira Pak pricing scheme is rational and perhaps, dare we say, a best-case scenario for Gilead. We would have grown more concerned if, on the other hand, the list price for the Viekira Pak had been set drastically below than that of Solvaldi/Harvoni – say at $10,000 per regimen. It appears that AbbVie will be a rational participant in the HCV market.

By extension, we believe AbbVie had to offer a 30%-35% discount to land the deal with Express Scripts (ESRX) because its product could potentially be viewed as an inferior, four-to-six pills-a-day, less-efficacious regimen by physicians. Additionally, Express Scripts seems to be mounting pressure on all drug makers, revealing that the discount will hardly be an HCV-specific issue. From our perspective, however, price will be only one deciding factor when it comes to human health, and ultimately we believe a patient’s doctor will determine overall HCV market share, even if physicians encounter obstacles across the PBM chain. Some doctors, for example, may refuse to switch regimens. In fact, the AbbVie/Express Scripts deal seems to fly in the face of increasing patient treatment options (one of the goals of modern medicine), and we would not be surprised if Express Scripts eventually backs off a bit with its exclusivity clause.

In any case, given that a large portion of the HCV market is the baby-boom generation (which may already take a number of pills daily), even with Express Scripts, the Viekira Pak may not move the market-share needle too much, or not as much as market observers believe. The Viekira Pak may generate $2-$3 billion in sales during 2015, or about what Solvaldi did during the most recent third quarter alone, which was depressed due to impending Harvoni sales. From our point of view, Johnson & Johnson, AbbVie, and Gilead are “still playing nicely in the sandbox,” and it appears a rational oligopoly is present. Neither firm has any incentive to destroy the HCV-market value pie, especially as litigation ensues.

Wrapping Things Up

Gilead Sciences continues to trade like a stock that is experiencing tax-loss selling and profit taking, not one that is fundamentally (or technically) in much trouble. We think the HCV market is a rational oligopoly, and eventually, we would expect Express Scripts to lighten up exclusivity on account of improving patient treatment options. From our perspective, physicians will ultimately decide which HCV treatment is most appropriate for patients, and on the basis of efficacy and convenience, Gilead’s Harvoni still appears to be a very, very good option, if not the best.

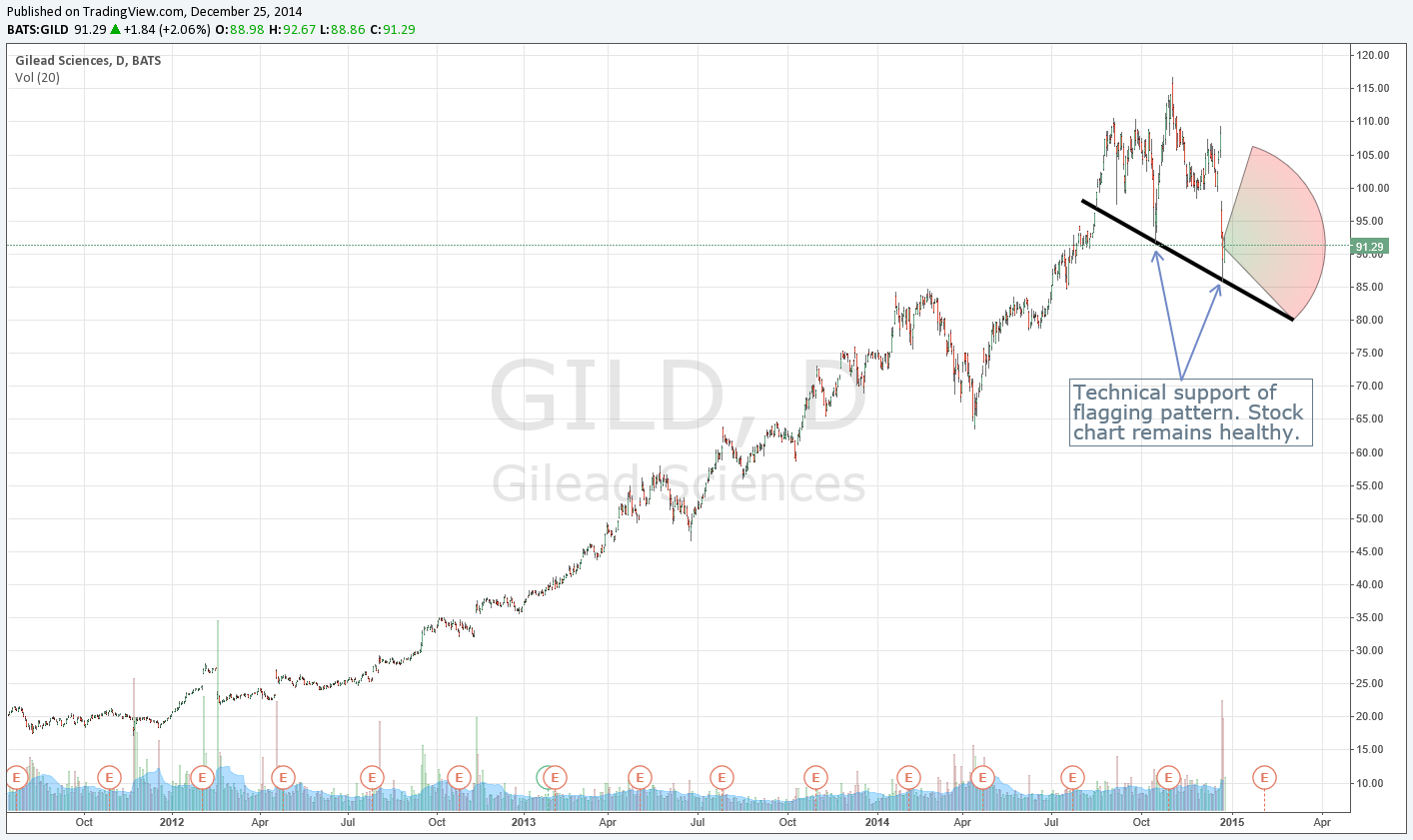

We think news flow over the next several weeks will improve at Gilead as a result of positive management commentary at an upcoming conference and as we near the firm’s fourth-quarter results, which we expect to be strong. Our fair value estimate for Gilead remains unchanged at ~$150 per share, and our technical evaluation of the firm indicates that support is healthy. Consensus estimates reveal a stock that is trading at just 10 times 2015 earnings, and even under a bear-case scenario where expected earnings are slashed by 35% next year, Gilead’s shares are still trading at a very digestible 14 times 2015 earnings.

Market participants are being way too punitive with Gilead’s shares, and the weighting of the firm in the Best Ideas portfolio remains unchanged in light of recent events. We outline a multi-month chart of Gilead to provide increased perspective of the company’s fantastic price run. Shares could fall to as low as $70 each before we would become concerned technically. The company closed above $90 per share before the Christmas holiday.

Related ETFs: IBB, BIS, BIB