The Marissa Mayer hype has been exciting and refreshing. But with Mayer and the executive suite having done little to turn around the core operations of Yahoo (YHOO), and more recently snubbing talks about tying the knot with AOL (AOL), the time may be ripe for a shakeup. Activist investor and investment management firm Starboard Value thinks so.

In an open letter to Mayer and the board of directors of Yahoo, Starboard Value announced that it has acquired a significant ownership stake in the beleaguered, and once-relevant, Internet portal. Starboard outlined a case for Yahoo to monetize the company’s non-core minority equity investments (Alibaba, Yahoo Japan) in a tax-efficient manner and tie-up with AOL, which itself has been on the path toward irrelevancy for a while. The investment management firm believes that a combination of Yahoo’s core search and display businesses and AOL could result in $1 billion of synergies.

Though this sounds nice, it is not the real reason, in our view. Starboard and likely the vast majority of Yahoo shareholders are very concerned that Mayer will use the capital raised from selling a portion of its stake in Alibaba (BABA) to pursue aggressive value-destroying acquisitions in trendy and hip (but low-ROIC) technologies. Mayer’s commentary on recent earnings press releases hasn’t exactly showcased her deep understanding of finance. It has been flat-out puzzling, for example, to hear Mayer include the following statement in recent press releases: “I’m very pleased with our execution, especially as we’ve continued to invest in and strengthen our core business.” Her statement is quite a stretch considering actual financial performance at the core Yahoo business (at the time she’s uttering those words):

GAAP revenue down 5%. Revenue ex-TAC down 1%. Adjusted EBITDA down 19%. Income from operations down 39%. Non-GAAP operating income down 27%. Net earnings down 91%. EPS attributable to Yahoo down 89%. Non-GAAP EPS down 13%. Free cash flow down 73%. Cash and marketable securities down 66%.

Mayer’s lack of focus on the financials may be why activist investors are working as fast as they can to block further value-destruction. Obviously, if Mayer thinks that recent performance is great execution, then shareholders are certainly in for a disappointment with her continuing at the helm. It’s probably not an overstatement to say that the market simply has no faith in Mayer’s ability to make the right decisions—that is, to focus on return on invested capital. Starboard outlined as much in the letter: “Yahoo’s aggressive acquisition strategy…has resulted in $1.3 billion of capital spent since Q2 2012 while consolidated revenues have remained stagnant and EBITDA has materially decreased.”

Starboard goes on to say so more directly (note: fact): “This substantial valuation gap is likely due to the fact that investors currently expect Yahoo to continue its past practices of (a) monetizing its non-core minority equity stakes in a tax inefficient manner and (b) using the cash proceeds from such sales to acquire businesses at massive valuations with seemingly little to no regard for profitability and return on capital.” We think Starboard is just being polite.

The investment management firm also outlined the terrible core performance at Yahoo since Mayer took the reins:

Although Yahoo’s stock price performance over the past few years has been strong, we believe the main reason for this performance has been the significant increase in value of Yahoo’s stake in Alibaba. The appreciation in Alibaba’s valuation, which Yahoo purchased in 2005, has masked the poor performance of Yahoo’s core business…since new management was appointed in Q2 2012, revenue in Yahoo’s core Search and Display businesses has been stagnant, yet SG&A and R&D expenditures have grown by a staggering $390 million, in turn, causing EBITDA to decline by 19%.

Unlike Starboard that is advocating a tie-up with AOL to steer the combined entities to better times, we don’t think combining two inferior firms with inferior technologies and legacy issues will result in progress. Facebook (FB) has become a powerhouse for advertisers, while Google’s (GOOG) dominance in search appears insurmountable. Combining Yahoo and AOL will not change the competitive environment, and we don’t think it will brew innovation.

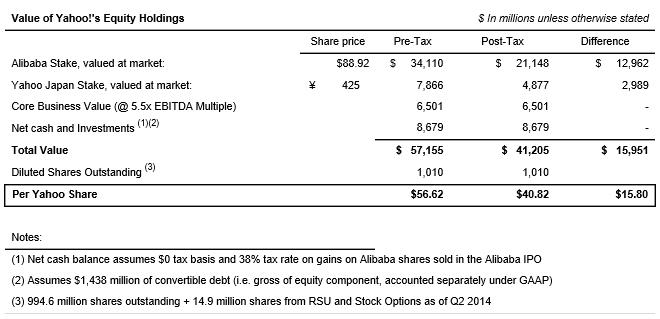

Starboard values Yahoo’s consolidated holdings and core operations at $41 per share on an after-tax basis, roughly in line with our $38 per share fair value estimate. The primary difference rests on the value assigned to Yahoo’s core operations, which we value at a slightly greater discount. On a pre-tax basis, Starboard values Yahoo at $57 per share, though it gives no specifics on how it can attain a tax-free spinoff of the firm’s non-core assets. Given the growing opposition to tax-inversions, we’re not sure that Starboard will be successful in its tax-free monetization efforts. Some taxes have to be due in any scenario, from our perspective.

Image Source: Starboard

All in, we were intrigued by Starboard’s letter, but we think the most important aspect of it rests in preventing Yahoo from making any foolish acquisitions with complete disregard to return on invested capital. A tie-up with AOL will not change the competitive environment, and we’re not sure that Starboard can completely avoid the payment of taxes, as it has alluded to in its open letter.

We think actions speak louder than words, and Yahoo’s commitment to creating shareholder value has and continues to fall short. Mayer’s experiment has failed, and it may be time for a change to a more finance-oriented leader. The high end of our fair value estimate range of Yahoo remains unchanged at $48 per share. We’d much rather own fast-growing Alibaba, however, than two struggling firms (YHOO/AOL) that have to cut costs to the bone and seek tax help in order to achieve value creation.