On Friday, General Electric (GE) and Honeywell (HON) posted solid results. GE is included in both the Best Ideas portfolio and Dividend Growth portfolio, while Honeywell is worthy of keeping a close eye on as its results shed light on the industrial sector as a whole.

Our coverage universe allows us to comment on a wide variety of firms that are held outside the actively-managed portfolios. The analyst team spends most of their time evaluating the fundamentals and financials of these firms. Though we consider the best ideas to be in the portfolios, we also see the tremendous value in commenting on companies that are not directly included in the portfolios. We also provide extensive valuation and dividend analysis of these firms in their 16-page reports and dividend reports.

Please be sure to take advantage of all of the research available on our website for the companies that are of interest to you. Whether you’re evaluating the Dividend Cushion ratio of a 6%+ dividend-yielder to assess its dividend safety and growth prospects, or evaluating a firm’s investor sentiment via technical and momentum analysis in the TradingView charting technology, there is a lot of information for every type of investor on the website. Most importantly, access to the analyst staff is a critical part of the research services. If you’re not sure ‘why we think this’ or ‘why this number is that,’ please just ask us.

Before we dig into General Electric’s and Honeywell’s earnings, we wanted to mention that it’s good practice to get a feel for how we think about each firm’s fundamentals and valuation via the 16-page reports and dividend reports before reading any commentary or article about them on the website. For one, we can’t possibly include all of our thoughts in every earnings or event-update note every single time. This would become quite repetitive, and we wouldn’t be able to get you the incremental information immediately. Hosting 16-page reports and dividend reports separate from the commentary on the website is somewhat different than what you might find on other sites. However, we think it’s the best way to get the most relevant information to you in the most efficient manner. You can access a video that walks through the features of the 16-page report here (it’s less than 5 minutes).

The reports can be accessed by using the ‘Symbol’ search box in the website header – just type in the ticker symbols ‘GE’ or ‘HON’ for example. After selecting ‘Search’, you will be directed to their landing pages, where we house the TradingView charts, their reports, the latest Valuentum commentary on them, and each firm’s press releases. You can view a video on how to access the reports on our website here. For your convenience in this article, the links to the landing pages of General Electric and Honeywell can be accessed here and here. Some of the newsletter-only members are surprised we also have full coverage of companies on our website. Please don’t forget about this core feature of the service.

With all of that said, let’s get to General Electric’s second-quarter report. GE continues to benefit from strong industrial demand as it diversifies away from its risky financial operations. The core of our thesis on the company is that the market is not giving GE enough credit for industrial strength and is still valuing the firm as if it were a risky financial, as arguably it was heading into the Great Recession, when it was forced to cut its dividend.

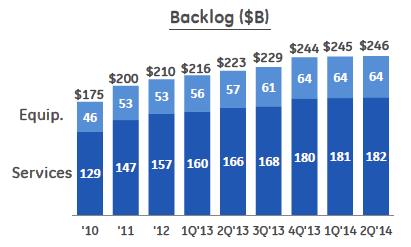

The firm’s quarterly report reflected a $23 billion increase in its backlog of unfulfilled industrial orders, industrial organic revenue expansion of 5%, 20 basis points of margin improvement, and segment profit growth of 9%. Management was quick to note that “the environment continues to be generally positive.” Importantly, the firm is making progress with the Alstom deal and decreasing the size of GE Capital’s non-core portfolio—both supporting our investment thesis on the company:

The firm’s quarterly report reflected a $23 billion increase in its backlog of unfulfilled industrial orders, industrial organic revenue expansion of 5%, 20 basis points of margin improvement, and segment profit growth of 9%. Management was quick to note that “the environment continues to be generally positive.” Importantly, the firm is making progress with the Alstom deal and decreasing the size of GE Capital’s non-core portfolio—both supporting our investment thesis on the company:

During the quarter, GE’s offer for Alstom’s Power and Grid businesses was accepted by the Alstom board and approved by the French government. It is proceeding to works council consultations and is subject to Alstom shareholder approval and customary regulatory approvals. The deal is targeted to close in 2015. GE expects Alstom to be accretive to earnings in 2015, and add $0.06 to $0.09 per share in 2016. This will accelerate the Company’s portfolio strategy to achieve 75% of earnings from its Industrial business by 2016.

GE Capital continued its strategy to decrease the size of its non-core portfolio. ENI (excluding cash and equivalents) was at $371 billion at quarter-end, down $2.4 billion from last quarter and down 5% from the year-ago period. General Electric Capital Corporation’s (GECC) estimated Tier 1 common ratio (Basel 1) rose 51 basis points from the year-ago period to 11.7%, and net interest margin was strong at 5%. Through the first half of the year, GECC has returned $1.4 billion in dividends to the parent. GECC recorded tax benefits in the quarter to reflect a lower expected tax rate for 2014, primarily driven by its planned tax-efficient disposition of the consumer bank in the Nordics.

GE is also announcing today that it is targeting the IPO of its North American Retail Finance business (Synchrony Financial) for the end of July, the first step in a planned, staged exit from that business.

GE remains on track with its simplification goals, and we’re very pleased with the order momentum in its industrial operations. We’re expecting strong dividend growth from the company in coming years, particularly as it monetizes non-core financial assets and benefits from growth in the cash-rich profile of its industrial operations.

Honeywell’s second-quarter results reinforced GE’s views of a generally positive operating environment for global industrials. Organic growth at Honeywell advanced 3% while earnings per share leapt 8% thanks to a 110 basis-point improvement in its operating margin (segment margins advanced 60 basis points). Cash flow from operations improved 7%, while free cash flow increased 5% from the same period a year ago. Honeywell is also benefiting from a robust backlog in its long-cycle businesses, though revenue will be a little lighter than previously expected for the full year. However, the industrial giant raised the bottom end of its 2014 proforma earnings-per-share guidance by $0.05 (now $5.45-$5.55, was $5.40-$5.55) on expectations of improved organic growth and continued margin improvement during the second half of the year.

Valuentum’s Take

General Electric’s performance continues to reinforce our investment thesis on the company, and we like what we saw with respect to Honeywell’s outlook for the remainder of 2014. Though both firms are fantastic companies, we’re comfortable holding GE in the actively-managed portfolios at present. GE sports a ~3.3% dividend yield. Other industrials exposure includes Ford (F) and Precision Castparts (PCP) in the Best Ideas portfolio and Emerson Electric (EMR) in the Dividend Growth portfolio.

Interested in higher-yielding equities? Inquire about our Dividend100 publication. Please don’t forget to take advantage of the most important aspect of the services: access to the analyst team.