They say ‘a picture is worth a thousand words,’ and the following snapshot may be worth a million. We like Realty Income (O) for the steady dividend increases and flexibility it provides income investors with a monthly (not quarterly or semi-annual) dividend payout.

Image Source: Realty Income

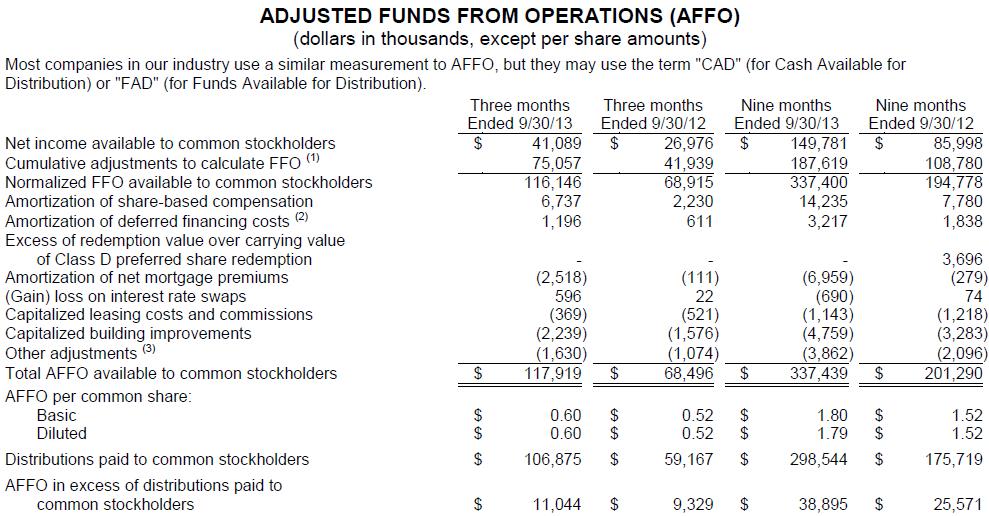

Third-quarter performance from the ‘Monthly Dividend Company,’ released Thursday, only reinforces the reasons why we hold the company in the portfolio of our Dividend Growth Newsletter. Internals during the period were fantastic — same store rents advanced 1.3% and portfolio occupancy jumped to 98.1% from 97%. The company posted adjusted funds from operations (AFFO) of $0.60 per diluted share in the quarter, comfortably above the cash dividends of $0.545 issued during the period. We also liked that ‘AFFO in excess of distributions paid to common stockholders’ advanced on a year-over-year basis ($11 million versus $9.3 million in the prior-year period) — bottom line of image below.

Image Source: Realty Income

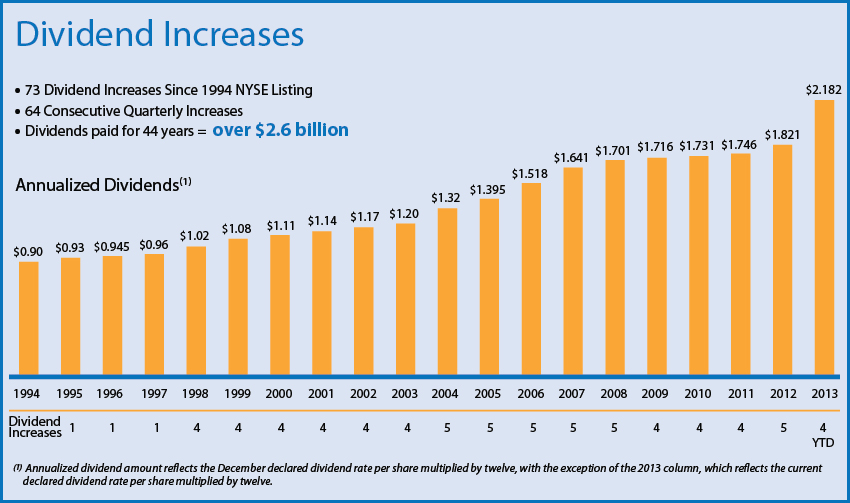

Realty Income also issued solid AFFO guidance for 2014 — $2.53-$2.58 per share, up 5%-8% from the $2.38-$2.42 per share range expected in 2013. The 2014 target range covers the company’s $2.182 annualized dividend quite well, paving the way for multiple dividend increases during 2014. We think income investors will be quite pleased with Realty Income next year.

Valuentum’s Take

We view Realty Income as a core position in the portfolio of our Dividend Growth Newsletter. The firm continues to diversify its tenant base, with the largest 15 tenants now accounting for 44.4% of portfolio rental revenue (down from more than half). FedEx (FDX), Walgreens (WAG), Family Dollar (FDO) and LA Fitness are its four largest tenants. The company’s exposure to convenience stores has also fallen to 11.2% of the portfolio at the end of the period from 18.5% at the end of 2011. The firm has also reduced its dependence on casual dining restaurants (now 5% of rental revenue; was more than 13% in 2010). We like how things are progressing at Realty Income, and we may opportunistically add to our position on weakness.