Performance was far from rosy across the majors during the calendar third quarter. BP’s (BP) performance showed a 26% fall in underlying replacement cost profit, Exxon Mobil’s (XOM) third-quarter results revealed an 18% decline in earnings, Chevron’s (CVX) quarterly earnings dropped nearly 6% during the period, and Shell’s (RDS.A; RDS.B) third-quarter profit (on a current cost of supplies basis) slid 31% from the same period a year ago. Only ConocoPhillips’ third-quarter results (COP) showed adjusted earnings expansion during the quarter (about 7%).

Source: Valuentum

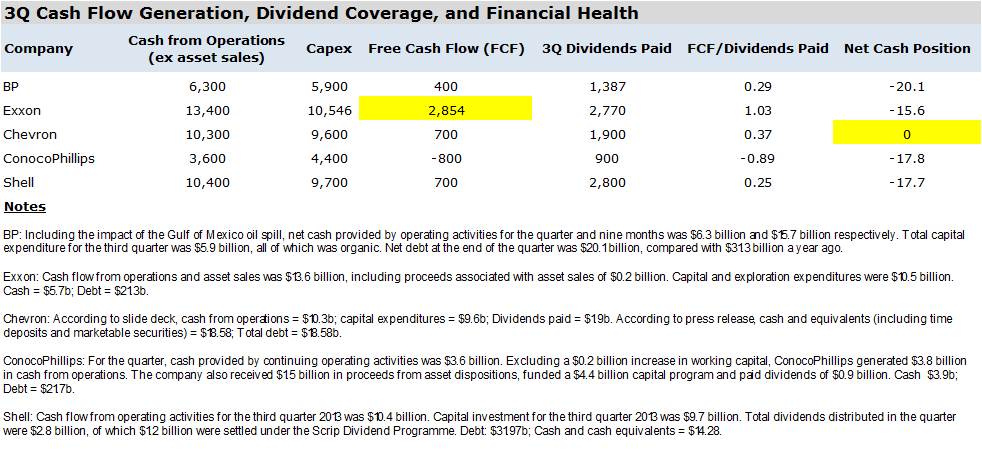

The investment landscape in the ‘Major – Oil & Gas’ space remains mixed, in our view. We liked ConocoPhillips third-quarter results, but its hefty capital investment plan and net debt position certainly don’t speak of equity resiliency in the face of the next inevitable economic downturn (and/or declining liquids pricing). Exxon’s free cash flow measures continue to be remarkable, but its stock price isn’t yet trading at a steep enough discount to its intrinsic value for us to get excited (see its 16-page report). Chevron’s third-quarter performance wasn’t fantastic, but the firm boasts the strongest balance sheet by a landslide (its net debt position is practically negligible). This affords Chevron tremendous strength and flexibility during the depths of the energy cycle to continue raising its quarterly dividend payout and/or scoop up assets at depressed prices. We consider this investment environment as mixed.

Valuentum’s Take

From a fundamental perspective, the global economic environment for the oil and gas majors remains constrained. Exxon Mobil perhaps best described the current trajectory of underlying trends in the industry in its third-quarter slide deck:

a) Moderate US economic growth

b) China’s growth rate improved modestly

c) Europe’s economic conditions uncertain

d) Higher crude oil and lower natural gas prices

e) Global industry refining margins deteriorated significantly

f) Stronger chemical commodity margins

Still, ConocoPhillips’ strong quarterly performance suggests succeeding in this environment is not out of the reach of constituents. We continue to hold Chevron in the portfolio of our Dividend Growth Newsletter as a result of its unrivaled financial flexibility, which we view as a necessity for any dividend-payer in a commodity-producing industry.