J.C. Penney (JCP)

We believe J.C. Penney (click ticker for report: ) is one of the most overpriced – if not, the most overpriced – stock on the market today. Based on our cash-burn analysis, we think the firm has sufficient liquidity to remain a going concern only through mid-2014, where the threat of bankruptcy will become severe (absent a significant change in the trajectory of cash flows). The firm’s shares register the worst score of a 1 on the Valuentum Buying Index and are suffering greatly today. We expect downside to the low-single-digits per share and perhaps worse. Our fair value estimate at the time of this writing is $3 per share.

Shares are down nearly 8% today at the time of this writing.

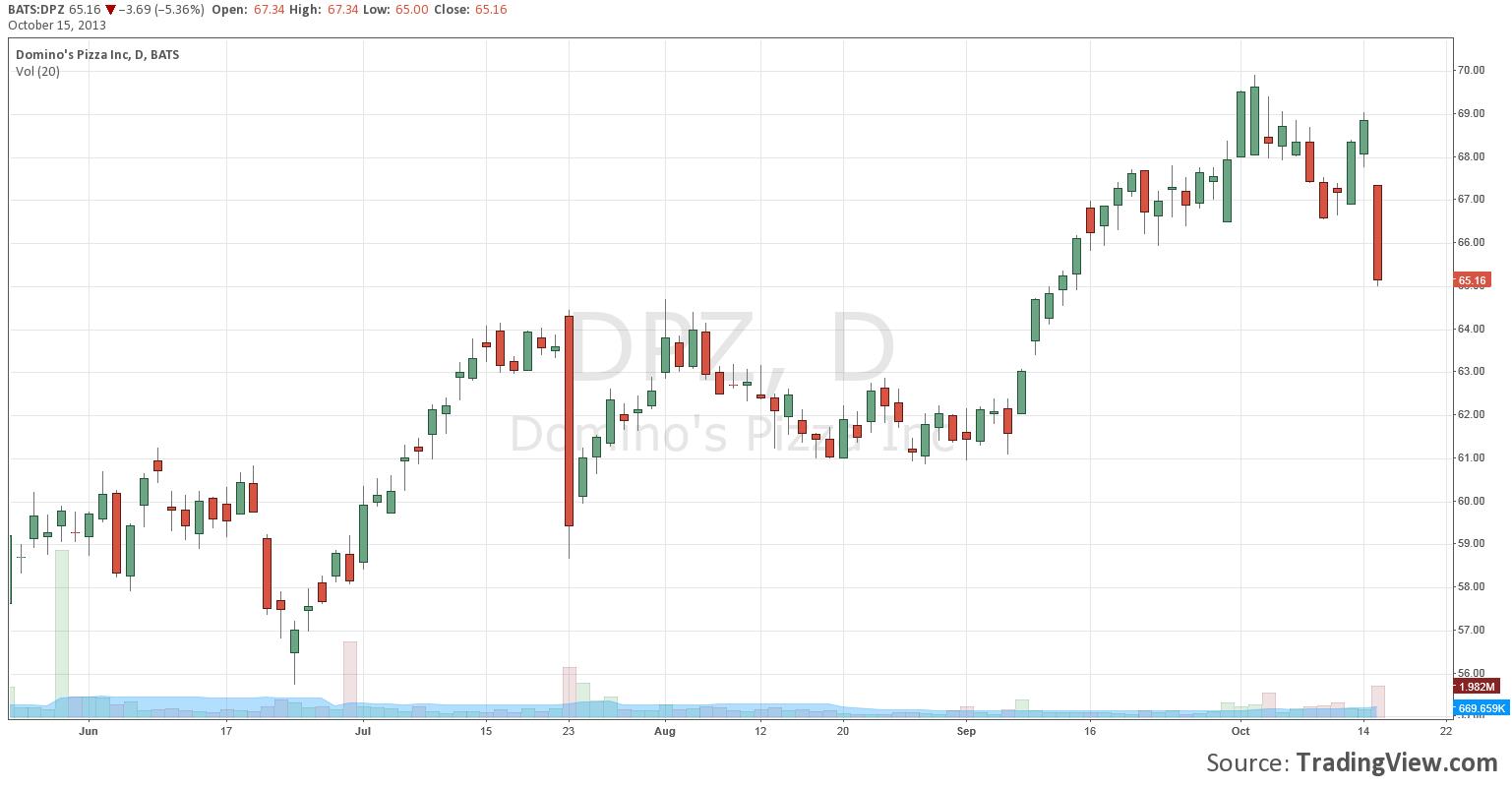

Domino’s Pizza (DPZ)

Domino’s Pizza (click ticker for report: ) reported weaker-than-expected third quarter results Tuesday, and we think expectations have been ratcheted up a bit too high for the number one pizza delivery-company in the US. Though the third-quarter bottom-line miss was fundamentally minor, when momentum starts to turn on high-flying overpriced stocks, the bottom is typically much lower than here. Based on our estimates, Domino’s is trading at more than 25 times this years’ earnings and boasts a price-earnings-to-growth (PEG) ratio north of 2.5, both measures higher than the firm’s peer median of 20 and 1.7, respectively. The high end of our fair value range for Domino’s is $50 per share, and we would not be surprised to see the company trade down to that level on any broader market weakness. It remains one of the most overvalued stocks on the market.

Shares are down more than 5% today at the time of this writing.

Valuentum’s Take

A score of 1 on the Valuentum Buying Index reveals that a firm is not only overpriced but also that shares have poor pricing momentum (and may continue to head south). In the case of J.C. Penney, we think the firm is headed to bankruptcy (and remains a high-conviction idea), and while Domino’s fundamentals aren’t terrible, we think the Street is factoring in too optimistic long-term assumptions. We’re strongly considering opening a put option in the portfolio of our Best Ideas Newsletter on J.C. Penney, and we intend to steer clear of Domino’s shares.