Image Source: Teva

Let’s cover some ground on Teva Pharma’s (TEVA) third-quarter report.

By Brian Nelson, CFA

What management said:

“This has been a year of transition for Teva, underscored this quarter by the close of our strategic acquisition of Actavis Generics, which had significant contribution to our results. Actavis will continue to contribute in a meaningful way to the future growth of our generics business through the strengthened R&D capabilities and complementary pipeline and portfolio, and enhance our leadership in an increasingly evolving industry,” stated Erez Vigodman, Teva’s President and CEO. “We were also pleased to report this quarter that we have successfully completed the second pivotal phase three study for SD-809 for tardive dyskinesia and plan to submit that NDA to the U.S. FDA at the end of this year, and have also resubmitted SD-809 for Huntington disease in response to the FDA’s Complete Response Letter. Going forward, we will focus on also growing our specialty pipeline through in-house opportunities, including in the development and commercialization of our key pipeline assets, most notably our anti-CGRP product for migraine headaches and fasinumab. In the face of the industry and company-specific challenges we have been dealing with this year, we remain excited about the future as we strive to create a platform that is unique to the industry, working every day to find the delicate balance between access and innovation and laying the foundation for Teva’s continued growth.”

The scoop:

Teva’s third-quarter performance, released November 15, was messy. The contribution of the Actavis generics business muddied the organic growth calculation, while despite the acquisition-related expansion, GAAP reported gross profit was essentially flat. On a non-GAAP basis, gross profit jumped 14%, essentially matching the rate of all-in year-over-year revenue growth in the quarter, however. Both research and development (R&D) and selling and marketing (S&M) spending advanced at a pace faster than top-line growth in the quarter, pressuring GAAP reported operating income, which fell to $0.8 billion (down 24% compared to $1 billion in last year’s period). However, quarterly non-GAAP operating income leapt 16%, to $1.6 billion, after adjusting for legal settlements, loss contingencies, and one-time acquisition-related items.

The company’s generics medicines revenue (~52% of total) increased 35% on a year-over-year, local-currency basis, propelled mostly by business outside the US and Europe (Rest-of-World generic sales increased 60%). Generic medicine gross profit jumped ~45%, while generic medicine segment profit leapt 50% thanks for the most part to the Actavis combination. Specialty medicines revenue fell 6%, a decline largely expected, as its blockbuster multiple sclerosis drug Capaxone itself continues to face generic competition, with sales of the therapy sliding a better-than-expected 2% during the period (many had been expecting worse). The decline in specialty medicines revenue was across the board in the quarter, however, in all of Teva’s “core therapeutic areas.” Specialty medicine gross and segment profit was essentially flat and down 10%, respectively.

Teva’s cash flow from operations advanced to $1.5 billion in the quarter, an increase of 34% compared to the same period a year ago. Free cash flow was $1.2 billion, up 27% on a year-over-year basis. Cash on the balance sheet stood at $2.7 billion, while debt stood at $36.9 billion, the latter up $26 billion largely as a result of the Actavis acquisition. Shares outstanding on a non-GAAP basis, including the potential dilution resulting from mandatory convertible shares, were 1.044 billion at the end of the third quarter. Total revenue for 2016 is expected in the range of $21.6-$21.9 billion, while non-GAAP earnings per share for the year is targeted at $5.10-$5.20. Teva expects cash flow from operations of as much as $5 billion for 2016.

Insight from the quarterly conference call:

“The completion of the Actavis acquisition strengthens and broadens our R&D capabilities and highly complements our product pipeline, product portfolio, geographical footprint, and our operational network. It enhances Teva’s leadership in an evolving competitive landscape and massive consolidation across our customer base. In addition, our integration plans with the Actavis Generic business are on track.” – CEO Erez Vigodman

“For our specialty business, this means successful execution in the development and commercialization of our key sites and assets, most notably our anti-CGRP product for migraine and SD-809 in fasinumab. And further expanding our pipeline to in-house development programs, by the same time, we’ll continue to protect Copaxone in multiple ways. 2017 will be an important year for Copaxone as we await the decision of the local and several patents for technical patent possibility. It is our intention now to focus on using our cash flow to pay-down our current level of debt. Today, we benefit for an investment grade rating and it is very important for Teva that we maintain it and even make it stronger over time.” – CEO Erez Vigodman

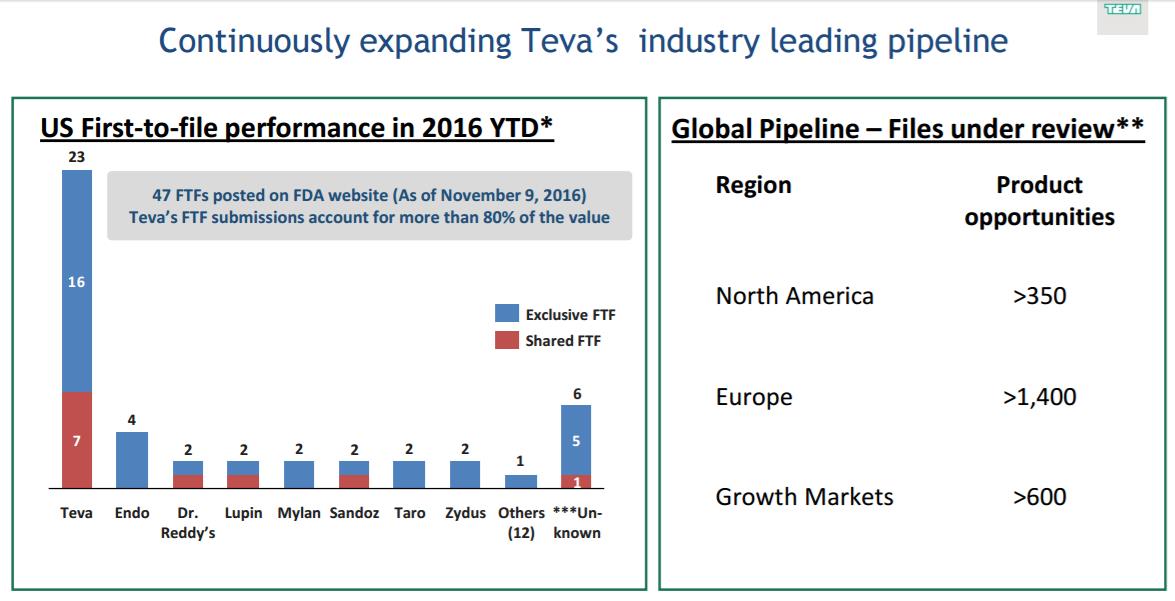

“…we continue to lead the industry in the U.S. On first-to-files, which is still a significant value driver in the U.S. generic market, this year, Teva has received confirmation of 23 new first-to-files, which is approximately half of the total number posted by the FDA, and more than 80% of the total first-to-files brand value posted in 2016. 10 of these past 23 first-to-files procured in third and fourth quarter, and we hope for several more by year-end. New launches are the life-blood of any generics business and are key to any company’s ability to grow, both the top and bottom-lines. With the acquisition, Teva now has more than 2,000 product registrations pending approval around the world, and we have significant value in our more than 100 confirmed first-to-files for the U.S. markets.” – CEO Erez Vigodman

“In closing, we strongly believe in the generic industry for the long-term, despite the current volatility. With our recent investments, Teva is the best positioned company in terms of market presence, manufacturing capabilities, and pipeline, and I see this business growing mid-single digits going forward.” – CEO Erez Vigodman

Are we changing our mind with our position?:

There are a handful of reasons Teva’s stock has been under significant pressure.

First, selling pressure in advance of the news alleging potential price fixing among generic pharma entities was likely severe during the past few months with many close to the situation in the know, “Trouble Developing for Generic Pharma Stocks?” Regulatory and legal risks are unpredictable, and the outcome and potential damages to Teva remains so. We don’t think the end-game is a tragic one to Teva, however.

Second, Teva’s reported performance continues to be opaque with a lot of moving parts, and we suspect many on the buy side of the investment industry are waiting for cleaner results to get a better feel for the long-term earnings power of the combined entity (Teva-Actavis). This will only take time and is partly why shares continue to trade at ~7 times current-year non-GAAP earnings, while most of the market bolsters a 16+ times multiple.

Third, the debt load associated with the Teva-Actavis tie-up is substantial, and while Teva retains an investment-grade credit rating and phenomenal free cash flow generation capacity to pay down debt, many have stepped to the sidelines in light of the outsize leverage. Debt-to-EBITDA stood at 5.4 times at the end of the quarter, but management expects this to improve considerably to 3.5 times as quickly as possible to retain its BBB credit rating.

Fourth, Teva continues to face pressure in its specialty medicines business, and while multiple sclerosis drup Capaxone is performing better-than-expected, new developments in the pipeline haven’t been coming at a fast enough pace to satisfy market participants. Long-term uncertainty related to the Capaxone franchise, a huge profit driver, will remain a concern.

While we are very disappointed with Teva’s recent share-price performance, even if we didn’t act in advance of the price-fixing news, we should have probably moved to the sidelines in light of the company’s debt load. But hindsight is 20-20, and we have to think about what to do now. Right now, Teva’s shares are cheap, the company has a fantastic long-term opportunity in generics, and generates gobs of free cash flow that will be used to deleverage the balance sheet. In light of Teva’s rather small weighting, we’re going to keep exposure to shares in the Best Ideas Newsletter portfolio as the story continues to evolve.

Related tickers: RDY, MYL, TARO