By Brian Nelson, CFA

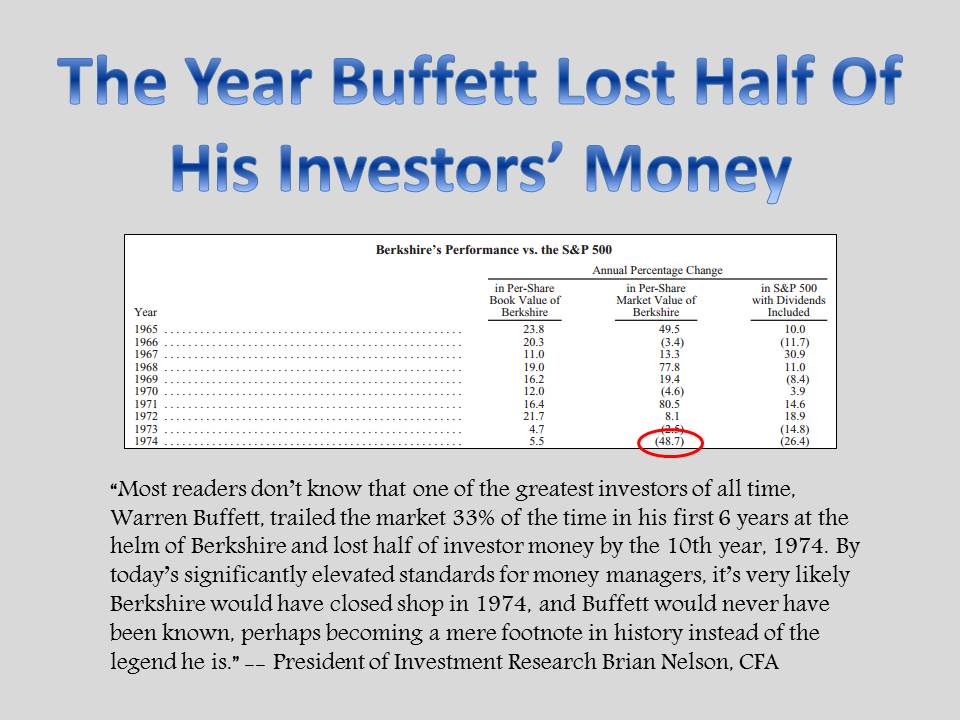

It’s always a wonder to open up on the Berkshire Hathaway (BRK.A, BRK.B) annual report for a large variety of different reasons, but every time I do I can’t help but ponder yesteryear through the table on page 2, “Berkshire’s Performance vs. the S&P 500.”

I think I have a unique knack for imagining what might have been if today’s standards would have been applied to Berkshire in the 1970s, perhaps in some ways how many baseball fans may think about whether the legends of the past would have put up the type of numbers that they did if presented with today’s dynamics. For example, would Joe DiMaggio have really been able to hit safely in 56 consecutive games if he had to face the likes of today’s talent, the set-up man, and the 100mph fastball yielding closer, “Why Joe DiMaggio’s 56-Game Hit Streak Is So Enduring.” What about Ted Williams? Would the “Splendid Splinter” have been able to hit over .400 in 1941, the last player to do so? What about the “splitter” pitch and the scouting that goes on, the shifts, and more? Would DiMaggio or Williams have performed as well under today’s elements?

The answer, in my view, is no.

The same can be said for the Oracle himself. Times have changed – the elements of investing have changed. The sheer availability of information, the timeliness of the distribution of information, the inter-connectedness and global systematic nature of the markets makes today’s dynamics all the more difficult to outperform. Capital was scarce in the 1970s, 1980s when the federal funds rate was a whopping 20% — hurdle rates on businesses and projects were higher. Investors and entrepreneurs alike had to deliver in a big way – a 20% return on invested capital is a high mark that very few S&P 500 companies can deliver on consistently through the course of an economic cycle.

Today, we effectively have “free” money with most of the world engaging in negative interest rate policy (NIRP) – “negative” hurdle rates. It is much harder today for the entrepreneur, the investor, to compete against the capital waste that goes into failed new start-up after failed new start-up. Google (GOOG, GOOGL) alone spends hundreds of millions on a line item called “other bets.” There are companies that have been running at losses for years, burning through cash that wouldn’t have been available to do so in the 1970s, 1980s just to grow – think Twitter (TWTR) and Tesla (TSLA) as quintessential examples.

These companies wouldn’t have been given a chance a number of decades ago, and such capital excesses continue to destroy otherwise economically-viable institutions. Twitter, for one, has only contributed to the declines of traditional newspaper circulation. For years, Amazon (AMZN) destroyed big box retail while operating near break-even or worse. Today, everyone has become an investment analyst, similar to the late 1990s during the dot-com bubble when everyone was a day trader – some quitting their jobs to do it full time. Today’s writers are now competing for followers, not dollars. The world has been turned upside-down, and raw talent is being drowned out by the capital excesses that only result in economic value-destruction as they destroy otherwise viable businesses. How awesome must a small, extremely talented team be to compete with the millions of dollars thrown at “the next big thing” that Google thinks up in a similar vertical? Today’s entrepreneurs must be superstars to make it big with so much capital chasing every little bit of excess return.

But perhaps to the point, a completely unproven Warren Buffett in the 1970s, after trailing the market a decent amount during the 1960s and losing half of his investors’ money in 1974, somehow managed to keep his investors onboard with him. Remember, the Warren Buffett of 1974 didn’t have the reputation he has today, meaning that there’d be nothing for shareholders to hang on to for comfort, to give them confidence in a turnaround. It’s my contention that based on today’s elevated standards for money managers, Warren Buffett’s Berkshire Hathaway would have closed down in the mid-1970s, and the Oracle himself would have been a mere footnote in history, not the legend that he has become. Oh how the table on page 2 reminds me of this every time I try to explain the ups and downs of the market to new readers. Only when they see just how terribly Mr. Buffett performed in his first 10 years do they understand that this business is not an easy one – and the best investors just like the best baseball players do not bat 1.000.

We left off in Part II here with the Oracle’s ever-optimistic views on America, and we’re going to push forward in this Part III in similar format, picking select excerpts from Mr. Buffett to highlight and then comment on: the Oracle’s words in italics, mine in regular type. Berkshire’s full “2015 Letter to Shareholders” can be downloaded here. Let’s go ahead and finish up this three-part series.

…Berkshire (and, to be sure, a great many other businesses) will almost certainly prosper. The managers who succeed Charlie and me will build Berkshire’s per-share intrinsic value by following our simple blueprint of: (1) constantly improving the basic earning power of our many subsidiaries; (2) further increasing their earnings through bolt-on acquisitions; (3) benefiting from the growth of our investees; (4) repurchasing Berkshire shares when they are available at a meaningful discount from intrinsic value; and (5) making an occasional large acquisition. Management will also try to maximize results for you by rarely, if ever, issuing Berkshire shares.

Mr. Buffett’s blueprint for continued success at Berkshire is a rather simple one, but there is one point that I want to make sure all readers understand, and that is point 4. We’ve written extensively about the concept of price versus intrinsic value in the past, but it bears repeating.

Price is what you pay for something – while value, as measured by the company’s net balance sheet and the discounted value of the entity’s future free cash flows, is what you get. The Oracle lays out this dynamic explicitly in point 4 by emphasizing that when Berkshire shares are available at a meaningful discount (to) intrinsic value, they’re worth repurchasing.

Repurchases typically only make sense in this context, and I point to the following article for further reading on this point, “Understanding Share Buybacks.” Please do spend some time nailing down this concept.

Intrinsic Business Value: As much as Charlie and I talk about intrinsic business value, we cannot tell you precisely what that number is for Berkshire shares (nor, in fact, for any other stock). It is possible, however, to make a sensible estimate.

Mr. Buffett’s genius shines through in the above excerpt. A core part of the Valuentum process rests on enterprise free cash flow valuation, and by extension, the idea of employing a fair value range when evaluating the intrinsic worth of shares. Why might we do this?

The answer is straightforward. The future cash flows generated by a company are inherently unpredictable to a degree, and because a company’s intrinsic worth will always be based in part on these future free cash flows, a company’s true intrinsic worth must be a range, a fair value range – one that reflects the range of future free cash flows or the cone of probable future free cash flows. Fair value can never be a point estimate, a result that ignores the concept of uncertainty and the undeniable fact that future reality will almost always differ from forecasted expectations.

The first component of the Valuentum Buying Index considers whether a company is trading above, below or within its fair value range to determine whether shares are overvalued, undervalued or fairly valued, respectively. We publish fair value estimates, but we embrace the fair value range, also known as a margin of safety. For further reading, please have a look at step 9 in my “13 Most Important Steps to Understand the Stock Market.” If you haven’t read it yet, please do so after completing this three-part series.

Since 1970, our per-share investments have increased at a rate of 18.9% compounded annually, and our earnings (including the underwriting results in both the initial and terminal year) have grown at a 23.7% clip. It is no coincidence that the price of Berkshire stock over the ensuing 45 years has increased at a rate very similar to that of our two measures of value. Charlie and I like to see gains in both sectors, but our main goal is to build operating earnings.

Just one quick point.

There’s nothing wrong with investing for income, or focusing on the dividend, but we think it is worth emphasizing, as Mr. Buffett mentions above, that long-term equity returns are highly correlated to operating earnings. This excerpt serves as a good reminder not to fall into the trap of relying on a financially-engineered distribution or a dividend that may make little sense in the context of a company’s future free cash flows and balance sheet position. If the distribution or dividend is not backed by tangible earnings and/or traditional free cash flow, as measured by cash flow from operations less all capital spending, then the distribution or dividend is not likely to make it over the long haul. The balance sheet matters, too.

…the wish of all insurers to achieve this happy result creates intense competition, so vigorous indeed that it sometimes causes the P/C industry as a whole to operate at a significant underwriting loss. This loss, in effect, is what the industry pays to hold its float. Competitive dynamics almost guarantee that the insurance industry, despite the float income all its companies enjoy, will continue its dismal record of earning subnormal returns on tangible net worth as compared to other American businesses. The prolonged period of low interest rates the world is now dealing with also virtually guarantees that earnings on float will steadily decrease for many years to come, thereby exacerbating the profit problems of insurers. It’s a good bet that industry results over the next ten years will fall short of those recorded in the past decade, particularly for those companies that specialize in reinsurance.

We have nothing further to add – today’s insurance business is a tough one, and the Oracle outlines why we do not include any insurer, besides Berkshire itself, in any newsletter portfolio.

Regulated, Capital-Intensive Businesses. A key characteristic of both companies is their huge investment in very long-lived, regulated assets, with these partially funded by large amounts of long-term debt that is not guaranteed by Berkshire…All told, BHE and BNSF invested $11.6 billion in plant and equipment last year, a massive commitment to key components of America’s infrastructure. We relish making such investments as long as they promise reasonable returns – and, on that front, we put a large amount of trust in future regulation.

Our confidence is justified both by our past experience and by the knowledge that society will forever need huge investments in both transportation and energy. It is in the self-interest of governments to treat capital providers in a manner that will ensure the continued flow of funds to essential projects. It is concomitantly in our self-interest to conduct our operations in a way that earns the approval of our regulators and the people they represent.

We have to make an important distinction.

Return on “new” invested capital is the holy-grail metric that measures the efficacy of any capital-allocation endeavor. As Mr. Buffett mentions, for largely regulated entities, capital investment can be a rather good thing, as regulators apply a fixed return-on-equity to the new capital put in place, ensuring a nice stream of profits…long into the future. For regulated utilities, this is the way of life. For railroads, however, not so much – as their economics are still tied to the vicissitudes of the economic cycle and end market exposure (just look at the performance of coal carloads as of late), but that’s not the distinction we are looking to iron out in this commentary.

What we want to emphasize, and this may be confusing for readers focused primarily on utilities and energy-related equities where investment and acquisitions are championed, not all capital investment is a good thing! All else equal, a company that generates massive returns on “new” invested capital, as in an Economic Castle, “What Is An Economic Castle?,” via minimal capital investment is far better than one that may only general marginal excess economic returns but needs massive capital outlays to do so. The more earnings generated from each dollar invested, the better. Lower capital requirements in any form also means there is more left to reinvest into high-return opportunities to further grow operating earnings, generating a virtuous cycle of value-creation.

The study of entities that are dependent on massive capital investment to grow regulated earnings muddies this very basic financial concept, but it’s so important to emphasize that equities that require very little capital to generate tremendous amounts of free cash flow are often the best types of businesses. A list of such Economic Castles can be found here.

Wall Street analysts often play their part in this charade, too, parroting the phony, compensation-ignoring “earnings” figures fed them by managements. Maybe the offending analysts don’t know any better. Or maybe they fear losing “access” to management. Or maybe they are cynical, telling themselves that since everyone else is playing the game, why shouldn’t they go along with it. Whatever their reasoning, these analysts are guilty of propagating misleading numbers that can deceive investors.

There is a tremendous problem with non-GAAP reporting this day and age, and we highlight our biggest pet peeve in the misnomer distributable cash flow, “Valuentum Applauds SEC’s move to Evaluate Non-GAAP Reporting.”

Not only is distributable cash flow a big problem as we outlined in our thesis on Kinder Morgan (KMI), but investors placing elevated multiples on inflated non-GAAP earnings forecasts is perpetuating a very ominous scenario for the broader market.

On a side note, I really like to see such passion in Mr. Buffett’s writing. Sometimes I feel like I’m being offensive with some of the things I write about (and how I write them), but it’s good to be in good company with the Oracle. I’m glad we share some of the same pet peeves.

Depreciation charges are a more complicated subject but are almost always true costs. Certainly they are at Berkshire. I wish we could keep our businesses competitive while spending less than our depreciation charge, but in 51 years I’ve yet to figure out how to do so. Indeed, the depreciation charge we record in our railroad business falls far short of the capital outlays needed to merely keep the railroad running properly, a mismatch that leads to GAAP earnings that are higher than true economic earnings. (This overstatement of earnings exists at all railroads.) When CEOs or investment bankers tout pre-depreciation figures such as EBITDA as a valuation guide, watch their noses lengthen while they speak.

The Oracle is once-again spot-on in this excerpt.

Just like the misnomer distributable cash flow excludes the very growth capital expenditures that drive future net income, which is included in distributable cash flow, EBITDA completely ignores the depreciation and amortization charges associated with the capital put in place. Certainly EBITDA can be used for relative valuation measures, but doing so only opens up the possibility of systematic overvaluation, much like what happened to the energy MLP (AMLP) universe prior to its collapse in late 2015.

Companies that are pulling back capital investment below depreciation are underinvesting in their businesses, perhaps the best example of this is J.C. Penney (JCP) at the moment. Eventually, this catches up with them.

Of course, a business with terrific economics can be a bad investment if it is bought at too high a price.

Yes, yes, yes.

Not all good businesses are good investments. Price will always matter. Just like one wants to buy groceries at the supermarket when they go on sale, one should want to buy stocks when they go on sale, too. There’s no away around a robust, forward-looking intrinsic value process and comparing that cash-flow-derived outcome to the share price to determine whether a good investment opportunity exists. If you understand this, you’ll never fall into the trap of overpaying for a business again.

In the closing of Part III, we’ll list the 15 common stock investments held at Berkshire Hathaway. I hope that you have enjoyed this series.

American Express (AXP), AT&T (T), Charter Communications (CHTR), Coca-Cola (KO), DaVita (DVA), Deere (DE), Goldman Sachs (GS), IBM (IBM), Moody’s (MCO), Phillips 66 (PSX), Procter & Gamble (PG), Sanofi (SNY), US Bancorp (USB), WalMart (WMT), Wells Fargo (WFC).

Image Source: Berkshire Hathaway (2015), page 20

Thank you for reading!