Kinder Morgan’s (KMI) second-quarter results, released July 15, left much to be desired. Internal measures of distributable cash flow are coming in lower than previous expectations and its total debt continues to advance to uncomfortable levels, approaching ~5.8 times annualized EBITDA, as disclosed in the second-quarter release. Though we maintain our view that Kinder Morgan has a fantastic business model with lucrative fee-based contracts and substantial cash-flow generating capacity, the risks associated with the company’s capital structure and future dividend obligations overwhelm such positives. We remain convincingly on the sidelines; our fair value estimate of $29 per share remains unchanged.

We continue to be impressed with Kinder Morgan’s excellent levels of transparency and disclosures, but the information included in the firm’s second-quarter press release is insufficient for our application. We encourage the executive team at the company to disclose not only the firm’s cash flow statement in such quarterly communications but also a measure of non-GAAP free cash flow, as calculated by cash flow from operations less all capital spending, including both growth and maintenance capex. The cash flow statement will be included in the 10-Q, but since most investors are focused on a company-provided measure of cash flow in the report, disclosing the GAAP number would be the best route for all stakeholders. We think the presentation of such incremental information would match the high integrity of the executive team, which continues to buy back warrants despite weakening fundamentals.

As many of our readers may know, we do not believe distributable cash flow is the way to view a corporate’s true free cash flow generating capacity. Within the calculation, distributable cash flow (not to be confused with discounted cash flow, or DCF, as in the case of widely-accepted valuation techniques) ignores growth capital spending, which remains vital to the expansion of net income, which is included in distributable cash flow. This severe imbalance of “not including one thing that drives the other thing” in the presentation of underlying fundamentals has, in our opinion, allowed Kinder Morgan to fetch an equity price that is completely disconnected to a true free-cash-flow based intrinsic value estimate.

In almost all cases with corporates, an organically-derived dividend–as most investors believe should be the characteristic of any dividend–is paid out as a portion of a company’s earnings and/or as a portion of a company’s free cash flow. In the second-quarter report, Kinder Morgan’s dividend was 3.5 times its reported earnings during the period ($0.49 per share / $0.15 per share), while we estimate the company’s free cash flow less dividend payments has been -$1.2 billion (a negative $1.2 billion) during the first half of the year. We’ll be able to disclose this actual figure when the company releases its 10-Q. Though Kinder Morgan’s free cash flow is positive, it remains insufficient to cover its astronomical dividend obligations without ongoing help from the capital markets. By definition, the company’s dividend is financially-engineered, and all stakeholders should be aware of this.

From our perspective, without the help of an increasing energy resource price environment, Kinder Morgan may eventually find itself in a pinch. Though the impact is sure to vary in coming years and the spot rate of energy resource pricing remains difficult to predict with any sort of precision, our view is that the delta related to the impact of changes in energy prices on Kinder Morgan’s cash flow will be incrementally greater in coming years than they are today. Hedges at the firm will roll off to less than 40% by 2017 from ~80% in 2015, and existing hedged prices are substantially above the current spot rates. Where a $1 change in the price of crude oil impacts cash flow by ~$10 million in 2015 (and each $0.10 per MMBtu change in the average price of natural gas impacts cash flow by ~$3 million), we expect this delta to be a multiple of that in coming years.

Crude oil prices have already collapsed to ~$50 per barrel from $125 per barrel, and we cannot rule out an increasingly dire situation where crude oil prices are halved from today’s levels. Kinder Morgan disclosed in its press release that its cash flow generating levels are “below…budgeted coverage,” as they assume “an average WTI crude oil price of approximately $70 per barrel and a Henry Hub natural gas price of $3.80 per MMBtu.” Unfortunately, Kinder Morgan’s business may not be as stable as some investors would hope, and with experts calling for a $10-$20 per barrel crude-oil price environment, it’s hard for us to say the corporate’s dividend is safe. We’re reiterating our Very Poor dividend safety rating at Kinder Morgan.

In the second quarter, Kinder Morgan’s reported operating income dropped nearly 12%, while reported net income per share was practically halved from last year’s period. Total segment EBDA also fell in the period as the firm faced earnings pressure in its ‘Natural Gas Pipelines’ and ‘CO2’ business segments. On an operational basis, we think it is fair to say the quarter was weak, but we’re most concerned about the direction of its financial leverage. The company’s annualized Debt-to-EBITDA expanded to 5.8 times, up from 5.5 times at the end of last year. We don’t think Kinder Morgan will be able to delever without a potentially dilutive equity raise, as the company pays out in dividends a multiple of its free cash flow generation.

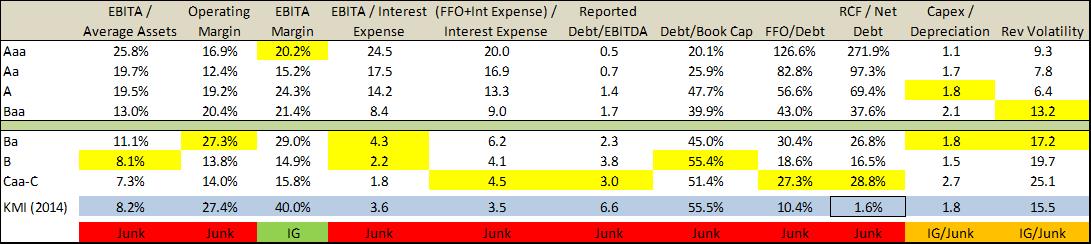

Though credit ratings are largely subjective and certainly are not dependent on one single metric, we maintain our view that Kinder Morgan’s debt is not of investment-grade quality. A Moody’s study, released December 2007, outlines a cross section of financial ratios most indicative of the rating category for global energy companies, including pipeline operators, based on most recent fiscal year-end data. Though we map Kinder Morgan’s reported 2014 results to a group of energy entities at the height of the pre-financial crisis period, we still believe such a comparison is useful in evaluating creditworthiness. When using a multi-variate approach, Kinder Morgan registers “junk” status for the vast majority of metrics. We believe Retained Cash Flow (RCF) to Net Debt is most informative of the risk debtholders bear with respect to the company’s ultra-aggressive dividend growth policy.

Source: Moody’s Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations, December 2007, Kinder Morgan regulatory filings

There are many things to like about Kinder Morgan’s cash-rich business model, but the company has simply bitten off more debt and dividend payments than it can chew. The vast majority of the firm’s operations are fee-based and predictable, but that doesn’t mean it is not also levered to changes in commodity prices. The second quarter showed that fundamental performance is weakening, leverage is increasing, and that energy price uncertainty has heightened–yet Kinder Morgan’s management team continues to raise the dividend, a 14% year-over-year increase in the last period. Something is coming to a head, and we don’t think it will end well for equity holders. We expect an additional 20% downside from here.