Home Depot (HD) and Lowe’s (LOW) reported calendar second-quarter results this week.

Home Depot continues to execute better than its peer, with the company witnessing strong performance in its spring seasonal business and across all geographies during the second quarter. Home Depot’s comparable sales growth of 6.4% in the US was also a full two percentage points better than Lowe’s second-quarter performance. Home Depot also upped its outlook for the remainder of the year, showcasing fantastic double-digit bottom-line expansion:

Based on its second quarter performance and its outlook for the year, the company raised its fiscal 2014 diluted earnings-per-share guidance and now expects diluted earnings per share to be up approximately 20.2 percent to $4.52 for the year. This earnings-per-share guidance includes the benefit of the company’s year-to-date share repurchases of $3.5 billion and the company’s intent to repurchase an additional $3.5 billion of shares over the remainder of the year.

As with Home Depot, Lowe’s benefited from an improvement in outdoor product sales, which were pushed back as a result of unfavorable weather conditions in the first quarter. But while Lowe’s noted improving job and income growth to drive home-improvement related sales, the company modestly reduced its sales outlook for the year. Comparable sales growth at Lowe’s for the year is now expected to be 3.5%, a level below prior guidance.

Though Lowe’s bottom-line target remained unchanged for 2014, we believe the company is not yet able to generate share gains against its larger rival. Still, total expected sales growth of 4.5% in 2014 is only a few basis points lower than that expected (4.8%) by Home Depot for its own full-year performance. So while performance has diverged a bit, both continue to benefit from strengthening industry trends.

Valuentum’s Take

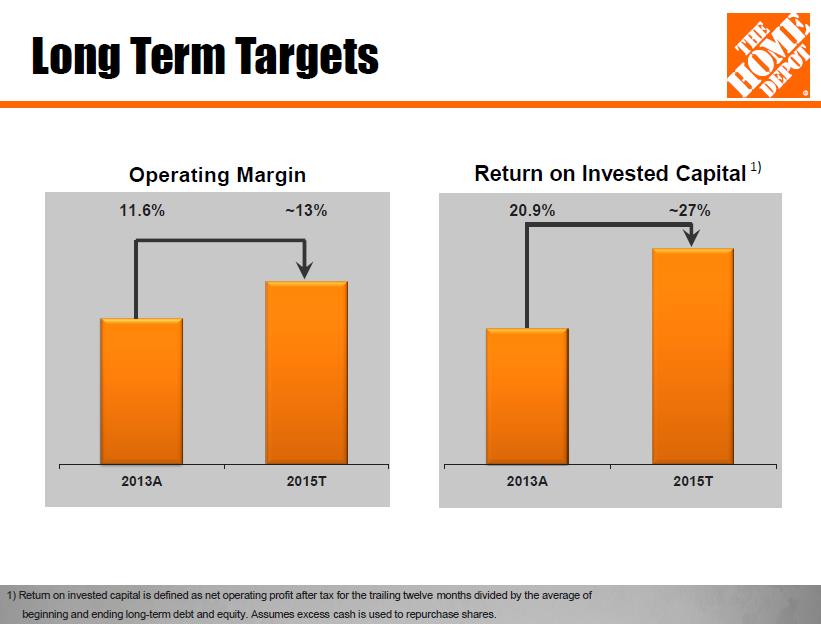

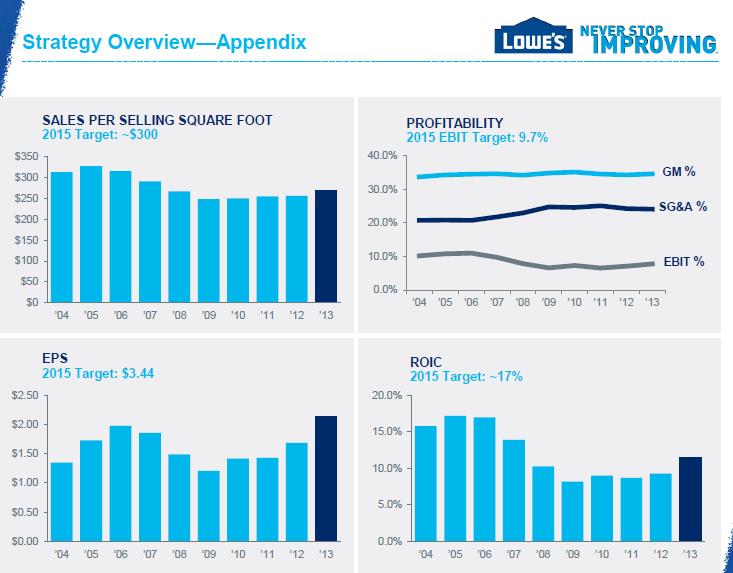

We’re huge fans of both Home Depot’s and Lowe’s focus on return on invested capital (ROIC), which is a superior measure than either return on equity (ROE), which can be impacted by financial leverage (debt), or return on assets (ROA), which can be impacted by non-operating cash on the balance sheet. Home Depot is targeting return on invested capital of ~27% by 2015, while Lowe’s targeted measure for the same year is a full 10 percentage points lower (see Appendix).

Both Home Depot and Lowe’s have strong brand names, and both are focused on satisfying customers’ needs via a service focus. The $640 billion home-improvement is large enough for both to shine, but we think Home Depot continues to execute better on a number of fronts (from comparable store sales growth to ROIC). At the time of this writing, Home Depot yields 2.3%, while Lowe’s yields 2%. We continue to prefer ideas in the Best Ideas portfolio and Dividend Growth portfolio, though we note that the dividend growth prospects of both Home Depot and Lowe’s are excellent as well.

Related Firms: LL

Appendix: ROIC

Image Source: Home Depot

Image Source: Lowe’s