We believe investors have a tremendous opportunity to be holders of Ford’s (F) equity. We can do a deep dive into the reasons why in this article, but we encourage members to peruse our website, especially Ford’s landing page to examine our investment thesis on the automaker. On Ford’s landing page, members can view the company’s 16-page equity report and its dividend report, as well as a list of the recent Valuentum commentary on the company and the firm’s corporate press releases. Our website may be slightly different than others’ in that we house pdf reports of firms on their respective landing pages — in addition to providing articles and press releases and other content. We can’t possibly put all of our thoughts on a company in each article every time, and in many cases (like this one) we like to hit on the high points that offer incremental information to our investment thesis on a firm.

We first outlined our bullish case on Ford in August 2011, first added shares to the Best Ideas portfolio in November 2011, added to the position in May 2012 at ~$10 per share, and today, we are reiterating our view that the company is worth north of $20 per share (at the time of this writing, the firm closed just shy of $16). There have been two new and important developments in the Ford story recently that followers of the Best Ideas portfolio should be aware of – for our new members, the Best Ideas portfolio is included in each edition of the monthly Best Ideas Newsletter and represents our flagship and most popular product. First, Ford announced a $1.8 billion share repurchase program. Second, the automaker revealed that it was back on track, setting records in the month of April. Let’s address both items below.

In finance, the economic substance of any transaction is all that matters, not if a particular action is accretive or dilutive to the income statement via earnings per share. The impact on the balance sheet, which is also a source of value, cannot be ignored in any dealings. Said differently, a firm’s operations and management’s actions should be judged on the basis of economic value added, not whether or not earnings per share is enhanced. In Ford’s decision to buy back shares, the action is significantly value-creative from an economic-value standpoint. As we outline in the introductory piece “Understanding Share Buybacks,” the general rule of thumb with share repurchases is as follows: If share buybacks are completed at a price level that is under a firm’s fair value estimate, the activity is value-creating. Ford’s shares are clearly underpriced, in our view.

The activity will eventually result in the elimination of Automotive debt as most of the buyback program will be used to offset the dilutive effect of potential conversions of its 4.25% Senior Convertible Notes due November 15, 2016. Though repaying debt with cash on the books is generally value neutral, the convertible debt at this juncture is essentially equity, considering the current price of Ford’s stock relative to the conversion price. Here are the details on the hybrid instrument that will be retired:

Subject to certain limitations relating to the price of Ford Common Stock, the 2016 Convertible Notes are convertible into shares of Ford Common Stock, based on a conversion rate (subject to adjustment) of 112.8203 shares per $1,000 principal amount of 2016 Convertible Notes (which is equal to a conversion price of $8.86 per share). Upon conversion of the 2016 Convertible Notes, we have the right to deliver, in lieu of shares of Ford Common Stock, either cash or a combination of cash and Ford Common Stock.

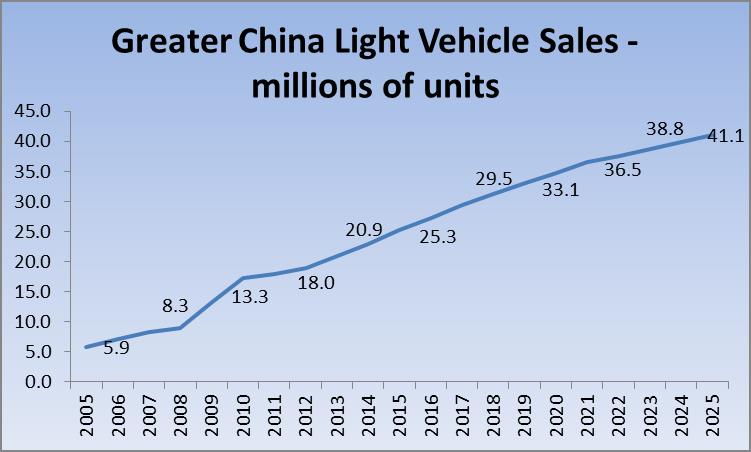

In other news, the auto giant’s April sales revealed the firm is back on track. The Ford F-Series had its best April US sales since 2006, while the Ford Explorer posted its best April sales since 2005. Though US sales declined 1% compared with last year, the number was a nice recovery from the results earlier in the year that were impacted by harsh winter weather. The automaker also noted that April China sales leapt 29% on a year-over-year basis, accelerating modestly from March, which followed a near-70% advance in February. Though GM (GM) and Volkswagan (VLKAY) continue to dominate China’s auto market, Valuentum is expecting substantial auto market growth in the country that will pave opportunities for all of the major constituents. China is the largest car market in the world, and it will remain the number one car-purchasing country for the foreseeable future.

Source: IHS AutoInsight April 2013; Accenture Research Analysis; Valuentum Projections

All told, we were very pleased with Ford’s buyback announcement and the progress it is making with respect to US sales, which recovered nicely from the harsh winter weather earlier this year. The automaker’s sales in China continue to grow faster than overall sales in the China auto market, and we would expect this to continue. We don’t expect to make any changes to Ford’s weighting in the Best Ideas portfolio in light of these two developments, and we continue to expect upside beyond $20 per share. We show our technical projection of the firm anchored by our fair value estimate below. Remember to view its landing page here.