On January 30, PotashCorp (POT) reported fourth-quarter and full-year 2013 results. The fertilizer giant faced challenging market conditions during much of the year, and PotashCorp CEO Bill Doyle was quick to note that “this past quarter was a difficult one. Pricing headwinds – most notably in potash – weighed on (its) performance, although there were signs as the quarter came to a close that the uncertainty in global markets was beginning to abate. (Its) focus remain(s) on those things (it) can influence, and (it) took important steps to enhance (its) competitive position across all three nutrients and prepare the company to deliver better performance.”

Unfortunately, the most important “thing” is something that PotashCorp cannot control: pricing. Competitive pressures and a breakdown of the global potash oligopoly drove the firm to realize average potash prices that were significantly lower than the year-ago period ($282 per tonne in the fourth quarter and $332 per tonne for the full year). We believe that pricing power is one of the key components revealing the strength of a company’s competitive advantages, and without the healthy functioning of the global potash oligopoly, PotashCorp’s competitive advantages break down. There are a number of industries that dominate their respective niches, where pricing competition is not always rational (think about the pricing wars between Boeing and Airbus). Though many are optimistic that a potash price recovery is upon us (see here), recent events have highlighted the fragility of PotashCorp’s competitive position–without a healthy-functioning oligopoly, PotashCorp is worth much less.

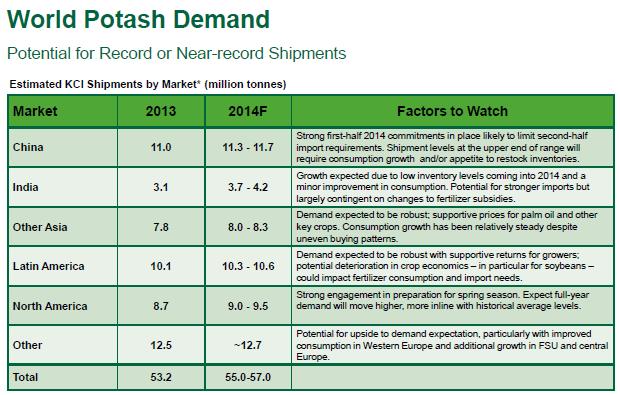

Looking ahead, PotashCorp expects global shipments of potash for the year to improve to 55-57 million tonnes, an increase of approximately 5% from 2013 levels (see image below). The firm cautioned, however, that achieving such levels will be dependent in part on continued sales efforts (“consistent buyer engagement”) and a devotion to developing agricultural economies to improve nutrient-deficient soils. PotashCorp expects its 2014 potash sales volumes to approximate 8.2-8.6 million tonnes, though it also noted that new pricing levels through the early part of 2014 will result in a lower realized price than during fourth-quarter 2013. PotashCorp has responded with cost-reduction targets in the $15-$20 per tonne range from 2013 levels mainly by increasing production at its lowest cost facilities. For the full-year 2014, Potash expects earnings in the range of $1.40-$1.80 per share, down materially from full-year 2013 earnings of $2.04 per share.

Image Source: PotashCorp

Valuentum’s Take

Weaknesses in PotashCorp’s business model have been exposed, and pricing strength for the fertilizer giant remains elusive. Though it is possible that a return to rational pricing in the potash market is right around the corner, we think this development rests more on political and behavioral tendencies of potash-producing entities (see here), which can be unpredictable at times, than on actual inflation-adjusted core pricing strength (as in the case of a consumer packaged goods company, for example). Many investors are clinging to the potash market dynamics of yesteryear, but we continue to be cautious. Our best ideas are included in the Best Ideas portfolio and Dividend Growth portfolio.

Chemicals – Agricultural: AGU, CF, CMP, IPI, MON, MOS, POT, SMG, TNH