The most common theme expressed by constituents in the chemicals (broad) industry during the calendar second quarter had to do with concerns about the economy. The negative tone was so prevalent that either management teams in the industry have started to engage in an executive form of “group think” or the economic environment continues to be difficult for many cyclical and largely commoditized chemical entities. Many industries, including housing, aerospace, and automotive, continue to perform well, but we think the latter interpretation of such commentary is likely correct:

Albemarle (ALB): “an economic environment that saw continued sluggishness across Europe…and a much weaker China”

Air Products (APD): “continued economic weakness…our outlook for the remainder of the fiscal year continues to be tempered by modest economic growth”

Celenese (CE): “as we look to the remainder of 2013, we expect the weak economic conditions that exist today will continue”

DuPont (DD): “market challenges associated with a sluggish global economy”

Ecolab (ECL): “the global economic backdrop remains challenging”

Huntsman (HUN): “many areas of the global economy continue to moderate or languish”

NewMarket (NEU): “slower than expected economic recovery in our customers’ end markets”

Praxair (PX): “poor overall business confidence…lower private and public spending on capital projects.”

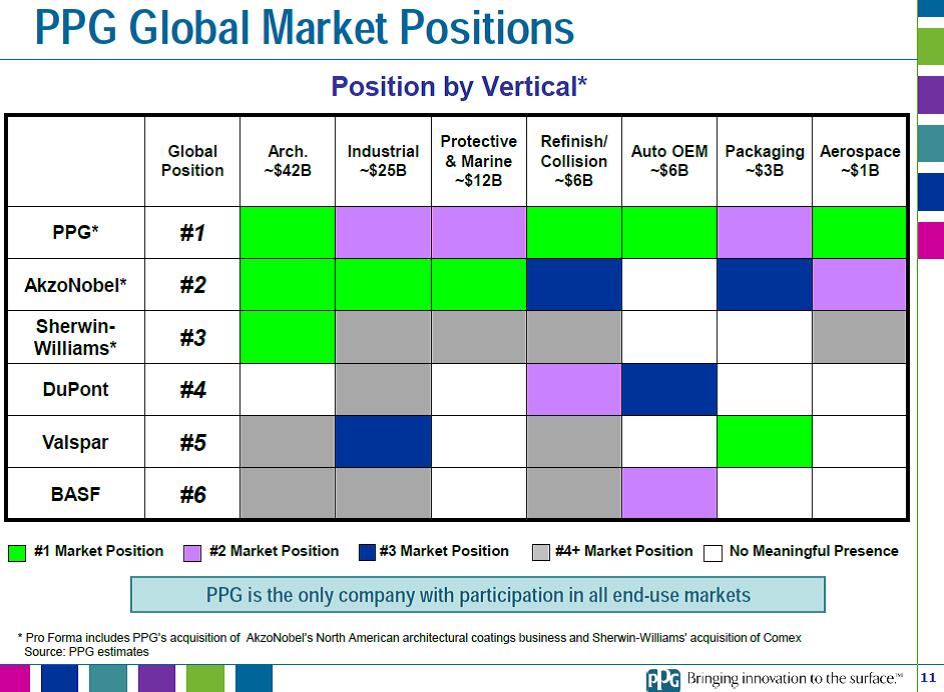

Still, there were a few bright spots, with perhaps the strongest performer during the calendar second quarter being PPG Industries (click ticker for report: ). The firm is a major global supplier of coatings for customers in a wide array of end markets. PPG Industries’ aerospace coatings business supplies sealants and coatings to many commercial and military aircraft, its architectural coatings are used by painting and maintenance contractors for decoration and maintenance of residential and commercial buildings, and its industrial coatings are used by automotive original equipment manufacturers (OEMs).

About PPG Industries

Image Source: PPG

Image Source: PPG

Image Source: PPG

PPG’s second quarter (results released July 18) set new records in terms of both net sales and adjusted earnings, which advanced 16% and 27% over the prior-year period, respectively. The company continues to benefit greatly from increased auto production in North America and higher local consumption in China. Automotive OEM coatings volumes within its ‘Industrial Coatings’ segment grew 12% in the period, and aerospace and automotive refinish within its ‘Performance Coatings’ segment advanced at a mid- to high-single digit pace.

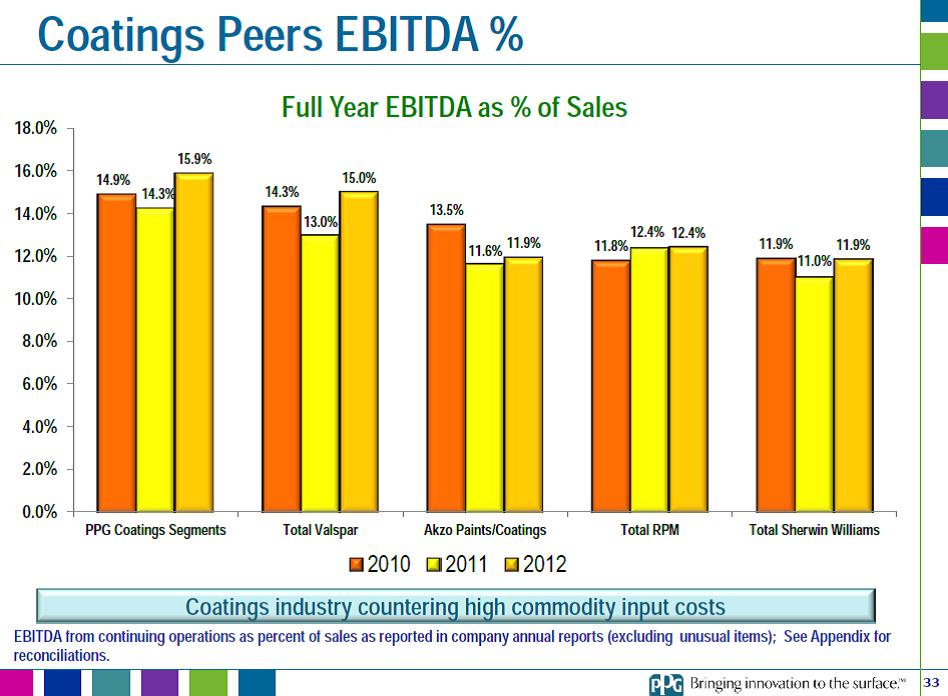

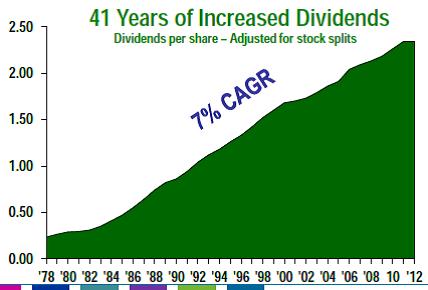

Though the firm announced a business restructuring program that will impact third-quarter results, we were very pleased with the quarterly performance, including cash flow from operations, which is roughly $500 million year-to-date (up $80 million from the year-ago period). PPG is acquisitive, but for the most part, we like its organic growth potential via emerging market expansion, increased sales content per airplane, and improving auto production. The firm isn’t too capital-intensive (capex averages about 2.5% of sales), has pricing power, and its top-market share position in a consolidating industry is hard not to like. Plus, the company’s EBITDA margin is best among peers, and its dividend track record is among the best we’ve seen, though PPG’s annual yield of about 1.5% isn’t a head-turner (the firm is a Dividend Aristocrat).

Image Source: PPG

But as with many excellent companies, shares aren’t cheap and trade north of our estimate of their intrinsic value at the time of this writing. Still, it’s a company we wouldn’t hesitate to add to our Best Ideas portfolio at the right price (below the low end of our fair value range on improving technical and momentum indicators).

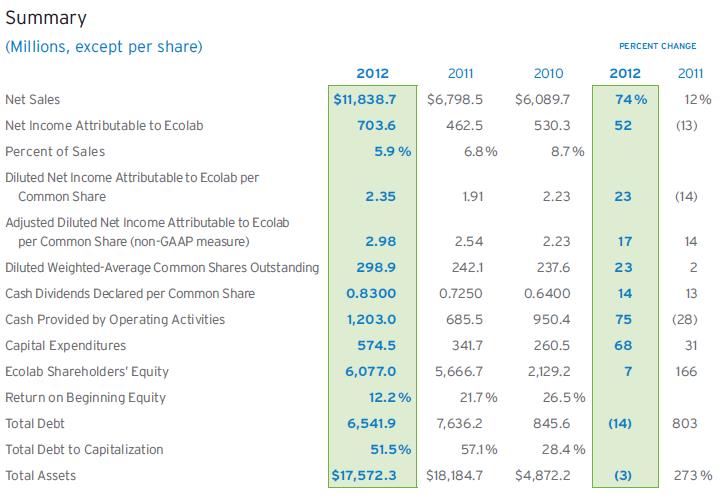

Ecolab’s (click ticker for report: ) second-quarter results, released July 20, were also very solid. The water and hygiene services firm put up record adjusted earnings per share on roughly 13% net sales expansion. The quarterly performance was so strong that management raised its full-year adjusted earnings outlook to the range of $3.48-$3.56 per share, representing a 17%-19% increase versus 2012.

About Ecolab

Image Source: Ecolab

Though we like Ecolab’s performance, we note that the firm’s net debt has ballooned as a result of the recent Nalco acquisition, which makes Ecolab’s Valuentum Dividend Cushion score a less-appealing alternative to that of PPG Industries—despite Ecolab also being a Dividend Aristocrat. Free cash flow remains robust at Ecolab (about 5% of sales in 2011 and 2012), but it trails that of PPG Industries, which on average converts a high-single-digit percentage of sales to free cash flow (cash from operations less capital expenditures). Total debt to capitalization was roughly 52% at the end of 2012 for Ecolab (it was roughly 10 percentage points lower at PPG).

Image Source: Ecolab 2012 Annual Report

However, we think a comparison of their respective net debt positions is more informative. PPG Industries’ net debt position at the end of the second quarter was $1.57 billion versus $6.26 billion for Ecolab. When it comes down to comparing these two Dividend Aristocrats, PPG Industries’ balance sheet, cash-flow conversion, and dividend yield are simply better. Ecolab’s shares aren’t cheap either.

Another standout performer in the group during the second quarter was Eastman Chemical (click ticker for report: ). This was a firm we had profiled in the November 2011 edition of our Best Ideas Newsletter (see page 5).

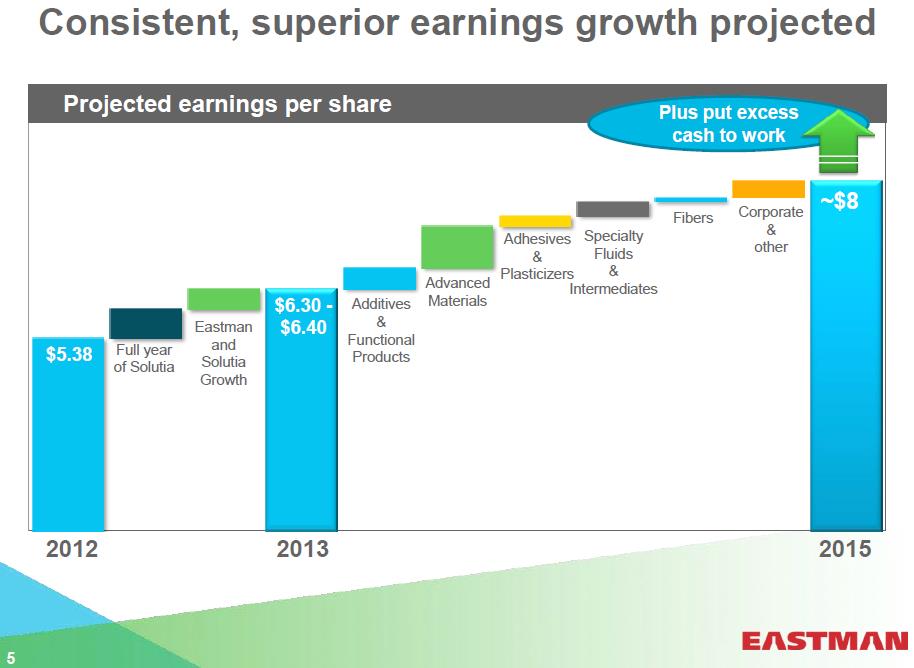

Though proforma sales expansion (adjusting for the Solutia acquisition) was meager at roughly 2%, it’s hard not to like Eastman Chemical’s second-quarter earnings, which were the best ever for the period. In addition to increasing expectations for 2013 earnings per share ($6.40-$6.50), the company also issued an optimistic intermediate-term outlook–management expects ‘annual’ double-digit earnings growth through 2015 (to approximately $8 per share) thanks primarily to strong end market performance.

Image Source: Eastman Chemical

Image Source: Eastman Chemical

At the time of this writing, Eastman Chemical trades above our estimate of its intrinsic value, and its Valuentum Dividend Cushion score is not as strong as Dividend Aristocrat PPG Industries. Still, we’ll be watching its stock price performance closely to announce its bargain-basement status (should the opportunity ever present itself again).

In part because we like their business models so much, the biggest disappointment to us in the chemicals (broad) space during the second-quarter were the industrial gas firms: Airgas (ARG), Air Products and Praxair. Air Products witnessed adjusted earnings deterioration during the period, while bottom-line growth at Airgas and Praxair was meager at best. Air Products boasts a hefty $3 billion backlog, but its outlook continues to be tempered by modest economic expansion. Airgas is facing a challenging refrigerants market and pointed to ongoing uncertainty within its customer base (and only slight sequential improvements in volume). Praxair also noted that demand for packaged gas weakened during the period, but it too has a decent backlog of large onsite projects. Neither firm’s performance stacked up to that of PPG Industries, Ecolab, and Eastman Chemical during the calendar second quarter.

Valuentum’s Take

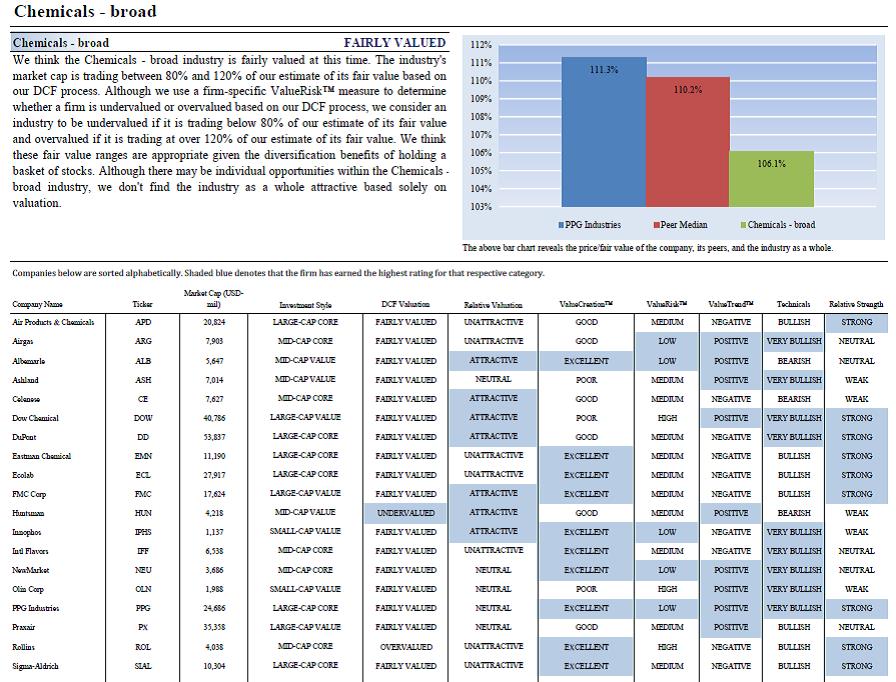

The chemicals (broad) industry is not cheap, by any stretch of the imagination. At the time of this writing, the group is collectively trading at more than a 6% premium to its estimated intrinsic value (see image below taken from page 11 of PPG Industries’ 16-page report). We think the market is not factoring in the cyclical nature of many constituents, which is leading to the valuation disconnect. Having made one of the best calls in the space on Eastman Chemical, our current favorite fundamental idea is PPG Industries. We note, however, that we’re waiting patiently for an entry point in shares on the basis of valuation.

Source: Valuentum

| Recently-Reported Quarterly Performance Statistics | ||||||

| Company Name | Organic Revenue Growth YoY% | Adjusted Operating Income Growth YoY% | Adjusted Net Income Per Share Growth YoY% | Management’s Outlook & Commentary (source: company press releases, conference calls) | Link to Quarterly Release | |

| Albemarle (ALB) | -7.4% | -28.2% | -24.2% | Expects Macroeconomic Weakness; Profits Down in Every Business Segment in 2Q (Polymer Solutions, Catalysts, and Fine Chemistry): “Our businesses delivered EBITDA margins of 22% in spite of facing lower metals surcharges and an economic environment which saw continued sluggishness across Europe, weak electronics and construction markets and a much weaker China than most anticipated at the beginning of the year. We also successfully met several key milestones with regard to bringing on our bromine and organometallics expansions, which will be essential drivers of our long term growth.” | Albemarle reports second quarter 2013 results, July 17 | |

| Air Products (APD) | -2.0% | -3.0% | -4.0% | Focused on Executing Its Record $3 Billion Backlog: “Productivity and solid execution offset continued economic weakness, enabling us to deliver earnings within guidance. We remain focused on delivering on our commitments and executing on our $3 billion backlog — and we expect these projects to be immediately accretive to earnings and cash flow as they come online. As stated previously, we are actively assessing additional actions that we can take that would result in increased value to our shareholders. While our review continues, we have already identified further actions we expect to take to improve margins and returns…While our outlook for the remainder of our fiscal year continues to be tempered by the modest economic growth, our focus on increasing shareholder value remains unwavering. Our emphasis on cost reduction, productivity improvement and disciplined project execution remain key priorities. Our future prospects are solid given our record project backlog and the significant leverage in our existing assets.” | Air Products Reports Fiscal Q3 Financial Results, July 23 | |

| Airgas (ARG) | Flat | 3.2% | 1.0% | Uncertainty Continues.”Airgas is well-positioned for growth. We continue to be optimistic about the long-term prospects for the U.S. manufacturing and energy industries, as well as non-residential construction, and our ability to leverage our unique value proposition and unrivaled platform to capitalize on the opportunities that lie ahead. Near-term uncertainty persists for our customers, however, and accordingly the mid-point of our fiscal 2014 guidance assumes only slight sequential improvement in daily sales volumes as the year progresses and low to mid single digit year-over-year organic sales growth rates for the remainder of the year. Given the challenging and unpredictable nature of the refrigerants market, including its impact on our first quarter results, our guidance also assumes an estimated $0.12 to $0.15 year-over-year negative impact related to R-22 pricing and volume following the EPA’s ruling. Our EPS guidance assumes a contribution from SAP benefits, net of expenses, of approximately $0.47 per diluted share in fiscal 2014.” | Airgas Reports Fiscal 2014 First Quarter Earnings, July 25 | |

| Ashland (ASH) | -4.0% | -19.7% | -18.4% | Raised Free Cash Flow Expectations. “Market demand and volume trends have begun to improve in several areas of our business, providing momentum as we head toward the end of our fiscal year. Although we face difficult year-over-year comparisons in guar sales and profitability in the fourth quarter, this will be the final quarter of that effect. We are generating higher free cash flow than originally expected, leading us to raise our estimates for the full fiscal year. And earlier this month we rolled out our enterprise resource planning system across the former ISP sites. We expect this SAP system to be fully implemented in the fourth quarter, allowing us to capture the majority of the remaining $15 million in synergy savings as we enter fiscal 2014. | Ashland Inc. reports preliminary financial results for third quarter of fiscal 2013, July 25 | |

| Celenese (CE) | Categories Member Articles | |||||