A version of this article appeared on Seeking Alpha’s website: https://seekingalpha.com/article/280602-mercks-shares-look-undervalued

As part of our process, we employ a discounted cash-flow model to arrive at a fair value estimate for every company within our equity coverage universe. In Merck’s (MRK) case, we think using a discounted cash-flow model is the best tool for valuation. We outline below our valuation summary for Merck and offer up our model template to investors if they are interested in using it to value any operating (non-financial) company they wish. This model template can be found at DCF Valuation Model Template.

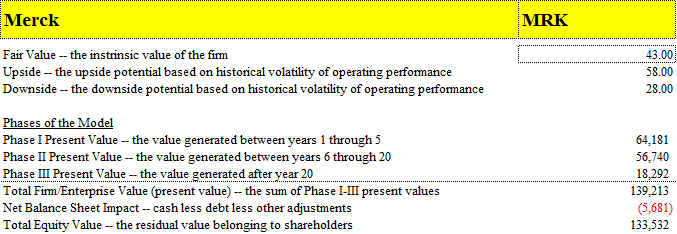

Valuation Summary

We think Merck’s shares are worth $43 each based on our discounted cash-flow process. We’re forecasting revenue expansion in the low-double-digits for fiscal 2011 and a slight decline for fiscal 2012, improving to low-single-digit expansion by fiscal 2014-2015. We expect the firm to earn $3.73 per share in fiscal 2011 and $3.85 per share in fiscal 2012, both of which line up with consensus forecasts. We display our valuation summary below. We use a 10%-10.5% weighted average cost of capital to discount future free cash flows.

(Click to enlarge)

In all, we’d consider adding Merck to our should it reach the lower bound of our downside scenario — just under $30 per share. However, with the firm’s dividend yield north of 4%, we may be a bit more flexible with our entry point. We would expect the firm to converge to our $43 fair value estimate within the next few years, while paying investors a nice series of dividend payments along the way.