This article appeared on Seeking Alpha. Please view disclosures: https://seekingalpha.com/article/279186-a-deep-look-into-microsofts-valuation

As part of our process, we employ a discounted cash-flow model to arrive at a fair value estimate for every company within our equity coverage universe. In Microsoft’s (MSFT) case, using a discounted cash-flow model is the best tool for valuation, given the firm’s robust cash-flow characteristics. We outline below our forecasts and fair value estimate for Microsoft and offer up our model template to investors if they are interested in using it to value any operating (non-financial) company they wish. This model template can be found at DCF Valuation Model Template.

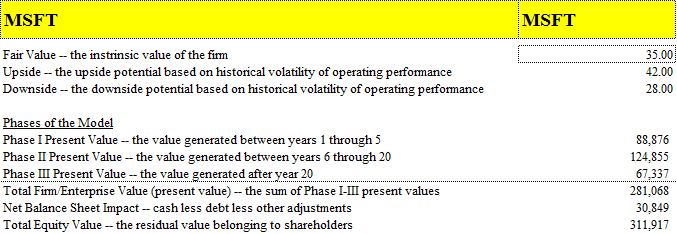

Valuation Summary

We think Microsoft’s shares are worth $35 each. We’re forecasting revenue expansion in the low-double-digits for fiscal 2011 and in the mid-single-digits for fiscal 2012, slowing to the low-single-digits by fiscal 2014-2015. We expect the firm to earn $2.56 per share in fiscal 2011 and $2.77 per share in fiscal 2012, the latter implying less than a 10x earnings multiple at today’s prices. We think Microsoft’s free cash flow trajectory should garner a multiple on next year’s earnings of about 12.7x, indicating significant upside from today’s levels.

(Click to enlarge)

We outline below our forecasts for Microsoft’s business, across all three of the key financial statements found in our valuation model. Even under these relatively conservative growth assumptions, Microsoft offers considerable upside from today’s levels. With the firm’s valuation attractive, we think a technical improvement would indicate that the market would no longer be viewing Microsoft as “dead money” and serve as one of many potential catalysts for a move higher. Should this technical improvement occur, we may consider adding the stock to our Best Ideas list. In fact, our methodology allows us to identify the most undervalued stocks via our DCF process and bring them to our subscribers’ attention at the best time technically to avoid the opportunity cost of owning an undervalued company with no particular catalyst (fundamental or technical) for its value to be recognized by the market.

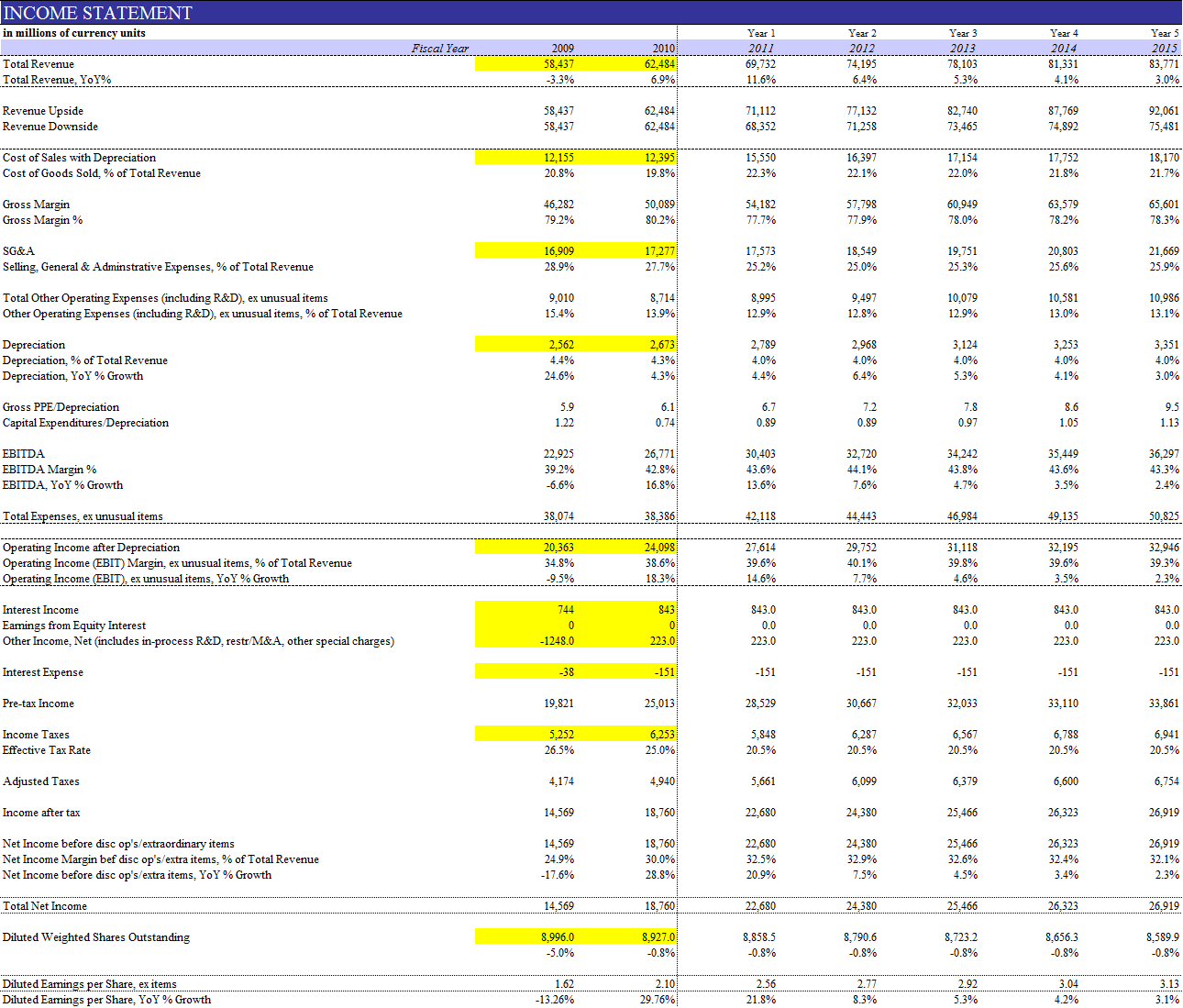

Income Statement

(Click to enlarge)

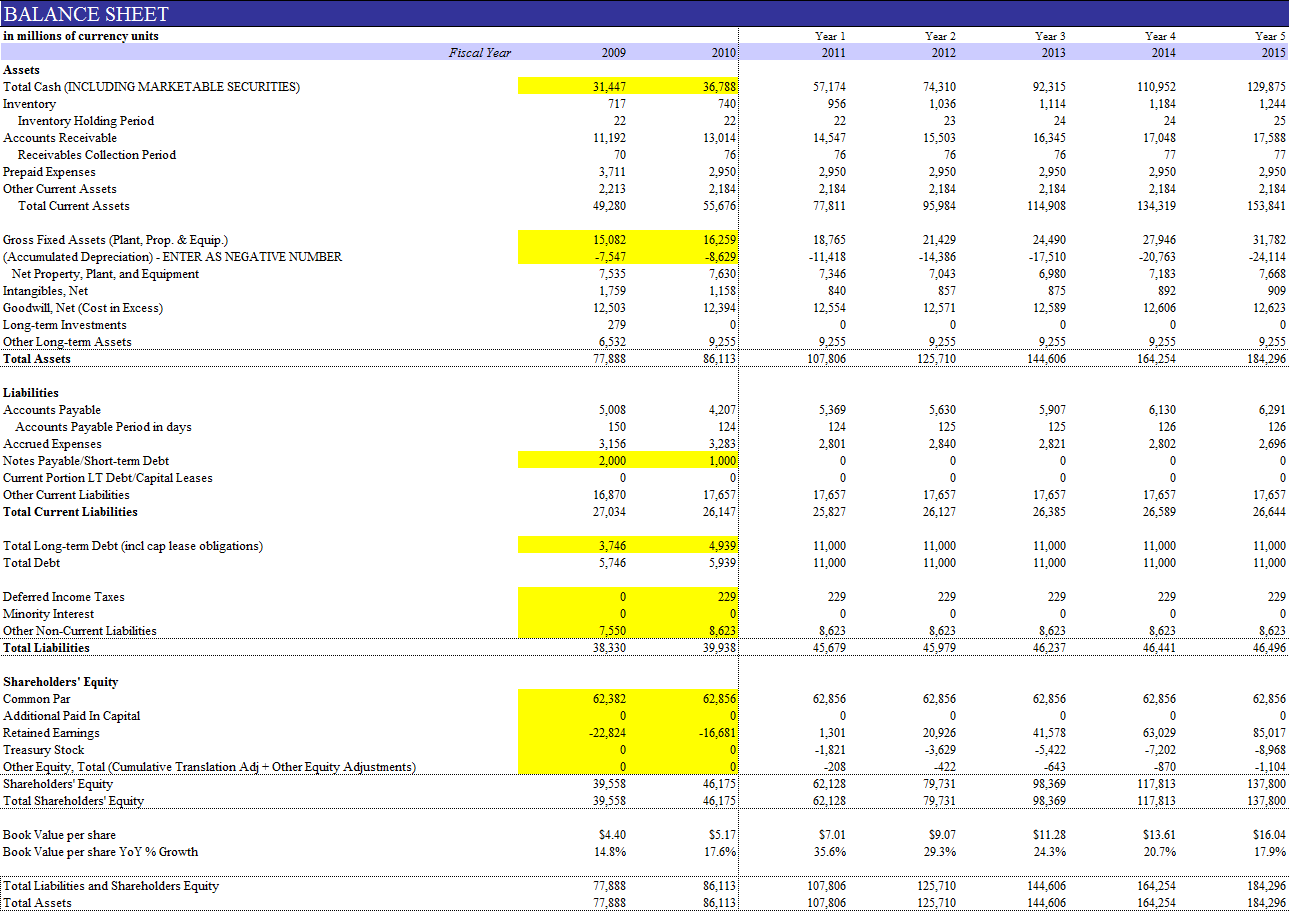

Balance Sheet

(Click to enlarge)

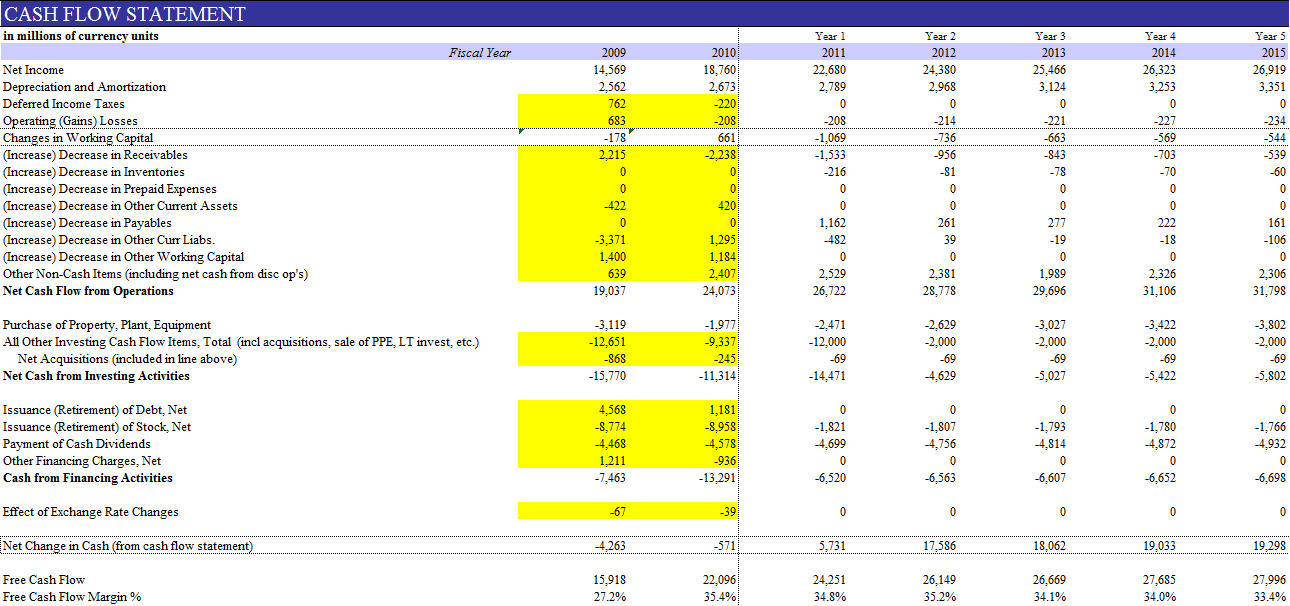

Cash Flow Statement

(Click to enlarge)

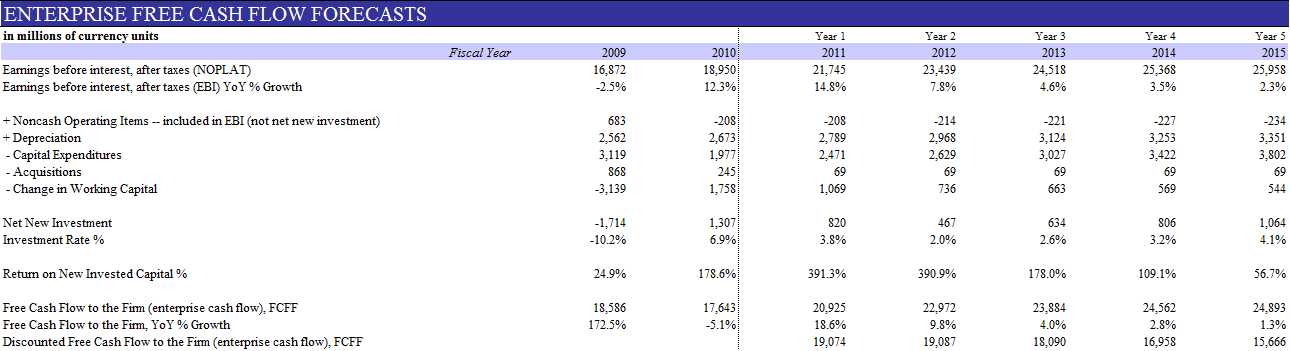

Free Cash Flow Forecasts

(Click to enlarge)

In all, we think Microsoft’s valuation is very tempting at this point in time, but we’re waiting for improvement in the firm’s technicals before adding it to our Best Ideas list.