How to Navigate the Low Return Environment

Image Shown: Investors continue to gamble on meme stocks and cryptocurrencies. Image Source: QuoteInspector.com.

Modern Finance Is Dead, Long Live Value Trap

By Brian Nelson, CFA

At Valuentum, we don’t believe in many of the quantitative theories out there. We like to operate within the stock component of market returns, as this has historically been the strongest place to focus one’s efforts. We don’t think it makes sense to add “bad” assets to a portfolio just for the sake of diversification. Can you imagine adding pipeline MLPs to your portfolio in June 2015?

If we can find great ideas within the stronger relatively performing stock market, we think we’ll be far better off than any stock/bond mix that one may choose. In fact, during the past 10 years, this view has held up. While our simulated stock newsletter portfolios have been great, a 60/40 stock/bond portfolio has underperformed the S&P 500 index during the past 10 years.

The underperformance hasn’t been small; on the contrary, it's been eye-opening. For example, a 60%/40% stock/bond portfolio, as measured by the Vanguard Balanced Index Fund Investor Shares (VBINX) trailed the S&P 500 by over 110 percentage points during the trailing 10-year period ending July 30, 2020. The outlook for the 60/40 stock/bond portfolio isn’t that great either. According to a recent Financial Times article:

Based on historical valuations and returns, AQR, the investment group, now estimates that a traditional 60/40 portfolio — split between 60 per cent in equities and 40 per cent in bonds — will return just 2.1 per cent a year after accounting for inflation over the next five to 10 years. A US 60/40 portfolio will return a miserly 1.4 per cent in the coming years, compared to an average of nearly 5 per cent since 1900.

Investors today are faced with one of the biggest challenges of their lifetimes. Many won’t be happy with such a meager return outlook for the 60%/40% stock/bond mix, and many won't feel comfortable gambling on meme stocks and cryptocurrencies to bolster "expected" returns in the context of modern portfolio theory. For one, AMC Entertainment (AMC) recently warned investors “against investing in (its) Class A common stock, unless you are prepared to incur the risk of losing all or a substantial portion of your investment,” while Bitcoin just registered one of its worst monthly returns ever in May.

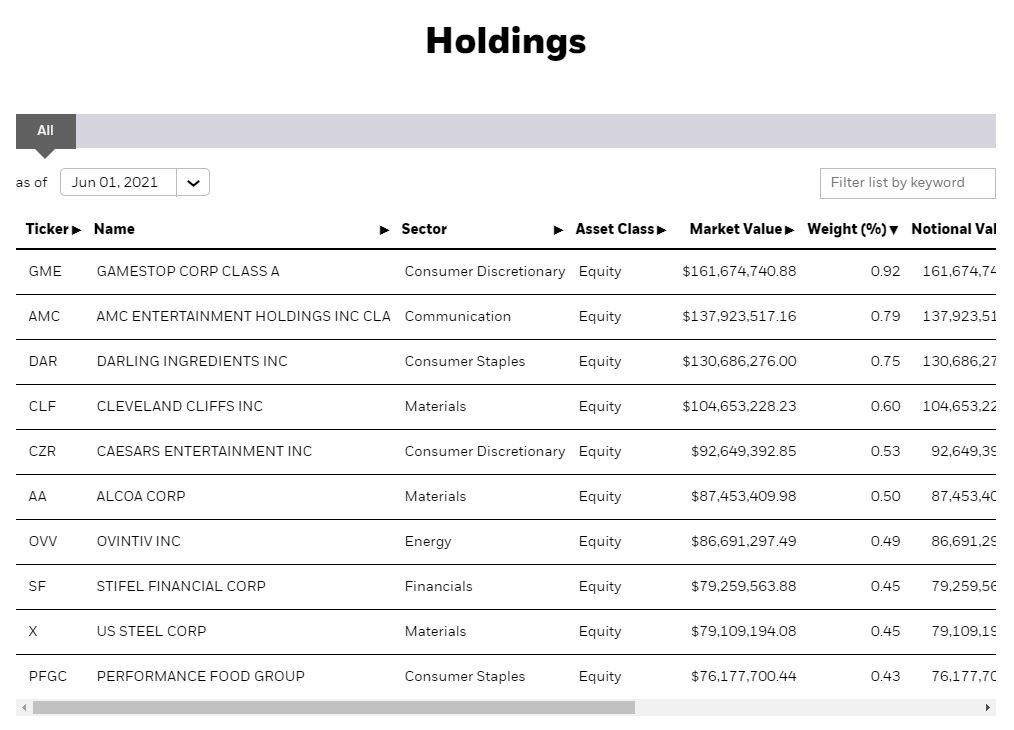

Adding to the frustrations of many investors, the value-versus-growth conversation continues to be completely nonsensical, almost asinine, with two meme stocks GameStop (GME) and AMC Entertainment now the two largest weightings in the iShares Russell 2000 Value ETF (IWN). Paying attention to the fundamentals of the companies in your portfolios to avoid the risk of $0 will always trump any discussion about whether a stock is "value" or "growth."

Image Shown: The top holdings of the iShares Russell 2000 Value ETF. Quantitative value, for all intents and purposes, has become meme-stock oriented, further supporting the nonsensical nature of separating stocks with the labels of value versus growth. Image Source: iShares.

In fact, be careful about extrapolating anything from "value" versus "growth" quant analysis. It suffers greatly from the "garbage in" component of statistical pitfalls. Think of stocks with low price-to-book ratios, for example, as spheres. When thrown into water, these spheres either sink or float, but it is not the sphere shape, itself, that is causal to its floatation, but something else. This is how I think about the price-to-book ratio, or the traditional quant value factor – it is not causal to the return outcome.

There is no better time than now to study the cash-based sources of intrinsic value of equities and finetune one's stock selection skills. This may be the most important tool in your investor toolkit in the coming years as both equities and bonds may encounter low market returns, in aggregate, while cryptocurrencies and alternative asset classes experience whipsawing volatility. Further, it's very important to conduct your own due diligence with a focus on net cash and future expected free cash flows and not rely on short-cut multiple analysis or spurious quantitative relationships.

Concluding Thoughts

There are no shortcuts to success in the markets and focusing on individual security selection within the equity component of the capital structure with a focus on long-term cash-flow-based fundamentals continues to be a prudent strategy, in our view. Success rates within the Exclusive publication, for example, continue to be fantastic. The success rates* for capital appreciation ideas (49 of 59) and short idea considerations (53 of 59) in the Exclusive publication are now ~83%% and ~90% from July 2016-May 2021.

For investors focused on capital appreciation potential, the Best Ideas Newsletter portfolio may be worth a look. For those with a dividend growth focus, the Dividend Growth Newsletter portfolio has a plethora of ideas. Though AT&T (T) threw us a curve ball with respect to changes in its dividend payout recently, the prudent and diversified nature of the simulated High Yield Dividend Newsletter portfolio continues to deliver, while idea generation remains robust. Many of our options ideas have done quite well, too.

We remember when the S&P was trading at about 3,000, and we pegged a fair value range on the S&P 500 of 3,530-3,920, and many thought we were crazy at the time (the S&P 500 now stands at ~4,200 at the time of this writing). You have to understand: Stock prices and returns are based on future expectations and forecasts, a truism that AMC Entertainment’s trading activity has all but proven. AMC defeats efficient markets theory. AMC defeats value versus growth. AMC defeats backward-looking analysis. Modern finance is dead. The field must evolve.

Long live Value Trap.

* The percentage of ideas highlighted in the Exclusive that have moved in the direction of our thesis (i.e. up for capital appreciation ideas and down for short idea considerations) through the current price or closed price, with consideration of cash and stock dividends. Success rates do not consider trading costs or tax implications.

Related: GBTC, COIN, RIOT, MARA, BTBT, MSTR

Other meme stocks: BBBY, EXPR, BB, NOK, MVIS, SNDL, PLTR, TLRY, NIO

-----

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, and IWM. Brian Nelson's household owns shares in HON, DIS, HAS. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment