Is AMR's Equity Practically Worthless?

This article originally appeared on Seeking Alpha. Please view disclosures: https://seekingalpha.com/article/270933-is-amrs-equity-practically-worthless

As outlined in "Why Airline Stocks Are Not Long-Term Investments," pegging a fair value on an airline's equity is a nearly impossible task due to the tremendous operating leverage inherent to their business models and the fact that key valuation drivers such as unit revenue and unit cost are largely out of their control. That said, let's take a look at what AMR's equity investors have to overcome to recognize any value in their holdings.

- AMR's pension obligations are staggering: ~$24 per share. Unlike peers that passed along their pension obligations to the Pension Benefit Guaranty Corporation via Chapter 11 reorganization (United Continental (UAL), Delta (DAL), etc.), AMR still retains this huge burden. The underfunded status, as of the end of last year, of its pension and retiree medical/other benefits obligations (OPEB) was an astounding $8 billion-plus. This is derived by taking the firm's projected benefit obligation (pension benefits: $12.97 billion; OPEB: $3.1 billion) less the fair value of the corresponding plan assets (pension: $7.7 billion; OPEB: $0.23 billion). Based on roughly 333 million diluted shares outstanding at the end of last year, this $8 billion-plus underfundedness translates into a burden of roughly $24 per share.

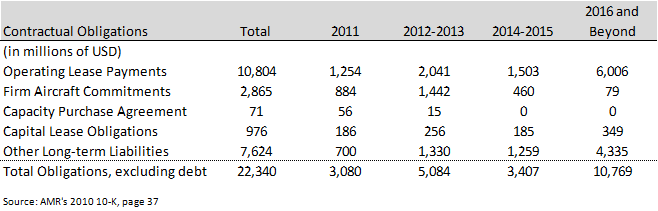

- AMR's net debt load is massive: ~$17 per share. As of the end of the first quarter, AMR's net debt position stood at about $5.6 billion ($5.8 billion in cash and short-term investments less $11.4 billion in debt), excluding the capitalization of operating leases (which are also debt-like instruments). Again, using the 333 million diluted shares as the denominator, this represents about $17 per share. Importantly, investors should also be aware of the firm's other operating commitments that will inevitably pressure results and its cash position in the years ahead.

What does all of this mean? Essentially, in order for AMR's equity to be worth anything, the firm would need to generate a discounted enterprise free cash flow stream (i.e. free cash flow to the firm) that amounts to more than $41 per share (or about $13.7 billion).

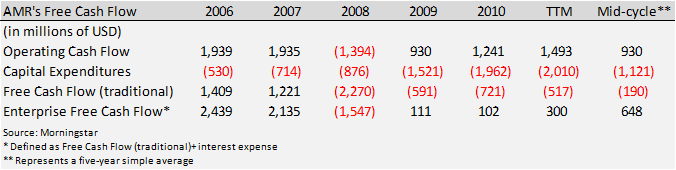

Let's get a feel for how free cash flow has trended during the past number of years.

The firm's federal net operating losses of approximately $6.7 billion and state net operating losses of $3.7 billion should allow it to avoid paying taxes for many years to come. Since these tax benefits have been in place for some time, it may be relatively straightforward to use the mid-cycle estimate of $648 million in enterprise cash flow (see above), which notably includes the boom years of 2006 and 2007 when WTI crude prices were $66 and $72, respectively, well below today's levels.

If we value AMR's operating assets through a standard mid-cycle perpetuity function, we're looking at about $6 billion to $7 billion in value (assuming a very generous 10% discount rate, given AMR's risk profile) -- not even close to the $13.7 billion equity investors need to break even.

Admittedly, there's always option value in companies like AMR should mid-cycle performance in the industry be raised considerably. For example, if crude oil prices fell below $70 permanently and global economic growth resumed the pre-Great Recession levels, AMR could see its stock pop to over $20 per share, assuming peak cash-flow assumptions are now the new norm for the company and industry.

Needless to say, this is a very unlikely scenario, and modeling peak assumptions into perpetuity for an extremely cyclical industry is a classic no-no in estimating long-term intrinsic value. And while a sum-of-the-parts analysis for AMR (breaking apart Eagle, its frequent-flyer program) may suggest even higher valuations, especially during optimistic times, we caution investors that breaking apart an entity does little to alter the underlying long-term, cash-flow dynamics of the components of that entity.

AMR's equity is not worth $0 per share given the concept of option value. But with a break-even, mid-cycle enterprise free cash flow number that's north of about $1.4 billion (assuming very generous discount rates, given its competitive position and well-documented risks of the airline industry), AMR has some work to do to deliver any value to shareholders.

Disclosures: Brian Nelson owns put options on AMR at the time of this writing.